Nvidia (NASDAQ: NVDA) shares have delivered stunning returns again in 2024 after a blistering performance last year, but a closer look at the company’s price chart shows it has lost momentum over the past three months.

Nvidia shares have been flat during this period amid doubts about the company’s artificial intelligence (AI)-related prospects and its ability to continue delivering eye-popping growth. Investors may be wondering whether they should buy more shares of this semiconductor giant or start booking profits. However, it won’t be surprising to see Nvidia stock regain its mojo and deliver another stellar year in 2025.

In this article, we’ll look at some of the reasons why buying Nvidia stock before 2025 is a no-brainer.

Nvidia is expected to release more AI chips next year

Analysts expect Nvidia to witness a substantial increase in shipments of its AI graphics processing units (GPUs) by 2025. Market research firm TrendForce believes that Nvidia could witness a 55% increase in shipments of its AI GPUs next year, driven by the arrival of the company’s next-generation Blackwell processors.

TrendForce estimates that Blackwell will account for 80% of Nvidia’s AI GPU shipments next year. This also means that shipments of Nvidia’s older generation Hopper chips will remain solid into 2025. The good part is that TrendForce isn’t the only one expecting a jump in Nvidia’s AI GPU sales next year.

Japanese investment bank Mizuho has increased its estimate for Nvidia’s AI GPU shipments in 2025 by 8% to 10% compared to its previous estimate from July this year. Mizuho attributes this upward revision to an improvement in the company’s supply chain. More specifically, Nvidia’s foundry partner Taiwanese semiconductor manufacturing (popularly known as TSMC) is reportedly set to double its advanced packaging capacity, allowing the former to produce more AI GPUs.

Moreover, TSMC plans to continue increasing its advanced packaging capacity beyond next year. The foundry giant believes it will be able to achieve at least 60% annual growth in its chip-on-wafer-on-substrate (CoWoS) packaging capacity through 2026. This should put Nvidia in a nice position to take advantage of the fast-growing demand for AI chips.

Allied Market Research estimates that sales of AI chips could increase 38% annually through 2032, generating annual revenues of $384 billion. Nvidia is the dominant player in the AI chip market with a market share estimated at between 70% and 95%, although a closer look at its AI revenues compared to those of its rivals will indicate that its share is likely at the higher end off the market. that range.

More importantly, TSMC’s improving manufacturing profile should ensure Nvidia maintains its dominance in the AI chip market. Thus, higher sales of AI GPUs should translate into solid growth for Nvidia in the next fiscal year, while pricing power in this market should also lead to healthy bottom line growth.

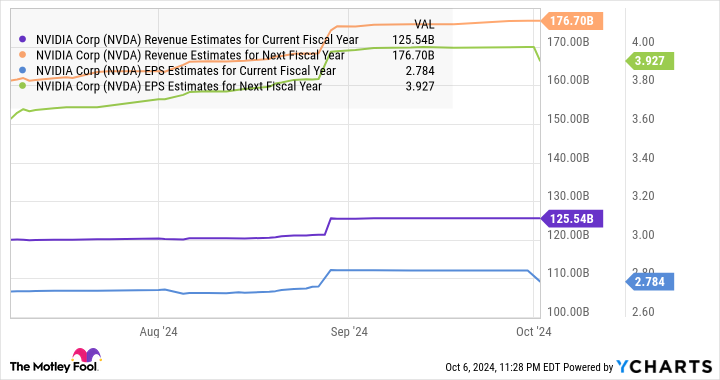

NVDA revenue estimates for current fiscal year data based on YCharts

The valuation does not have to be a problem given the potential growth

Some might point out that Nvidia is currently richly valued, with a price-to-earnings (P/E) ratio of 58, which is higher than Nasdaq-100 The index’s average earnings multiple is 32. But at the same time, Nvidia has been able to justify its valuation with excellent growth. In fact, Nvidia’s profit margin is currently lower than its five-year average price-to-earnings ratio of 72.

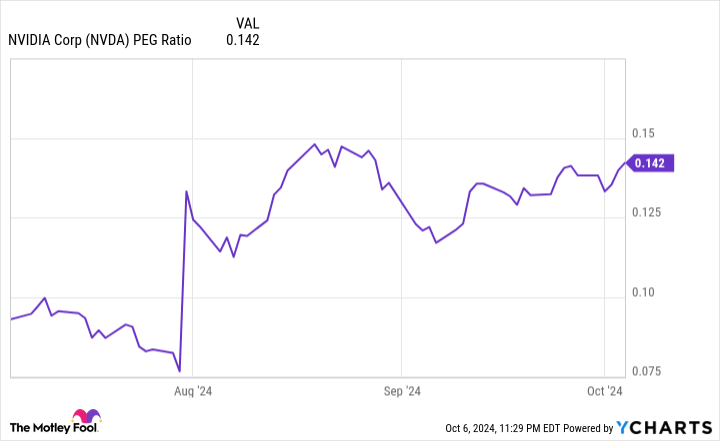

Furthermore, Nvidia’s price-to-earnings-growth ratio (PEG ratio) of just 0.14 means the stock is highly undervalued given the growth it is expected to deliver.

NVDA PEG Ratio data according to YCharts

The PEG ratio is a valuation measure that takes into account the potential earnings growth a company could achieve. A value of less than 1 means that the mentioned stock is undervalued. Therefore, now would be a good time for investors to stock up on Nvidia stock before the potential jump in sales of the company’s AI chips in 2025 sends them soaring.

Should You Invest $1,000 in Nvidia Now?

Before you buy shares in Nvidia, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $814,364!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns October 7, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool holds positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

2 Huge Reasons to Buy Nvidia Stock Before 2025 was originally published by The Motley Fool