News that high-profile activist hedge fund Elliot Investment Management has built a $1 billion position in building management and heating, ventilation and air conditioning (HVAC) companies Johnson checks (NYSE: JCI) has sent the stock higher.

While some of the moves are undoubtedly due to investors just wanting to jump on the bandwagon, it’s also a reflection of the fact that Johnson’s management could do a better job of generating value for investors. Here’s why the latter is a robust example, and the hedge fund’s move could be a positive catalyst for the stock.

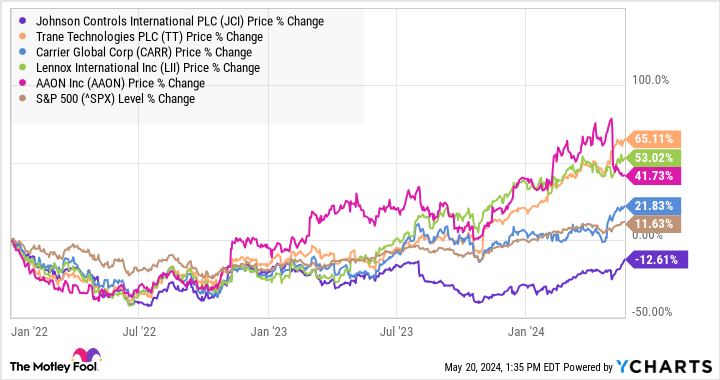

Johnson Controls is underperforming

A quick look at the company’s stock chart compared to its HVAC peers and the S&P500 says a lot. Not only has it significantly underperformed, but it has also fallen since early 2022. It was an excellent stock to buy on a dip, but not so good for long-term buy-and-hold investors.

It is surprising because the company operates in attractive end markets. The solutions help building owners achieve their net zero emissions targets by improving building efficiency. This applies to new buildings, but also to the renovation of existing buildings. Net Zero goals drive demand for Johnson Controls solutions, and the OpenBlue digital platform increases the effectiveness of smart building solutions.

Missing guidance

In summary, Johnson Controls’ management has over-promised and under-delivered in recent years, and there are also legitimate questions about its 2024 guidance.

The table below shows how the company failed to meet its initial 2022 earnings guidance and barely met its 2023 revenue growth forecast.

|

Johnson Controls Initial guidance vs. end result |

2022 Initially |

2022 Actually |

2023 Initially |

2023 Actually |

2024 Initially |

2024 Current |

|---|---|---|---|---|---|---|

|

Organic sales growth |

High-single digits |

9% |

From high single digits to low double digits |

8% |

Mid single digits |

Mid single digits |

|

Profit per share |

$3.22-$3.32 |

$3.00 |

$3.20-$3.60 |

$3.50 |

$3.65 -$3.80 |

$3.60-$3.75 |

Data source: Johnson Controls presentations.

What went wrong?

I’ll get to 2024 in a moment, but first a quick recap of what happened. In 2022, management lowered its full-year earnings guidance due to the supply chain crisis that limited the availability of semiconductor chips and other technology components, negatively impacting some of its higher-margin businesses. Sales were fine, but margins were not, hence the loss of profit in 2022.

Fast forward to 2023, management has reaffirmed its initial expectations for full-year organic sales growth of up to 10% based on second-quarter earnings. Three months later, on the third-quarter earnings call, management told investors it would expect “high single-digit” growth. The reason? Management attributed it to dealers having to reset inventory as product lead times improved. In other words, dealers previously built up inventory when Johnson Controls struggled to deliver products, but they (the dealers) are now reducing it as the company returns to delivering products on a normal schedule.

Getting worse; Johnson Controls missed sales and earnings expectations for the fourth quarter of 2024 a few months later. As noted at the time, the company was hit by a cyberattack, which was unfortunate but was not entirely responsible for the revenue and profit loss.

Johnson Controls in 2024

As the table shows, management expects full-year organic revenue growth in the mid-single digit range. However, meeting these guidelines is not an easy task. For example, organic sales growth fell 1% in the first quarter, but rose only 1% in the second quarter, and is only expected to increase by low single digits in the third quarter.

On the earnings call, Wall Street analysts wanted to know how exactly the company is meeting its full-year revenue growth ambition in light of three quarters of lackluster growth. Management argued that it needed high single-digit growth in the fourth quarter to reach the middle of the range, and 10% growth to reach the top.

Although a cyber attack occurred in the fourth quarter of last year, making this year’s comparison easier, it is still difficult to understand how Johnson Controls’ growth could soar so much in the fourth quarter.

As such, the Wall Street consensus EPS of $3.58 is below the lower end of management’s current expectations.

What it means for investors

Johnson Controls has a lot of upside potential, but management needs to start providing guidance. The pressure is on management to deliver results by 2024, and the potential for an activist investor like Elliot to push for change will only increase if the company misses its numbers again. The downside of the potential lack of full-year guidance could be mitigated by the prospect of shareholder activism to drive change. That makes the share attractive on a risk/reward basis.

So while investors should keep in mind that Johnson Controls might be overlooked, they should also be aware that good business is happening here and that there will be a potential catalyst for change if that happens.

Should you invest $1,000 in Johnson Controls International now?

Before you buy shares in Johnson Controls International, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Johnson Controls International wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns May 13, 2024

Lee Samaha holds positions at Trane Technologies Plc. The Motley Fool holds and recommends positions in Aaon. The Motley Fool has a disclosure policy.

An activist hedge fund buys this dividend stock. Time to follow? was originally published by The Motley Fool