The supply of artificial intelligence (AI) servers has increased noticeably in recent years, as cloud service providers have invested enormous amounts of money in infrastructure capable of training AI models, and deploying those models for AI inference purposes. real world applications.

Market research firm TrendForce estimates that the global AI server market could generate as much as $187 billion in revenue this year, a 69% increase from 2023. Several companies are already taking full advantage of this massive end-market opportunity. From chip manufacturers such as Nvidia to custom chip makers such as Broadcom and server solution providers such as Dell Technologiesthere are multiple ways to invest in the booming AI server market.

However, in this article we will take a closer look at the prospects of Micron technology (NASDAQ:MU) And Marvell technology (NASDAQ: MRVL)two companies that make crucial components for AI servers.

There is a huge demand for Micron Technology’s high bandwidth memory chips

High-bandwidth memory (HBM) is used in AI server chips such as graphics processing units (GPUs) for its ability to enable faster data transfer to reduce processing times, improve performance, and reduce power consumption. Demand for HBM is so high that Micron says it has sold out its entire capacity for this year and next.

In fact, Micron management points out that it will have “a more diversified HBM revenue profile” by 2026 thanks to the new business it has won for its latest HBM3E chip. The chipmaker points out that it has already started shipping this new chip to its customers for approval.

Micron claims that HBM3E uses 20% less power and offers 50% more capacity compared to competing offerings. The company expects to start production of HBM3E in early 2025 and increase production as the year progresses. Better yet, Micron is confident that it will continue to gain more share in the HBM market.

Singapore-based news outlet CNA points out that Micron is reportedly aiming to capture 20% to 25% of the HBM market next year. That’s likely to give Micron’s growth a big boost next year, as the company expects HBM market revenue to rise to an impressive $25 billion by 2025, up from just $4 billion in 2023.

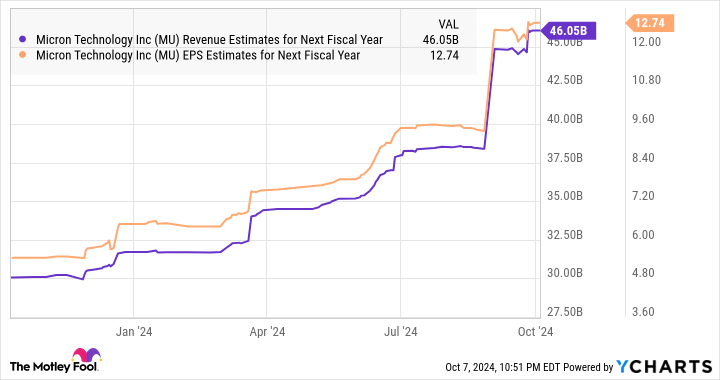

An end-market expansion along with Micron’s focus on capturing a larger share of the HBM space are the reasons why the company’s revenue is expected to rise a stunning 52% to $38 billion in the current fiscal year ( that started on August 30). . Meanwhile, analysts predict Micron’s earnings will rise to $8.94 per share from $1.30 per share last year.

Micron is expected to continue growing at a tremendous pace in the coming fiscal year.

Buying shares of Micron Technology now could be a smart move for investors looking to capitalize on the growing deployment of AI servers. The stock has a forward earnings multiple of just 11, while its price-to-earnings-growth ratio (PEG ratio) of just 0.16 further underlines that it is incredibly undervalued relative to the growth it is expected to deliver.

Marvell Technology is getting a nice boost thanks to its custom AI chips

Marvell Technology is known for manufacturing application-specific integrated circuits (ASICs), which are custom chips designed to perform specific tasks. It is worth noting that the demand for these custom chips deployed in AI servers has been increasing since major cloud service providers such as Metaplatforms, Alphabet‘s Google, and Amazon want to reduce their costs by developing internal processors.

As a result, ASICs are expected to account for 26% of the total AI server chip market by 2024. Better yet, the deployment of ASICs in AI servers is expected to increase at a nice pace in the future, opening up a potential revenue opportunity. with a value of no less than 150 billion dollars. Marvell is already taking advantage of this lucrative opportunity.

The company’s total revenue declined 5% year over year to $1.27 billion in the second quarter of fiscal 2025 (for the three months ended August 3), driven by weakness in the carrier infrastructure, consumer, automotive and corporate networks. However, it delivered a massive year-over-year increase of 92% in data center revenue to $881 million.

There’s a good chance that Marvell’s data center business will continue to grow in a healthy manner as the company’s AI chip production increases, as CEO Matt Murphy noted during the company’s latest earnings conference call:

Our custom AI silicon programs are progressing very well, with our first two chips now entering volume production. The development of new bespoke programs we have already secured, including projects with the new Tier 1 AI customer we announced earlier this year, are also following key milestones closely.

As a result, Marvell expects growth in its data center business to “accelerate sequentially into the high teens on a percentage basis” in the current quarter, which would be an improvement over the 8% sequential growth it reported in the previous quarter. This explains why Marvell’s expectations for the current quarter point to an improvement in financial performance.

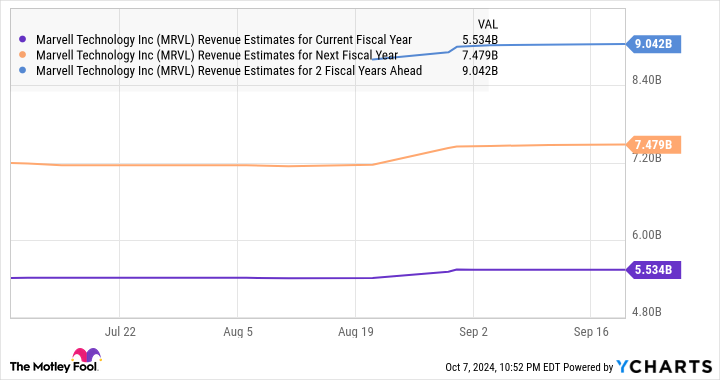

The company expects third-quarter revenue of $1.45 billion, compared to $1.42 billion in the same quarter last year. So Marvell will return to growth from the current quarter, and analysts expect this to deliver robust growth in the coming fiscal years.

Furthermore, analysts expect Marvell’s profits to grow at a compound annual growth rate of 21% over the next five years. So, investors looking to grab a semiconductor stock to capitalize on the growing demand for custom AI chips may want to consider adding Marvell Technology to their portfolios. Growth will accelerate due to the enormous opportunities in the AI server market.

Should You Invest $1,000 in Micron Technology Now?

Consider the following before purchasing shares in Micron Technology:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $826,130!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns October 7, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, former director of market development and spokeswoman for Facebook and sister of Mark Zuckerberg, CEO of Meta Platforms, is a member of The Motley Fool’s board of directors. Suzanne Frey, a director at Alphabet, is a member of The Motley Fool’s board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool holds positions in and recommends Alphabet, Amazon, Meta Platforms and Nvidia. The Motley Fool recommends Broadcom and Marvell Technology. The Motley Fool has a disclosure policy.

Artificial intelligence (AI) servers will become a $187 billion industry by 2024: two hot stocks set to rise on this huge opportunity. originally published by The Motley Fool