There’s no doubt about that Nvidia (NASDAQ: NVDA) is currently the darling of tech investments, and for good reason. (Despite a recent decline, the stock is up 145% so far in 2024.) The company has strengthened its position as the leading chip supplier for artificial intelligence (AI) after gaining about 80% of the market. You can bet that every other semiconductor company is eager to dethrone the king.

Advanced micro devices (NASDAQ: AMD) it certainly is. The old Nvidia rival is pouring money into developing a chip that can compete with the latest offerings from its nemesis. AMD CEO Lisa Su said during a recent unveiling of the company’s latest chips, “AI is our No. 1 priority.”

If AMD is able to zoom to the top of the AI chip field, it could allow investors to experience the gains that Nvidia investors have enjoyed in recent years. But it’s a big if.

Morgan Stanley analyst Joseph Moore is among those who aren’t so sure this will happen. He recently downgraded his rating on AMD, believing there is “limited upside revision potential for AI as of now.” Ouch.

This analyst believes expectations for AMD may be too high, but take this with a grain of salt

Moore’s argument is not that AMD doesn’t benefit from it. He thinks the company will continue to see success in video game cards and will also succeed in AI, but not enough to overtake Nvidia.

This analyst’s biggest concern is that the market is setting too high expectations. The market is pricing AMD at a hefty premium and is counting on the company to significantly expand its AI chip business. The stock is trading at a price-to-earnings ratio of around 230. If we switch to the forward price-to-earnings ratio based on estimates, the valuation is more in line with Nvdia’s around 47.

But remember that analysts are not always right. In fact, they are often wrong. For every bear you’ll find a bull, and eventually one of them will be wrong, right? It is best to look at the arguments themselves and form your own opinion.

Also keep in mind that analysts change their ratings and price targets quite frequently, typically targeting a shorter investment horizon than individual investors should consider. Even if AMD fails to meet Wall Street expectations in the coming quarter, the long-term prospects could still be attractive.

AMD still has a lot to prove and will have a hard time dethroning Nvidia

I tend to agree with Moore’s main point, which is that Nvidia will remain the top dog in AI for the foreseeable future.

The difficulty AMD has in replicating what Nvidia is doing is enormous. Remember the AI chip sales expectations for 2024? $4 billion. Nvidia sold about $34 billion last year. That’s a lot of ground to cover.

If AMD wants to compete, it needs to offer something at least comparable to Nvidia, but this is an uphill battle when you’re outpaced in research and development (R&D) by such a large margin. Nvidia spent $2.7 billion on R&D last quarter, compared to $1.5 billion for AMD.

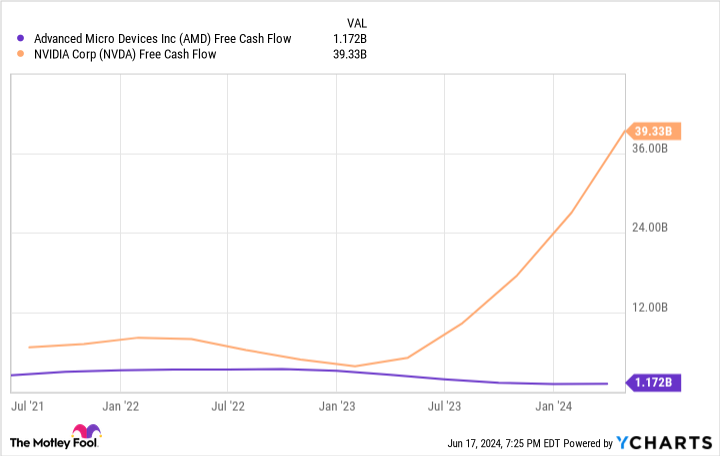

AMD, which is already spending almost 2-to-1, also doesn’t have nearly the leeway to increase this budget line the way Nvidia does. Look at this chart showing the difference in free cash flow (FCF) between the two companies. FCF is a company’s income after deducting operating costs and capital expenditures.

Nvidia could, if it wanted, spend nearly $40 billion on R&D, leaving AMD behind. That’s a pretty powerful position to be in.

This doesn’t mean that I think AMD is a bad investment; on the contrary. The AI market has the potential to be so big that it is not a zero-sum game. AMD and Nvidia can both be successful. However, I think Nvidia is the better long-term investment.

It has sufficient resources to defend its pole position. And, in my opinion, given the vision that Nvidia’s leadership has already demonstrated, Nvidia will use those ample resources to not only defend itself, but also to grow and expand its business in ways we can’t yet foresee.

Should you invest €1,000 in advanced micro-devices now?

Consider the following before purchasing shares in Advanced Micro Devices:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Advanced Micro Devices wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $723,729!*

Stock advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns June 24, 2024

Johnny Rice has no position in any of the stocks mentioned. The Motley Fool holds positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool has a disclosure policy.

Forget AMD: Nvidia is still king, according to one Wall Street analyst. What does this mean for investors? was originally published by The Motley Fool