Nvidia (NASDAQ: NVDA) embodies the excitement of artificial intelligence (AI), unlike any other growth stock. But what if you already own enough Nvidia, or are just looking for other options?

A good place to start is by looking at the companies Nvidia works with and that indirectly benefit from its success.

Those are three that stand out Micron technology (NASDAQ:MU), Vertiv Holdings (NYSE: VRT)And Taiwanese semiconductor manufacturing (NYSE: TSM). Here’s what makes each stock a great buy right now.

Micron provides a key ingredient in Nvidia’s new GPU

Scott Levine (Micron Technology): Of the many Nvidia partners that have the potential to prosper from a relationship with the AI juggernaut, Micron is a company that should definitely be on the radar of growth investors.

As a leader in memory and storage solutions, Micron benefited from the AI industry’s rapid growth in 2023. The new partnership with Nvidia suggests the company is extremely well positioned for future growth as the AI market continues to rise.

In February, Micron announced that it had begun large-scale production of its high-capacity memory solution, the High Bandwidth Memory 3E (HBM3E), and would ship the product in the second quarter. Micron claims the HBM3E will help “enable lightning-fast data access for AI accelerators, supercomputers and data centers.” Nvidia will use the HBM3E in its graphics processing card (GPU), the H200 Tensor Core GPU. It is not only the performance improvements that make the HBM3E attractive, but also from an economic perspective. Micron touts the HBM3E as a more cost-effective option, as it uses 30% less power than comparable products.

According to Nvidia, the H200 Tensor Core GPU doubles the memory capacity of its previous product, the H100 Tensor Core GPU, and has 1.4 times the bandwidth. With this performance improvement, Nvidia is confident that the H200 Tensor Core GPU will further facilitate the development of generative AI and large language models.

The relationship between Micron and Nvidia goes beyond the recently announced partnership. For example, in fiscal 2019, Nvidia launched the GeForce RTX graphics card for the gaming market, which relied on Micron’s memory chips.

Vertiv stock still has upside potential

Lee Samaha (Vertiv Companies): The data center equipment supplier’s inventory has soared. With a rise of 549% in the last year and 103% in 2024 alone, investors must be wondering how much longer the stock will last, not least because it trades at 41 times estimated 2024 earnings.

Yes, the valuation looks heady, but not when we are only in the very early stages of a multi-year data center investment cycle driven by AI-related investments. Vertiv’s digital infrastructure technology (power management, thermal management, rack systems, etc.) is critical to data center operations, and it is a solutions advisor or consultant partner in the Nvidia partner network.

As such, it is a crucial beneficiary of the boom in AI spending, and the company’s recent first-quarter earnings figures have demonstrated the strength of momentum in the trend. Order growth was 60% higher than in Q1 2023, and the book-to-bill ratio was 1.5x, implying significant revenue growth to come as the company expands its $6.3 billion order book further elaborated.

Wall Street has Vertiv’s free cash flow growing 22% and 25% in the years beyond 2024, and if AI spending trends continue, Vertiv should be able to grow toward its valuation. If you’re bullish on Nvidia, it makes sense to also look at Vertiv.

The hub of chip production

Daniel Foelber (Taiwan semiconductor): Taiwan Semi is betting on continued demand for chips for consumer electronics, the automotive industry, AI accelerators and more. By 2023, the chipmaker had 61% of the global chip foundry activity.

Nvidia, Broadcom, Advanced micro devices, Qualcomm, and others rely on Taiwan Semi to carry out their own designs and manufacturing to extremely precise specifications. Not to put down construction or engineering contractors, but what Taiwan Semi does is some of the most complicated manufacturing in the world. Taiwan Semi’s ability to fulfill complex orders is why companies around the world outsource their chip manufacturing to Taiwan.

Investors may want to look at Taiwan Semi as a one-stop bet on the rise of AI, electrification, data centers, and the general need for more computing power. Taiwan Semi should benefit as long as overall demand grows. It doesn’t really matter whether AMD takes market share from Nvidia or the other way around.

Despite the benefits, Taiwan Semi does have some risks, namely competition and the need to simplify supply chains and localize chip production to reduce geopolitical risk. For example, the CHIPS Act in the US would like to free up billions to increase domestic chip production. Taiwan Semi has factories in the US, but still mainly produces chips in Asia.

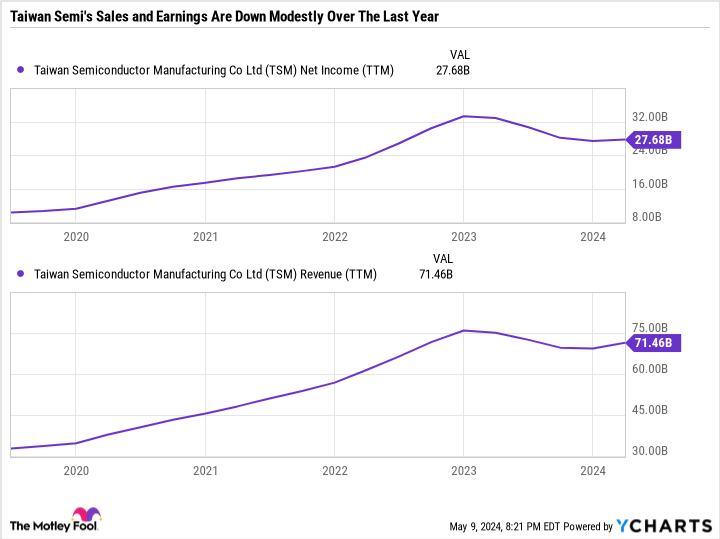

The AI tailwind is strong, but that doesn’t mean growth in the semiconductor industry is in a straight line. Apple, for example, is experiencing a slowdown due to weak demand for iPhones. Taiwan Semi’s sales and profits have leveled off recently as some of its core markets are under pressure.

The good news is that analysts expect earnings to rebound, with consensus estimates projecting earnings per share of $6.26 in 2024 and a consensus estimate for 2025 of $7.86. As a result, Taiwan Semi’s forward price-to-earnings (P/E) ratio is 22.7, compared to the current P/E of 27.2.

Despite being only 10% off its all-time high, Taiwan Semi is great value and a balanced buy for investors with the patience to weather the sector’s cyclicality. It also has a 1.4% dividend yield to top off its strong underlying investment thesis.

Should You Invest $1,000 in Micron Technology Now?

Consider the following before purchasing shares in Micron Technology:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $550,688!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns May 13, 2024

Daniel Foelber has the following options: July 2024 long calls of $180 on Advanced Micro Devices. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool holds positions in and recommends Advanced Micro Devices, Apple, Nvidia, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

3 Nvidia Partners with Explosive Growth Potential to Buy Now was originally published by The Motley Fool