One of the best things about putting your money on Wall Street is that there is no one-size-fits-all investment approach. With thousands of publicly traded companies and exchange-traded funds (ETFs) to choose from, there is bound to be one or more securities that can help you achieve your goal(s).

But of the countless ways to build wealth on Wall Street, few strategies have proven more consistently successful than buying and holding high-quality dividend stocks.

The appeal of dividend stocks is simple: They are almost always consistently profitable and time-tested. A company that regularly shares a percentage of its profits is one that investors rarely have to worry about when they go to sleep at night.

More importantly, dividend stocks have been crushing nonpayers in the return column for the past 50 years, according to a report released last year by the investment advisors at Hartford Funds (The Power of Dividends: Past, Present and Future) compared the performance of income stocks to nonpayers over the past half century (1973-2023). What Hartford Funds, working with Ned Davis Research, found is that income stocks more than doubled the average annual return of nonpayers — 9.17% versus 4.27% — over that period.

But that doesn’t mean investors can throw a dart at the newspaper and pick a winner. All dividend stocks are unique, and ultra-high-yielding companies (companies with yields four or more times the S&P 500) often come with additional risk. Because returns are dependent on the stock price, a company with a failing business model can “trap” income seekers with a lucrative but unsustainable return.

But not all supercharged high-yield stocks are worth avoiding. With the Federal Reserve beginning a cycle of rate cuts this week, two income stocks with truly eye-popping yields of 12.5% and 13.9% are perfectly positioned to thrive.

The light at the end of the tunnel has come for Wall Street’s most hated industry

While the term “most hated” is somewhat subjective, there is perhaps no sector that analysts have hated longer than mortgage real estate investment trusts (REITs).

Mortgage REITs are companies that seek to borrow money at lower short-term interest rates and use that capital to purchase higher-yielding long-term assets, such as mortgage-backed securities (MBSs), from which the industry gets its name. The goal of mortgage REITs is to maximize their net interest margin, which is the average return on the assets they own minus their average short-term borrowing costs.

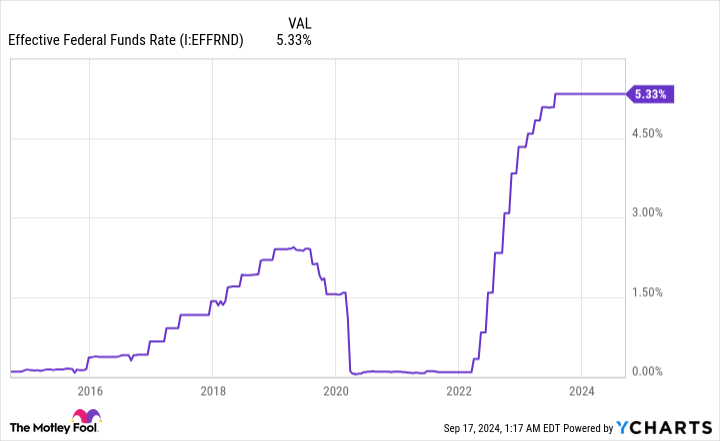

As you’ve probably gathered, the mortgage REIT industry is highly sensitive to changes in interest rates. When the nation’s central bank began its steepest rate hike cycle in four decades in March 2022, short-term borrowing costs skyrocketed. The result for the mortgage REIT industry was a shrinking net interest margin.

And it’s not just higher interest rates that the industry has to worry about. The speed of monetary policy moves matters, too. When the Federal Reserve makes slow, calculated, well-telegraphed moves, mortgage REITs have the opportunity to reposition their assets to maximize returns. But with the Fed targeting a four-decade peak in prevailing inflation, slowing the rate-hike cycle has quickly gone out the window.

The book value of virtually all publicly traded companies in the mortgage REIT sector has declined (most mortgage REITs trade at a price close to their book value) and net interest margin has declined since March 2022.

However, there is finally light at the end of the tunnel for the most hated sector on Wall Street. Annaly Capital Management (NYSE: NLY) And AGNC investment (NASDAQ: AGNC)which yield 12.5% and 13.9% respectively, now have an excellent opportunity to outperform.

Annaly and AGNC are ideally positioned to thrive during a rate cut cycle

With inflation cooling to 2.5% in August, the lowest level since February 2021, the country’s central bank had every reason to cut rates.

When the Fed moves to a dovish monetary policy and lowers the federal funds rate, it tends to lower the cost of short-term borrowing and expand the net interest margin for Annaly and AGNC Investment. At the same time, these two leading mortgage REITs have been able to buy higher-yielding MBSs over the past two years, which can further boost their respective net interest margins.

Equally important, the Fed is currently walking on eggshells with respect to monetary policy. After federal funds rates have remained at historic lows for too long and, in retrospect, have overshot due to high inflation, it is likely that the Federal Open Market Committee will delay further changes. Well-announced moves allow Annaly and AGNC to position their portfolios for optimal success.

It can be expected that a cycle of rate cuts will eventually lead to a normalization of the yield curve.

Normally, the Treasury yield curve slopes upward and to the right. This means that longer-term bonds maturing in 30 years have higher yields than Treasury bills maturing in a year or less. We recently experienced the longest yield curve inversion in history, with short-term yields far outpacing long-term bonds. When the yield curve normalizes, mortgage REITs shine.

The final piece of the puzzle for Annaly Capital Management and AGNC Investment is that they primarily invest in agency securities. An “agency” asset is an asset that is backed by the federal government in the unlikely event of default.

Annaly ended the June quarter with $66 billion of its $74.8 billion portfolio locked up in highly liquid agency assets, while AGNC had all but $1 billion of its $66 billion portfolio allocated to agency MBSs and various agency securities. The additional protection that Annaly and AGNC enjoy from agency securities allows both firms to prudently deploy their portfolios to maximize profits and preserve their outsized dividends.

While both companies have underperformed significantly in the current market boom, Annaly and AGNC appear ready for their moment in the spotlight.

Should You Invest $1,000 in Annaly Capital Management Now?

Before buying Annaly Capital Management stock, you should consider the following:

The Motley Fool Stock Advisor team of analysts has just identified what they think is the 10 best stocks for investors to buy now… and Annaly Capital Management wasn’t one of them. The 10 stocks that made the cut could deliver monster returns in the years to come.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $708,348!*

Stock Advisor offers investors an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks each month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns as of September 16, 2024

Sean Williams has positions in Annaly Capital Management. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

2 Ultra-High Yield Dividend Stocks Yielding 12% or More That Are Ideally Positioned for a Rate Cut Cycle was originally published by The Motley Fool