Companies like it Alphabet, MicrosoftAnd Nvidia are attracting a lot of attention in the artificial intelligence (AI) race – the first two because they are investing in public-facing products, such as ChatGPT (Microsoft) and the generative AI chatbot Gemini (Alphabet). And in Nvidia’s case, it’s thanks to its indispensable chips and incredible stock performance.

But don’t forget what’s behind the curtain. A number of smaller, lesser-known companies are also playing a key role in the development of AI. Let’s get to know one of them.

Why are data centers important?

Nvidia’s recent success is driven by data center revenue, which reached $22.6 billion last quarter, an astonishing 427% year-over-year growth. Why are data centers so important? Data centers form a crucial infrastructure in which enormous amounts of information are stored, managed and processed. They enable cloud-based applications, e-commerce and much more.

Here are some fun data center facts:

-

There are more than 10,000 data centers worldwide, including more than 5,300 in the US

-

The average data center is approximately 100,000 square feet. While some are small, like the ones built by hyperscalers AmazonAlphabet and Microsoft could cover more than 1 million square feet.

-

The largest data center in the US, spanning 4.6 million square feet, is located in Oregon and operated by Metaplatforms.

-

Experts expect more than 120 hyperscale centers to come online annual for a decade. One plan, reported by Reuters, is a partnership between Microsoft and OpenAI (the maker of ChatGPT) for a $100 billion project called Stargate.

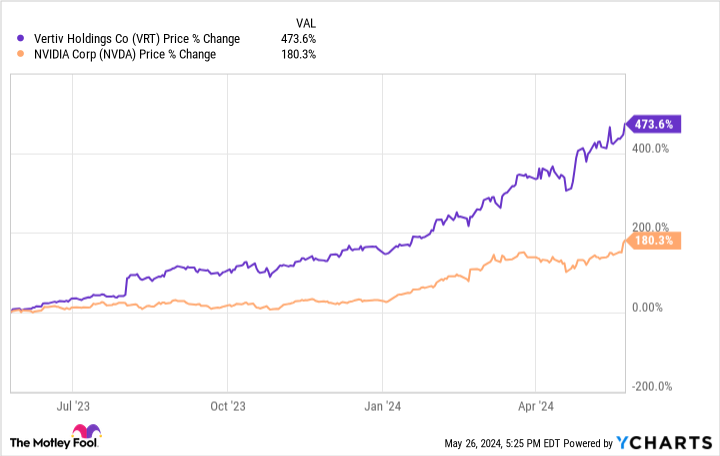

These enormous complexes are not just empty vessels with servers stacked inside. They require infrastructure such as racks, enclosures, power systems, thermal management components, switches, software and maintenance. Vertiv Holdings (NYSE: VRT) is a leading provider of this infrastructure, and increased demand has made it one of the hottest stocks on the market over the past year, as shown below.

Is Vertiv Holdings stock a buy?

The question is whether there is still gas in the tank. 2023 was a huge year for Vertiv. Revenue rose 20% to $6.9 billion, and margins increased. Vertiv reported gross and operating margins of 35% and 13%, respectively, compared to 28% and 4% in 2022. Expanding margins demonstrate Vertiv’s pricing power in the sector due to growing demand. They also show that the company’s business model will become even more profitable as it scales.

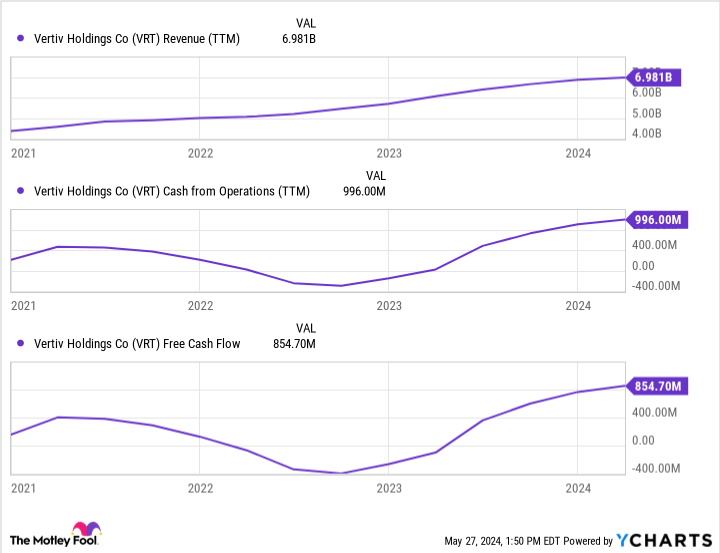

Operating cash flow and free cash flow also rose, as shown below.

The company used $600 million of its cash to buy back shares in the first quarter of 2024 at an average price of $66 per share, demonstrating Vertiv’s confidence that its stock was undervalued. The stock now trades for just over $100 per share.

First quarter revenue was $1.6 billion, a growth rate of 8%. The growth does not seem impressive at first glance; however, the company’s order volume grew by 60%. This means that customers have placed 60% more orders than in the previous year, and this turnover will be recognized in the coming quarters.

Vertiv also reported a book-to-bill ratio of 1.5. This means that for every €1 in revenue invoiced to a customer, Vertiv received €1.50 in new orders. Both figures indicate significant, continued growth, reinforcing the upward trend in demand for data center infrastructure.

The biggest risk for Vertiv investors is the stock’s valuation. The price-to-earnings ratio is almost 45, which seems high. But that’s not the whole story. Operating profit quadrupled in 2023 versus 2022, from $223 million to $872 million, and diluted earnings shot up from negative $0.04 to positive $1.19 per share. Vertiv also raised its full-year 2024 guidance in the first quarter. In the fourth quarter of 2023, the company forecast operating income growth of 23% for 2024. Last quarter it increased this to 28%.

Vertiv appears to be an excellent long-term investment, given its long-term tailwinds and profitable business model.

Should you invest €1,000 in Vertiv now?

Before purchasing shares in Vertiv, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Vertiv wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $671,728!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns May 28, 2024

Suzanne Frey, a director at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, former director of market development and spokeswoman for Facebook and sister of Mark Zuckerberg, CEO of Meta Platforms, is a member of The Motley Fool’s board of directors. Bradley Guichard has positions in Alphabet, Amazon, Nvidia and Vertiv. The Motley Fool holds positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls to Microsoft and short January 2026 $405 calls to Microsoft. The Motley Fool has a disclosure policy.

1 AI Stock Outpaced Nvidia by Nearly 300%; Is it still a strong buy? was originally published by The Motley Fool