Taiwanese semiconductor (NYSE: TSM) has been a brilliant investment over the last five years. The total efficiency is about 350%, which easily outperforms the NASDAQ100 and the S&P500which rose by 170% and 110% respectively.

Although TSMC has been a market-destroying stock over the past five years, I am confident it will do so again in the next five years. This makes the stock a strong buy now, and I have three reasons why it’s an attractive buy.

1. Strong sales growth

Taiwan Semiconductor’s revenue growth is expected to be strong and stable over the next five years. Several tailwinds, especially in the field of artificial intelligence (AI), are blowing in his favor.

Management believes that AI-related chips will grow at a compound annual growth rate (CAGR) of 50% through 2028, when they will account for around the low teens of total sales. That’s a strong growth rate, and much of the future growth will be driven by the 2 nanometer (nm) chip design.

Although the current generation of chips is 3nm, the gains for the next generation are impressive. When configured to maintain the same speed as a 3nm chip, the 2nm chips are expected to see a 25% to 30% efficiency improvement. With energy being a huge operating expense for data centers powering AI models, it’s no surprise that this innovation will be a hit with TSMC’s customers. Management is already seeing strong demand, which has exceeded pre-production demand of the previous 3nm and 5nm generations.

All this stems from management’s projection to grow revenue at a CAGR of 15% to 20% in the coming years. This is market-beating growth and is a key reason why TSMC will outperform the markets again in the future.

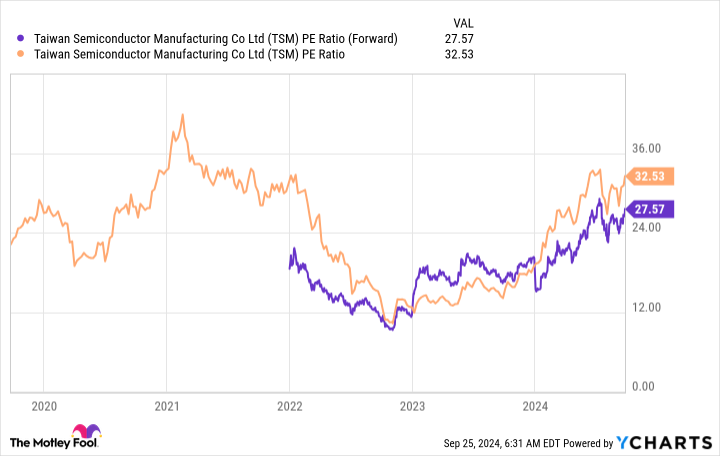

2. Attractive share price

Despite TSMC’s strong prospects, the stock doesn’t have a high price tag. Based on the rolling price-earnings ratio (P/E), Taiwan Semi is almost at the same price as five years ago. This is essential because it shows that you are not drastically overpaying for TSMC stock.

Clearly it would have been better to buy the stock in early 2023, but that price is no longer available. Instead, investors will have to pay about 27.6 times forward earnings for TSMC, but that’s not much of a premium compared to the indexes it’s compared to. By comparison, the S&P 500 and NASDAQ 100 trade at 23 and 29.2 times forward earnings. That puts TSMC at a fairly reasonable price tag compared to the broader market, which should allay investors’ fears of overpaying for the stock despite a strong two years.

3. TSMC has a growing dividend

Taiwan Semiconductor isn’t on the radar of most dividend investors, and that’s a shame. While TSMC’s payout isn’t huge, it is a sizable part of the investment picture.

The dividend is not as consistent as other stocks because TSMC’s payout is based on New Taiwan (NT) dollars, not US dollars. However, from the NT dollar point of view, management’s policy is to “maintain a sustainable and steadily increasing cash dividend, and to pay out the cash dividend every year/quarter at a level not lower than the year/quarter before.”

TSMC’s policy of increasing the dividend every year makes it an excellent dividend investment. While the yield is around 1.4%, it’s still a big part of TSMC’s investment thesis, especially if management consistently increases it.

Taiwan Semiconductor will experience strong growth over the next five years and can be purchased at a fair price. Plus, it pays a respectable dividend that is also expected to grow. TSMC is about a no-brainer of a purchase, and I expect it to easily outperform the market in the future.

Should you invest $1,000 in semiconductor manufacturing in Taiwan now?

Consider the following before buying shares in Taiwan Semiconductor Manufacturing:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $743,952!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns September 23, 2024

Keithen Drury holds positions in Taiwan Semiconductor Manufacturing. The Motley Fool holds and recommends Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

3 Reasons to Buy Taiwanese Semiconductor Stocks Like There’s No Tomorrow was originally published by The Motley Fool