Every day, tens of thousands of market traders trade thousands of stocks, execute millions of trades – and generate a huge stream of raw data. That data contains everything the average investor needs to know about any stock on the market – but finding it is the problem. The sheer amount of stock market information in itself is a barrier to successful investing.

This is the problem the TipRanks Smart Score is designed to solve. The Smart Score is an advanced data crunching algorithm, which uses AI and natural language processing to pan the stream of market data and extract the valuable nuggets. The algorithms scan every stock out there, compare them against a range of factors known to predict future outperformance – and then give each stock a score, a simple rating on a scale of 1 to 10, to show investors how a particular stock The stock is likely to perform well in the near future. A ‘Perfect 10’ indicates stocks that are primed for gains.

Practically speaking, we can use the Smart Score tool to find stocks that boast that Perfect 10 score – and have recently received solid ratings from the Street’s analysts. Here’s the lowdown on two of them.

Flutter entertainment (FLUTE)

We’ll start with one of the world’s largest iGaming and sports betting providers, Flutter Entertainment. This company reported a global total of 12.3 million average monthly players last year, across all its gambling and gaming brands. Flutter operates as a parent company and its fifteen brands include big names in the industry such as Paddy Power, PokerStars and Betfair.

The company’s high player count last year translated into significant revenue. The company’s total revenue in 2023 was $11.8 billion, and Flutter was able to invest $100 million in safe gambling initiatives during the year. The revenue stream came from Flutter’s four geographic divisions – US, UKI, Australia and International – with the English-speaking divisions accounting for 76% of the total global footprint. The company’s US division generated 38% of total revenue in 2023. As of 4Q23, Flutter claimed to have a 53% market share in the sportsbook segment and a 26% market share in the iGaming segment.

In its most recent quarterly report, which covers the first quarter of 24, Flutter reported quarterly revenue of $3.4 billion, a figure that was more than 16% higher than last year, but slightly below forecast, trailing by $160 million. Flutter’s cash position improved year-on-year and the company reported a strong increase in adjusted free cash flow, which came out of negative territory and rose $207 million to $157 million.

This stock’s solid position in its sector leads Oppenheimer analyst Jed Kelly to start his coverage of the stock with an optimistic outlook, noting the company’s growth potential in the US.

“We expect Flutter’s FanDuel (FD) brand to maintain its leading US market share across FLUT’s global OSB/iGaming platforms, providing players with an engaging/localized experience with industry-leading profit margins to acquire and retain more customers at higher incremental gross profit dollars compared to competitors. We believe FLUT is best positioned to navigate states that may increase taxes on online betting based on its international scale, operating experience and higher unit economics,” Kelly opined.

Kelly further explains why he believes the shares are poised to generate returns going forward, adding: “We see the recent pullback creating an attractive environment for investors, and expect multiple extensions (currently 13.6x ’25E EBITDA) of a growing US EBITDA. % ’24E-’26E CAGR and validate FD moat thesis.”

These comments support Kelly’s Outperform (i.e. Buy) rating on FLUT stock, and his $240 price target implies a potential one-year upside of 25%. (To view Kelly’s track record, click here)

It is clear from the Smart Score and analyst consensus that Oppenheimer’s optimistic view is not an outlier; the stock has 17 recent analyst ratings split into 15 Buys and 2 Holds, for a Strong Buy consensus rating. The ‘Perfect 10’ stock is currently priced at $191.70 and the average price target of $260.07 is even more bullish than Kelly’s, suggesting a ~36% one-year upside. (To see FLUT stock analysis)

Agree Energy (CHRD)

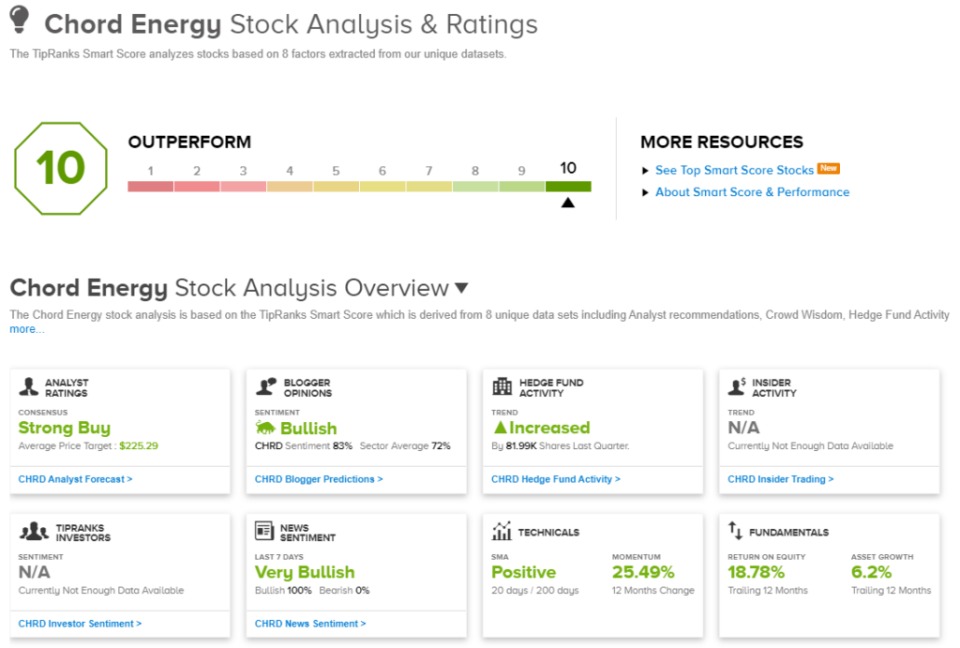

The second ‘Perfect 10’ stock we’ll look at is Chord Energy, one of the major operators in the Williston Basin of the northern Great Plains. Specifically, Chord is primarily active in the Bakken Shale, the oil-rich shale formation that extends across northern North Dakota and Montana and into Canada. The company has a net area of over 126,000 hectares in this region and has six operational platforms. Of the company’s reserves, approximately 57% are petroleum.

During the first quarter of this year, Chord achieved 99 MBblpd of crude oil production, 34.4 MBblpd of liquefied natural gas production and 209.8 MMcfpd of natural gas production. The company’s total production figure was 168.4 MBoepd, with 58.8% of that total being crude oil. The company’s total hydrocarbon revenues – from crude oil, natural gas and natural gas liquids – were $748.3 million, down 2.3% from the prior year.

Full revenue for the quarter, including purchased oil and gas sales, came in at $1.09 billion, up more than 21% year over year and more than $323 million higher than forecast. The company’s quarterly earnings per share of $4.65 were in line with expectations.

Additionally, Chord made headlines with its $4 billion strategic acquisition of Enerplus, a major Canadian independent oil and gas producer. This transaction, which was carried out in both cash and shares, was completed on May 31. The combined company has a total of 1.3 million net hectares in the Bakken Formation and a combined fourth quarter 2023 production of 287 MBoepd. Chord’s Q2 2024 report will be the first to include post-merger results.

The acquisition of Enerplus and the potential it can unlock are key points in this regard, according to BMO analyst Phillip Jungwirth. The analyst says of Chord: “We like the company’s strong FCF yield and low leverage, which enable strong capital returns… Chord completed the ~$4 billion acquisition of Enerplus, resulting in an enterprise value of ~ $12 billion, along with over a million acres of the Bakken, 10 years of inventory and ~270MBoe/d production. While integration will be a focus in the near term, we believe Chord is well-placed to further grow its Bakken footprint. This should improve relative valuation, as the stock only trades near SMID E&P peers, and at a ~0.5-1.0x discount to large-cap E&Ps.”

Looking ahead, Jungwirth gives an Outperform (i.e. Buy) rating on CHRD, and gives the stock a $230 price target that indicates a 33% upside over the next twelve months. (To view Jungwirth’s track record, click here)

Jungwirth’s colleagues also think CHRD is well positioned to deliver results. The stock has a Strong Buy consensus rating, based on a unanimous 7 Buy recommendation. The forecast is for a one-year gain of ~30%, as the average price target is currently $225.29. (To see Chord’s stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is for informational purposes only. It is very important to do your own analysis before making an investment.