It’s hard to find many people complaining about the S&P500‘s strong performance in 2024. Continuing the 24% gain it posted in 2023, the index is up about 20% year to date.

But not every member of the index has done so well. PPG Industries (NYSE:PPG), SJW Group (NYSE: SJW)And Archer-Daniels-Midland (NYSE:ADM) have all fallen lower since the start of the year. PPG and SJW are down 14% and 11%, respectively, while Archer-Daniels-Midland is down 18%. As a result, all three dividend stocks – Dividend Kings, in fact – are trading at attractive valuations, presenting great buying opportunities for both value and income investors.

PPG painted a less attractive picture for 2024, but don’t let that distract you

PPG, a supplier of paints, coatings and other specialty materials, frustrated investors in July when it cut its 2024 profitability outlook. During its second-quarter 2024 earnings presentation, PPG provided a less robust adjusted earnings per share (EPS) outlook of $8.15 to $8.30 than its original adjusted earnings per share guidance of $8.34 to $8.59. To further motivate investors to hit the sell button on PPG, several analysts lowered their price targets in July.

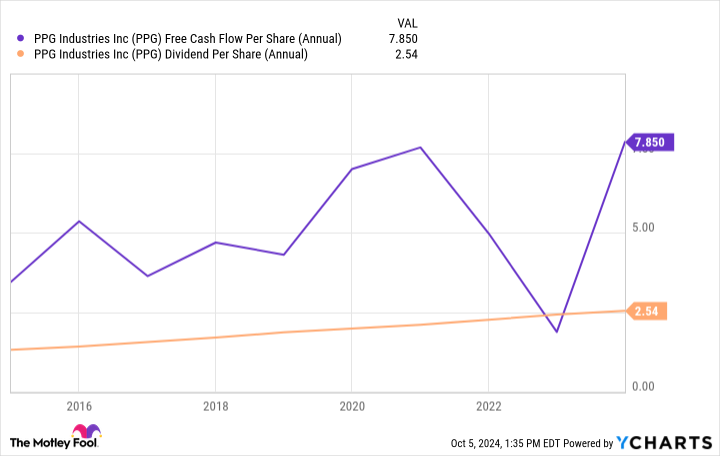

Although the summer days took a bite out of PPG stock, there’s no denying its appeal to long-term investors. First, the company has achieved a streak of 52 consecutive years of dividend increases – no small feat. And it’s not like the company has jeopardized its financial health while increasing its payouts. PPG consistently generates strong free cash flow from which it can earn its dividend.

The five-year average payout ratio of 44% further suggests that management is taking a sensible approach to returning capital to shareholders.

Dip your toes into a water business investment with SJW

Gaining even a little bit of investing experience is likely to cause some excitement. Will that excitement come from water companies like SJW Group? Probably not. And that’s fine for patient investors who want to build reliable passive income streams. There’s nothing as glamorous as leading technology stocks or exciting as innovative pharmaceutical treatments at SJW Group, which simply provides water and wastewater treatment. The water company is mainly active in regulated markets, which represented approximately 95% of net profit in 2023. As such, the company benefits from guaranteed returns, giving management excellent insight into future cash flows – foresight that helps plan capital expenditures such as acquisitions and dividend increases. SJW Group’s commitment to growth through acquisitions is clear. From 2010 to 2023, SJW Group completed more than 25 acquisitions, leading to a 72% growth in its customer base.

With 80 consecutive years of dividend payments and 56 consecutive years of dividend increases, there’s no denying that rewarding shareholders is inherent to the company’s culture, and the increases are not nominal. Over the past five years, SJW Group has increased its dividend at a compound annual growth rate of more than 6%.

Time to feast on Archer-Daniels-Midland stock

It hasn’t been a very promising start to the new year for Archer-Daniels-Midland, thanks in part to a shake-up in the C-suite, but the shares have still recovered some of their losses after falling 23% in January. Unsurprisingly, the turmoil caused by the CFO’s resignation and the audit has eroded investor confidence in the company, but this hardly suggests the shares can’t see a return to growth. With a history spanning 122 years, Archer-Daniels-Midland has overcome its share of challenges to become a leading agricultural staple, meeting the nutritional needs of both people and pets.

There’s no guarantee that the company will continue to thrive based solely on its long history, but it certainly gives investors some confidence that it has the resilience to overcome the challenges it has faced recently. Meanwhile, the appointment of a new CFO should also help the company regain investor confidence following the recent accounting investigation.

With 2024 adjusted earnings per share of $5.25 to $6.25, management expects a year-over-year decline in profitability as the company posted adjusted earnings per share of $6.98 in 2023. While this may deter short-term investors, those who have committed to buying and holding the stock for the long term need not fear.

Should you embrace these dividend darlings today?

Currently, PPG, SJW and Archer-Daniels-Midland all have attractive valuations, trading at discounts to their five-year operating cash flow multiples. For the most conservative investors, SJW and its 2.8% dividend payout shares are an excellent choice given its extensive business in regulated markets. Those who can tolerate some short-term volatility and fancy higher returns will want to look at Archer-Daniels-Midland with a forward dividend yield of 3.4%. While those interested in a specialty materials stock will want to look into PPG and its stock with a 2.1% forward yield.

Don’t miss this second chance at a potentially lucrative opportunity

Have you ever felt like you missed the boat on buying the most successful stocks? Then you would like to hear this.

On rare occasions, our expert team of analysts provides a “Double Down” Stocks recommendation for companies they think are about to pop. If you’re worried that you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: If you had invested $1,000 when we doubled in 2010, you would have $20,579!*

-

Apple: If you had invested $1,000 when we doubled in 2008, you would have $42,710!*

-

Netflix: If you had invested $1,000 when we doubled in 2004, you would have $389,239!*

We’re currently issuing ‘Double Down’ warnings for three incredible companies, and another opportunity like this may not happen anytime soon.

See 3 “Double Down” Stocks »

*Stock Advisor returns October 7, 2024

Scott Levine has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

3 Great S&P 500 Dividend Stocks Down 11% to 18% to Buy and Hold Forever originally published by The Motley Fool