stocks to buy before 2025")

Spending on artificial intelligence (AI) infrastructure has been solid in 2024, evidenced by the massive demand for data center chips and server solutions that has driven impressive revenue and profit growth for several companies.

The good news for companies benefiting from the AI boom is that infrastructure spending in this area will continue to grow into 2025. According to Barclayshyperscale cloud companies are on track to increase their capital expenditures by 41% by 2024, followed by an estimated 15% increase next year. However, the investment bank added that the increase in investments next year could be much higher than 15%, thanks to higher spending on graphics processing units (GPUs) and custom AI chips deployed in AI servers.

Additionally, market research firm Dell’Oro Group estimates that data center infrastructure spending is on track to increase at a compound annual growth rate (CAGR) of 24% through 2028.

All this explains why investors would do well to buy shares Broadcom (NASDAQ:AVGO) And Dell Technologies (NYSE: DELL)two companies that are directly benefiting from the increase in AI-focused data center spending.

Let’s take a look at the reasons why buying these two names now could be a profitable move for 2025 and beyond.

1. Broadcom

Broadcom makes application-specific integrated circuits (ASICs), which are custom chips designed to perform specific tasks. While GPUs are currently deployed in large numbers to train large language models (LLMs) thanks to their massive parallel computing power, McKinsey estimates that ASICs will be used to run the majority of AI workloads by 2030.

That’s not surprising, since ASICs are purpose-built chips that are more power efficient compared to general-purpose computer chips like GPUs. And because they are designed to perform specific tasks, ASICs have a speed and performance advantage over general-purpose chips. This explains why JPMorgan estimates that the market for ASICs, currently worth $20 to $30 billion, could grow by more than 20% annually in the long term.

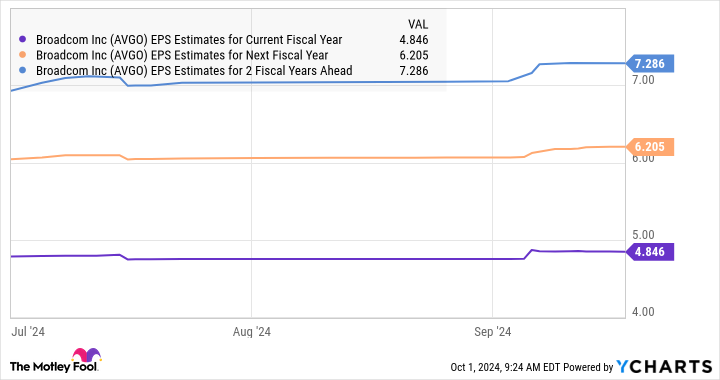

JPMorgan adds that Broadcom is the dominant player in ASICs, with an estimated market share of 55% to 60%. The company is expected to generate $12 billion in revenue this fiscal year from sales of its custom AI accelerators and Ethernet networking chips deployed in AI servers. That would be nearly triple the $4.2 billion in revenue Broadcom generated last year from selling AI chips.

The company expects to end the current fiscal year 2024 (which ends in early November) with $51.5 billion, meaning AI will account for 23% of revenue. That would be a nice improvement compared to last year, when AI accounted for 14% of sales.

Broadcom’s AI revenues are growing much faster than the market for custom AI chips, as JPMorgan previously stated. That’s because Broadcom’s networking chips are also witnessing healthy demand. The company’s network revenues rose a whopping 43% year-over-year in the previous quarter.

Broadcom management said during its September earnings conference call that sales of its Ethernet switches increased fourfold from the same period last year, thanks to demand from hyperscale customers. Investors should note that the data center switching market is getting a nice boost from AI, with Dell’Oro predicting it could double in size over the next five years and generate $80 billion in annual revenue.

As such, Broadcom appears capable of maintaining an impressive growth rate over the long term. Analysts expect corporate results to rise 20% annually over the next five years. However, they have been raising their expectations lately.

So there’s a chance that Broadcom’s earnings growth will exceed Wall Street expectations in the future. Therefore, it would be a good idea for investors to buy this AI stock before it jumps higher after an impressive 60% gain in 2024.

2. Dell Technologies

Dell is another company that has witnessed an improvement in its growth due to increased spending on AI infrastructure. More specifically, increasing demand for AI servers has been a tailwind for Dell, fueling impressive growth in the company’s Infrastructure Solutions Group (ISG), through which it sells server and storage products.

The company’s revenue in the second quarter of fiscal 2025 (which ended on August 2) rose 9% year over year to $25 billion. However, the company’s ISG business grew much faster, by 38%, and delivered record revenues of $11.6 billion. Within the ISG business, Dell said its servers and networking products witnessed a whopping 80% increase year-over-year to $7.7 billion.

The company shipped $3.1 billion worth of AI servers last quarter and received $3.2 billion in new orders from cloud service providers (CSPs). More importantly, Dell said its “AI server pipeline expanded again in the second quarter to both Tier 2 CSPs and Enterprise customers and has now grown to several multiples of our backlog.”

This is not surprising as the AI server market is witnessing excellent growth. This market could achieve annual sales growth of 18% through 2032, generating annual sales of $183 billion by the end of the forecast period. Not surprisingly, Dell said it is still in the early stages of the AI opportunity. Therefore, there is a good chance that the robust growth of its ISG business will move the needle for the company in a more meaningful way going forward.

Dell’s fiscal 2025 revenue guidance of $97 billion would represent a 10% improvement over the previous year. By comparison, the company’s revenue fell 14% in fiscal 2024. So AI has already started to improve Dell’s success, and that trend is expected to continue in the future thanks to additional AI-related opportunities in the form of the personal computer (PC) market.

All of this explains why Dell’s revenues are expected to grow nearly 11% annually over the next five years. That would be a big improvement over the 1.5% annual earnings erosion the company has experienced over the past five years.

Finally, Dell’s forward earnings multiple of just 15 makes buying the stock right now a no-brainer, as it represents a discount to the stock market. Nasdaq-100 the index’s future earnings multiple of 29 (using the index as a benchmark for technology stocks). Dell stock has posted an impressive 55% gain in 2024 and has the potential to move higher thanks to the AI-driven turnaround in its business.

Should You Invest $1,000 in Broadcom Now?

Consider the following before buying shares in Broadcom:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $752,838!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns September 30, 2024

JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool holds and recommends positions in JPMorgan Chase. The Motley Fool recommends Barclays Plc and Broadcom. The Motley Fool has a disclosure policy.

The Two Best Artificial Intelligence (AI) Stocks to Buy Before 2025 was originally published by The Motley Fool