The S&P 500 gained 24% in 2023 and is up more than 12% so far this year. Those are significant numbers, and it’s tempting to think that these good times will continue.

Ed Yardeni, the market expert behind Yardeni Research, is optimistic, but he is also both cautious and realistic. He believes markets will continue to make gains this year, albeit at a slower pace than we have seen recently. He puts a target of 5,400 on the S&P 500 index, which suggests a gain of just 1% from current levels.

“We are still in a bull market, but from now on it will slow down. A few days ago people asked me why I didn’t increase my grades. Now I feel comfortable that I didn’t do that,” Yardeni said. He notes that bond yields are high, which is always a sign that stock prices will be low, and that yields will take a bigger hit than previously expected.

In this environment, investors will focus on defensive stocks – and that often means dividend stocks. These stocks, especially the high-yield payers, provide a reliable, inflation-reducing income stream. And if the DIV payers have also outperformed the broader markets, the potential returns are sure to pique investor interest.

We used the TipRanks platform to look up the Street-level view of two such stocks, high-yielding dividend payers – up to 11% in one case – that also boast recent outperformance and Strong Buy consensus ratings. Here are the details.

Star bulk carriers (SBLK)

We’re getting into the world of freight forwarding, specifically ocean-going bulk freight, with Star Bulk Carriers. Based in Greece, this company is the owner-operator of a fleet of dry bulk vessels. These ships, ranging from modest vessels of 500 DWT (Dead Weight Tonnage) to colossal ocean giants of over 200,000 tons, serve as the backbone of global maritime trade, carrying a range of unpackaged bulk commodities such as iron ore, coal, grains and steel products. in addition to materials such as phosphates and bauxite.

With a robust ‘on the water fleet’ consisting of 163 carriers, Star Bulk’s offering spans a variety of sizes, from the ~50,000 DWT Supramax vessels to the towering ~210,000 DWT Newcastlemax giants. The company’s most common vessels include 49 Ultramax vessels, ranging from 60,000 to 66,000 DWT, and 41 Kamsarmax vessels, with capacities from 80,000 to 83,000 DWT.

Ocean voyages take their toll on ships, and the world’s bulk carriers work hard to maintain modern fleets. In addition to the ships it has in operation, Star Bulk has eight ships under construction at shipyards in Japan, the Philippines and China. Three of these ships will be delivered in the second half of 2024, two in 2025 and the rest in 2026.

Star Bulk’s current fleet includes vessels brought in through the acquisition of Eagle Bulk Shipping. The acquisition, via a full share transaction, was completed last April. The large size of this company’s active fleet makes Star Bulk the largest dry bulk carrier traded on the NASDAQ.

Not only is Star Bulk a leader in its niche, its shares have also strongly outperformed the larger NASDAQ index this year. For the year to date, SBLK shares are up about 22%; in that same time, the NASDAQ has posted a 14% gain.

At the end of May, Star Bulk reported its first quarter 24 financial results. The company showed travel revenue of $259.39 million, up more than 15% year over year and exceeding forecasts by more than $53 million. Ultimately, the company’s non-GAAP earnings per share were reported as 87 cents per share; While this exceeded expectations by 3 cents, it was significantly higher than the non-GAAP earnings per share of 36 cents reported in the prior year quarter.

Star Bulk has a regular dividend policy, with payments based on the company’s total cash balance, the minimum cash balance per ship and the total number of ships. Based on these factors, the company announced a dividend of 75 cents per common share on May 22, significantly higher than the previous quarter. Based on the current payment, the company’s dividend yields a forward yield of 11%.

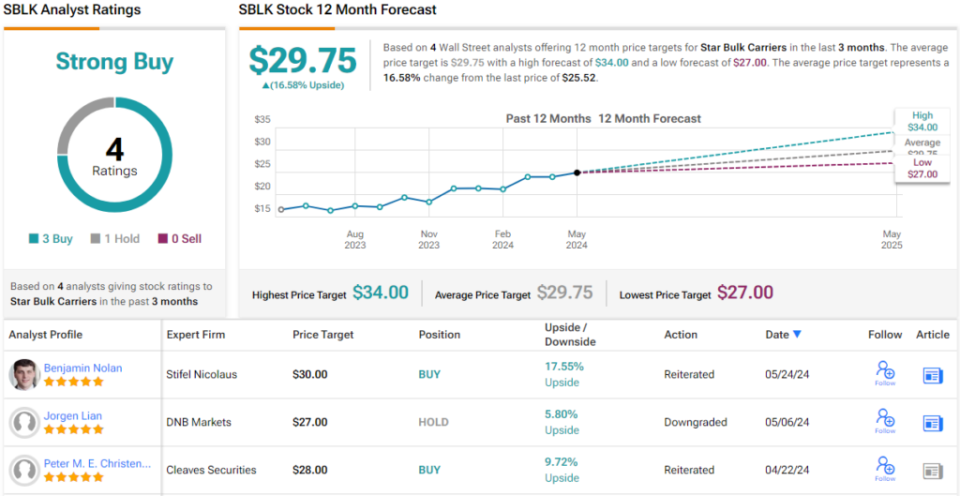

This high-yield dividend stock has caught the attention of Stifel analyst Benjamin Nolan, who ranks in the top 1% of Wall Street stock analysts according to TipRanks. Nolan is impressed with Star Bulk’s ability to expand its fleet and believes the company offers solid opportunities for investors.

“The company has begun to integrate the Eagle Bulk merger and is beginning to realize cost synergy benefits. At the same time, the dry bulk market remains healthy, supporting continued deleveraging and capital returns. We expect Star Bulk to continue to monetize older assets at higher prices while opportunistically using their shares as equity currency in dry bulk M&A transactions, similar to the Eagle deal. Ultimately, we expect market fundamentals to remain sound and SBLK stock to be the most investable of the dry bulk names,” Nolan opined.

Nolan gives a buy rating on SBLK stock and quantifies that with a target price of $30, which suggests a one-year upside potential of 17.5%. Including the dividend yield, the potential return here is close to 28.5%. (To view Nolan’s track record, click here)

Overall, there are four recent analyst ratings on this stock, and the 3-1 split in favor of Buy over Hold gives the stock a Strong Buy consensus rating. The stock is selling for $25.52 and the average price target of $29.75 implies a one-year upside of almost 17%. (To see SBLK Stock Prediction)

Frontline, Ltd. (FRO)

The next stock we’ll look at, Cyprus-based Frontline, is another shipping company, but of a very different breed than Star Bulk above. Frontline focuses on the tanker segment and operates one of the largest fleets of ocean-going tankers in the crude oil and other hydrocarbon fuel products industry. Frontline’s fleet currently consists of 82 ships in operation, including Aframax ships of 110,000 DWT, Suezmax ships of 157,000 to 158,000 DWT and, with 41 ships, the largest part of the fleet, VLCCs of 300,000 DWT.

VLCCs, or ‘Very Large Crude Carriers’, are intended solely for the transportation of crude oil. Suezmax ships, the largest that can navigate the Suez Canal, and Aframax tankers, known for their efficient transportation of crude oil around the world and access to most port facilities, complete Frontline’s diverse fleet.

Last year, in October-November, Frontline made a merger offer for Euronav, a Belgian tanker company, but ultimately withdrew this offer. Frontline sold its stake in Euronav and received $252.5 million in gross proceeds from the sale of its 13.7 million shares. However, Frontline also acquired 24 of Euronav’s 41 VLCCs, a transaction that was completed in the first quarter of this year. Measured by DWT, Frontline is now the largest pure-play tanker company on the public trading markets.

On the financial side, we note that Frontline reported a 16% year-over-year increase in revenue, to $578.4 million. Total revenues supported an adjusted profit of $137.9 million, or 62 cents per share. While revenue exceeded forecasts by nearly $195 million, non-GAAP earnings per share were 12 cents lower than expected. Still, despite the profit loss, FRO shares are up more than 41% so far this year.

The company’s earnings fully supported the common stock dividend payment. This was announced on May 29 at 62 cents per share, and the forward yield, based on the $2.48 annual payment, is 8.9%.

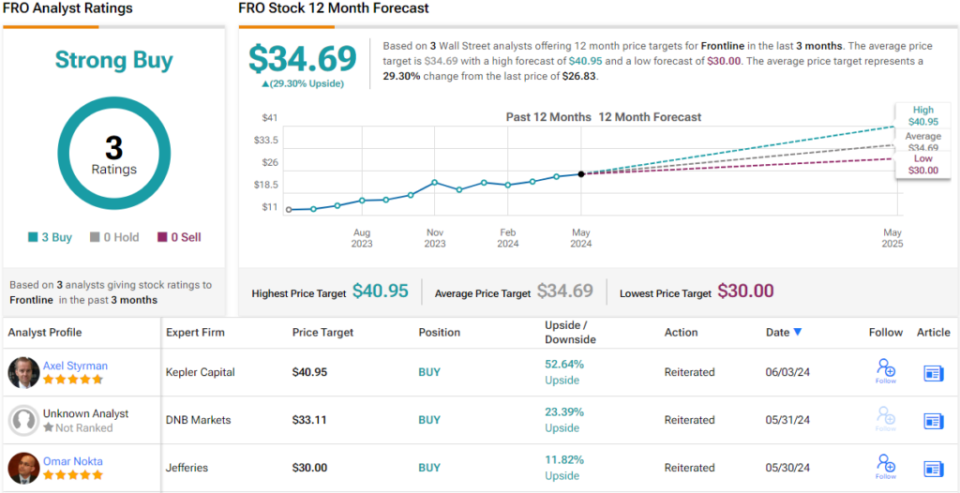

Frontline’s shares, like Star Bulk’s, have seen a remarkable rise this year, with a gain of about 36%. It has captured investors’ attention, along with one of the market’s leading analysts, Omar Nokta of Jefferies, who is ranked in the top 2% of Wall Street analysts according to TipRanks.

Explaining its Buy rating on FRO, Nokta claims: “We remain positive about the prospects for Frontline and for the tanker market in the coming years. Although the first quarter results were impacted by the repositioning, we expect the second quarter results to improve and the full impact of the Euronav fleet to be realized from the third quarter onwards. Tanker rates remain high and Frontline continues to generate significant free cash flow, with dividends a top priority.”

Along with the stock purchase, Nokta sets a $30 price target, indicating potential for a gain of nearly 12% over one year. With the dividend yield, the total return here approaches 21%. (To view Nokta’s track record, click here)

Overall, all three recent analyst reviews here are positive, making the stock’s Strong Buy consensus rating unanimous. The shares are priced at $26.83 and have an average price target of $34.69, suggesting a 29% upside in the coming year. (To see FRO stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is for informational purposes only. It is very important to do your own analysis before making an investment.

Stocks You Should Buy Now")

Stocks")