A wise man once said that there is nothing new under the sun – and that has been true lately when it comes to the stock markets. Just like last year, technology stocks are leading the gains, and AI stocks are driving the tech boom.

Artificial intelligence is not a new technology – the earliest iterations date back to the 1950s – but the latest variant, generative AI, took off in late 2022. Now, companies of all stripes are starting to use gene AI as a whole. numerous new applications. Gen AI represents a new evolution in artificial intelligence technology, the ability to generate new content and materials rather than simply analyzing and synthesizing existing data. Companies that can successfully integrate gen-AI and put it into action on behalf of their customers will have an advantage in today’s environment.

This perspective aligns with Barclays’ Ryan MacWilliams’ view of AI-related businesses. In a recent research report, the analyst wrote: “We see the DevOps market as an attractive investment opportunity. In our view, DevOps is well positioned to benefit from AI-driven demand in the near term as more enterprises prioritize increasing speed of software development through investments in developer tools. We note that the IDC expects a broader DevOps market CAGR of ~36% over the 2023-2027 period. Furthermore, we believe that front-office developer roles could be among the first to return in a improving macro.”

Against this backdrop, we used the TipRanks database to examine two of MacWilliams’ top AI picks, both of which received a Strong Buy consensus rating. Let’s take a closer look at these selections.

JFrog (FROG)

The first stock we’ll look at is JFrog, a DevOps software company dedicated to providing a seamless path for both regular and invisible software updates, with the goal of providing a smooth, secure workflow directly from developers to end users. JFrog offers its customers a set of DevOps tools that are compatible with all major software technologies. The company’s platform enables users to benefit from a fully automated DevOps pipeline.

In addition to full automation, JFrog’s DevOps platform provides high levels of security and availability for the secure creation of robust production pipelines. The company’s tools are scalable, for any number of users or servers, and any storage size needed. Additionally, JFrog is compatible with hybrid systems, giving customers the flexibility to use different combinations of cloud, multi-cloud and on-prem solutions.

Recently, JFrog announced that it had entered into an agreement to acquire Qwak AI, a maker of AI and MLOps platforms. The acquisition enables JFrog to provide a unified platform solution for DevOps, Security and MLOps stakeholders, providing industry-leading unified functionality. For JFrog, the deal will enhance its machine learning capabilities and further streamline its development models. The acquisition deal is valued at $230 million.

Many tech companies operate at a loss, but that hasn’t usually been the case for JFrog. In the latest set of financial results, which covered the first quarter of ’24, operating income by non-GAAP measures was 16 cents per share. These earnings per share were derived from total revenues of $100.3 million, up more than 25% year-over-year, and more than $1.6 million better than estimates.

When we reach out to Barclays analyst MacWilliams, we find that he is bullish on JFrog, both in the short and long term. He starts his commentary by writing: “We believe FROG can benefit from the near-term improvement in cloud demand for coding workloads (thanks to generative AI) as a global leader in binary management (MSFT partnership demonstrates strategic importance).”

Looking ahead, MacWilliams adds: “Longer term, AI could accelerate cloud adoption and drive additional spending on cloud artifacts, positioning FROG as a leader in software supply chain management. Further, we believe FROG’s consumption-based pricing approach could provide additional benefits as larger AI-driven software development workflows could accelerate binary demand. As such, we believe FROG’s monetization model could be more closely correlated with higher software output as a result of AI.”

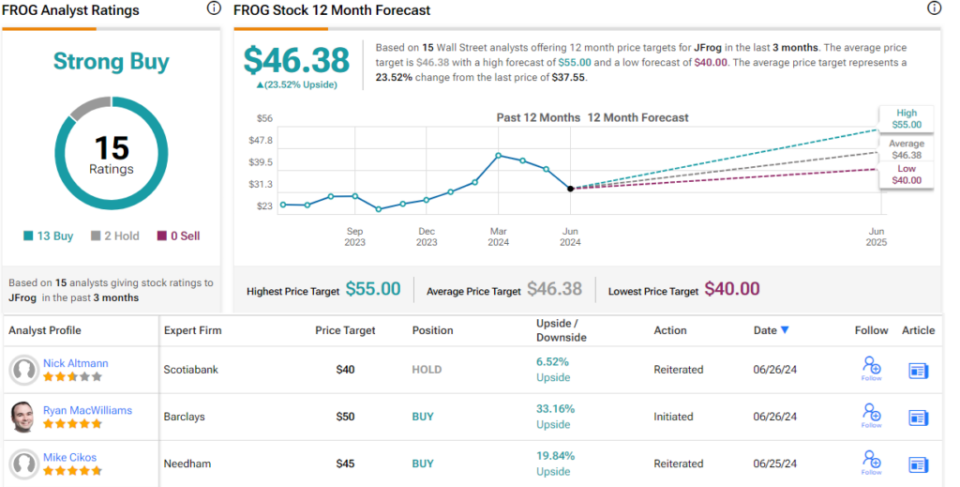

To quantify this stance, the analyst begins his coverage of FROG with an Overweight (Buy) rating and a $50 price target, implying a 33% year-over-year upside. (Click here to view MacWilliams’ track record)

Overall, the 15 recent analyst ratings, with their 13 Buys and 2 Holds, give FROG stock a Strong Buy consensus rating, while the average price target of $46.38 and current trading price of $37.55 together suggest a stock appreciation of 23.5% for the coming year. (To see JFrog’s Stock Forecast)

monday.com (MND)

Next on our list is monday.com, a cloud-based software company that develops and markets a line of popular work management software products. The company’s product lines include office systems optimization tools, CRM and project management, marketing and sales ops tools. The platform is cloud-based and is aimed at business customers on a wide range of scales. monday.com’s platform connects people and processes to bring transparency to office workflows.

Some numbers will show how popular the system is. At the end of 2023, the company had more than 225,000 customers on its books, and at the end of the first quarter of this year, it had 2,491 customers with more than $50,000 each in annual recurring revenue. This customer base is served by more than 1,900 employees worldwide, in offices as diverse as New York, Miami and Chicago; London and Warsaw; Sydney and Melbourne; Sao Paulo, Tokyo and Tel Aviv. Business customers ranging from blue chips like Coca Cola to leading technology innovators like Uber all trust monday.com.

Word processes are notoriously boring, but monday.com is bringing AI into the picture and using the technology to power its automation systems. Sort, analyze and categorize data; derive insights from textual analysis; create communication summaries; draw up action plans; even translating international communications – the company has integrated AI into its platform to streamline all these functions.

On the financial side, monday.com showed earnings of 61 cents per share by non-GAAP measures in 1Q24, beating forecasts by 21 cents. This earnings per share rose sharply on an annual basis; the result in 1Q23 was 14 cents per share. On the top line, the company brought in total revenue of $216.9 million, about $6.3 million better than expected – and up more than 33% year-over-year.

Analyst MacWilliams begins his coverage of MNDY with a bullish stance, writing: “We believe in MNDY’s greenfield opportunities and new product upsells (such as Monday Dev) within its existing customer base. This improved cross-sell movement, improving GTM efficiency and pricing advantages could boost CY25 Street estimates.”

He goes on to outline some of Monday’s strengths, adding: “MNDY recently indicated that ~1/3 of its customers were using a CRM or DevOps template by 2023 and ~10% of the Fortune 500 were using one of that uses products. Since the wide release of monday Sales CRM and Dev, both products are growing in line with faster growth than when monday.com first launched. We believe MNDY’s cross-sell move and greenfield opportunity in these markets are driving revenue growth LT will continue to replenish, and we note that CRM (~$25M in ARR as of Dec 2023) and Dev were only available to net new customers through May 2024.”

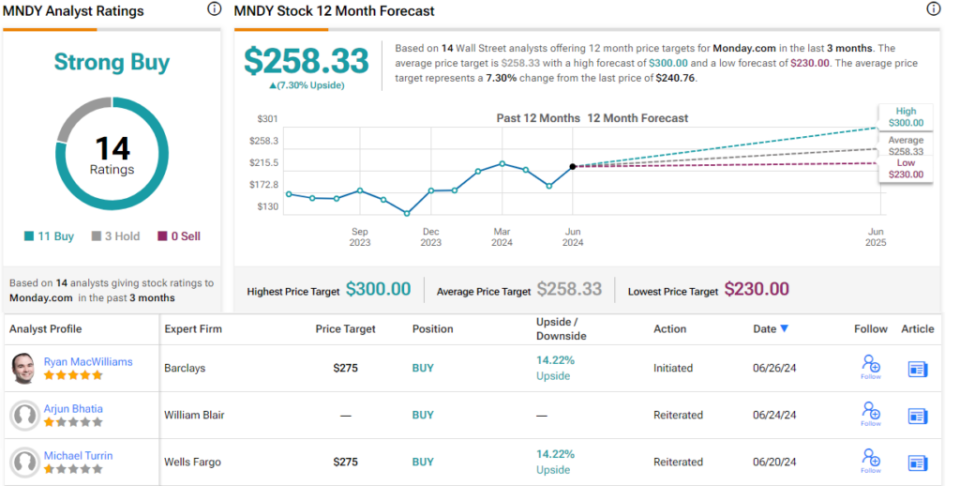

Taken together, these comments fully support MacWilliams’ Overweight (Buy) rating on MNDY stock, and his $275 price target shows his confidence in a 14% one-year upside.

This stock generally gets a lot of love on Wall Street. It has 14 recent analyst ratings with an 11-3 split favoring Buy over Hold, giving it a strong Buy consensus rating. That said, the average price target of $258.33 is slightly less bullish than Barclays’ view and implies a 7% one-year upside potential from the current share price of $240.76. (To see MNDY stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the analysts mentioned. The content is for informational purposes only. It is very important to do your own analysis before making an investment.