It would probably be a mistake to simply forget about the net-leasing giant Real estate income (NYSE:O). It’s a well-run company, but it poses some problems for investors when you dig into the story a bit. For those looking for a little more growth, competitors Agree Real Estate (NYSE:ADC) And W. P. Carey (NYSE:WPC) perhaps more attractive.

I enjoy owning Realty Income

There is nothing inherently wrong with Realty Income. In fact, I own it and I’m glad I do. But it’s not the perfect real estate investment trust (REIT). Like any company, this also has a number of negatives.

For example, while it is the largest net lease REIT (net leases require tenants to pay most real estate costs), its size means its growth will likely be slow over time. It just takes more to move the needle. It’s true that being big offers better access to the capital markets, but dividend investors looking for a combination of yield and dividend growth are likely to be disappointed here. Notably, the dividend has only grown by about 3% annually over the past five years. That’s enough to keep up with the historical rate of inflation growth, but not really enough to increase the purchasing power of the dividend over time.

Realty Income is a foundational investment for a more diversified dividend portfolio. That’s why investors may want to consider alternatives or companion stocks like Agree Realty or WP Carey.

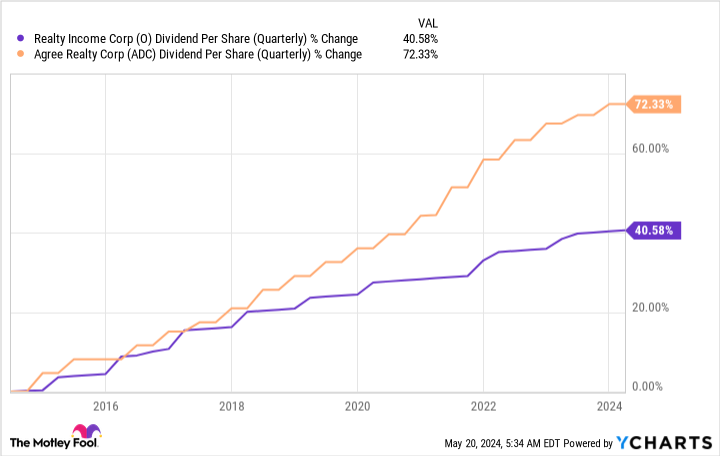

Agree Real estate is growing

Realty Income’s market cap is approximately $48 billion. Agree, the market cap is only about $6 billion. Realty Income owns more than 15,400 properties, while Agree owns about 2,100 properties. Obviously, Agree is a smaller REIT. But that’s a good thing if you’re interested in growth.

Simple calculations show that less investment in new properties is needed to have an impact on Agree’s turnover and profit. This has resulted in larger dividend increases, as shown in the chart below. This is no small detail, as Agree’s 70% dividend growth over the past decade pales in comparison to the 40% achieved by Realty Income. Because Agree focuses on US retail assets, it lacks the diversification of Realty Income, likely increasing risk slightly. But if you’re focused on dividend growth, Agree could be the better choice for you.

Switching gears at WP Carey

It’s very easy to dislike WP Carey these days, as the REIT has done the unthinkable: namely cut its dividend. This was part of what will ultimately be a transition year for this $13 billion market cap net-lease REIT. That said, it’s worth noting that the dividend is already back in growth mode.

So what’s going on? WP Carey has decided to exit the office sector and focus solely on retail and industrial spaces. Rather than exiting the office sector over time, management has ripped off the band-aid given the weakness of office space today. It spun off assets and sold a large number of offices in a short time. That eliminated a huge amount of cash flow and necessitated a dividend cut. But this move has also given WP Carey a lot of money that he can reallocate to other properties.

Add in some other moving parts, like a tenant exercising his right to buy the properties he occupies, and a few tenant-specific headwinds, and 2024 is shaping up to be a tough year for WP Carey. But the future seems like it could be much brighter. That’s driven not only by the money waiting to be invested, but also by the REIT’s large number of leases with inflation-linked rent escalators. For investors who like turnaround stories, WP Carey could be a more attractive option than Realty Income.

The return story

WP Carey’s yield is 5.7%, compared to about 5.6% for real estate income. That said, WP Carey likely has more upside potential as Wall Street starts to appreciate the changes it’s making to its business. Agree’s yield is just 4.9%, but given its more attractive historical dividend growth rate, many investors will still find it a more attractive option than Realty Income. Realty Income is a stable, slow-growth REIT, but that doesn’t mean it’s the best option for all investors.

Should you invest $1,000 in Agree Realty now?

Consider the following before purchasing shares in Agree Realty:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Agree Realty wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns May 13, 2024

Reuben Gregg Brewer has positions in Realty Income and WP Carey. The Motley Fool holds positions in and recommends Realty Income. The Motley Fool recommends WP Carey. The Motley Fool has a disclosure policy.

Forget Real Estate Income: 2 High-Yield REIT Stocks to Buy Instead was originally published by The Motley Fool