China has a “near monopoly” on the extraction of many raw materials crucial for the production of semiconductors and other technologies, JPMorgan said on Monday, highlighting the importance of key minerals in the escalating trade war between the US and China.

President Biden upped the ante in the ongoing feud with China last month when he targeted Chinese products with a series of new tariffs, including solar cells, electric vehicles, batteries, steel, aluminum, medical equipment and more.

“The Biden administration’s latest tariff announcement on $18 billion of Chinese imports has sparked debate over whether China’s dominance in the crucial mineral supply chain will emerge as the latest battleground for strategic competition between the US and China,” wrote Amy, executive director of strategic research at JPMorgan. Ho, and global head of research Joyce Chang, in a note to clients.

In 2022, China produced 68% of the world’s rare earth minerals, which are used for things like magnets and batteries, and 70% of the graphite, which is used in lubricants, electric motors and even nuclear reactors.

However, according to JPMorgan, China’s real dominance lies in its mineral processing capabilities. By 2022, China would process 100% of the world’s graphite supply, 90% of its rare earths and 74% of its cobalt (another crucial mineral for batteries).

“The increasing dependence on crucial minerals, which are key inputs for semiconductors, EVs, military weapons, etc., has raised concerns that China could use its dominance in this supply chain to retaliate against US industrial policies,” Ho and Chang.

The US-China trade war began in 2018, when then-President Donald Trump imposed tariffs on a range of Chinese goods and raw materials, including solar panels and steel, citing intellectual property (IP) theft and unfair trade in the country. practices. Since then, tensions between the world’s two biggest superpowers have only escalated, with a high-stakes battle over semiconductor intellectual property and manufacturing taking center stage amid the AI boom.

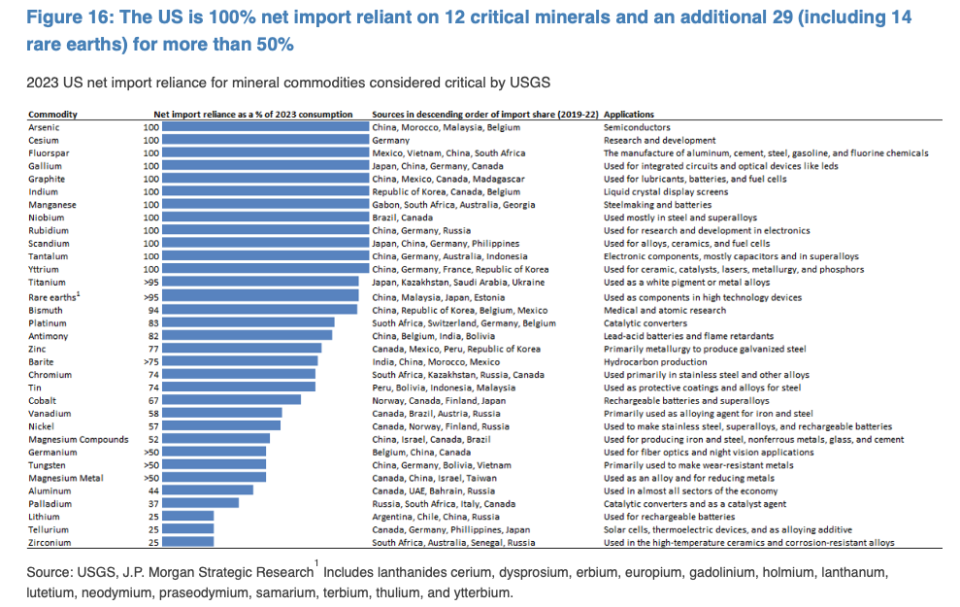

Import minerals only

Of the minerals identified by the US Geological Survey as critical to the US economy and national security, the US was 100% dependent on imports for 12 of them.

1. Arsenic

Top source: China

Applications: Semiconductors

2. Cesium

Top source: Germany

Applications: Research and development

3. Fluorspar

Top source: Mexico

Applications: Production of fuels, foams, coolants and more

4. Gallium

Top source: Japan

Applications: Integrated circuits and optical devices

5. Graphite

Top source: China

Applications: Lubricants, batteries and fuel cells

6. Indium

Top source: South Korea

Applications: Liquid crystal screens

7. Manganese

Top source: Gabon

Applications: Production of steel and batteries

8. Niobium

Top source: Brazil

Applications: Production of superalloys

9. Rubidium

Top source: China

Applications: Research and development in the field of electronics

10. Scandium

Top source: Japan

Applications: Production of alloys, ceramics and fuel cells

11. Tantalum

Top source: China

Applications: Production of electronic components, capacitors and superalloys

12. Yttrium

Top source: China

Applications: Manufacture of ceramics and lasers

China is the leading source for five of the twelve of these crucial minerals, and the second or third leading source for another three: fluorspar, galium and scandium. But China isn’t the only country the US depends on for important minerals. Mexico, Japan and Korea are among the other top sources.

The US relies on imports for 50% or more of its supply of another 29 minerals, in addition to the ten mentioned above. This includes a net import dependence of more than 90% for titanium, 14 rare earth elements and bismuth.

Will China weaponize its ‘near-monopoly’ on crucial minerals?

With the US-China trade war escalating, minerals could become an exploitable weakness for Beijing. In a worst-case scenario where China increases export restrictions on key minerals or implements a complete ban, the electronics, oil refining, defense and EV sectors would be particularly at risk, JPMorgan’s Ho and Chang noted.

Still, JPMorgan strategists do not foresee a serious mineral war happening for the time being. “There are growing concerns that China will weaponize its position, but we expect China’s response will remain proportionate and limited based on past actions,” they wrote on Monday, adding that the US could also look to alternative suppliers and substitutes to look.

The pair made some recommendations on how the US can stabilize the supply of crucial minerals to protect the defense industry, support the EV transition and avoid the economic fallout of a potential commodity trade war.

First, Ho and Chang noted that creating new U.S. mining capacity is not an option to solve U.S. dependence on mineral imports. New mining operations take years to start, they pose environmental risks, and U.S. regulatory approval is often uncertain. According to the International Energy Agency, it takes an average of 16.5 years for a U.S. mining project to go from discovery to production. And obtaining a permit for a mine alone takes an average of seven to ten years.

Instead of new mining activities, Ho and Chang recommended the diversification of mineral extraction, the implementation of new mining technologies, and the strategic stockpiling of key minerals. They estimate that technological innovation and recycling could reduce demand by 20% to 40%, while material substitution could ease supply pressure and reduce costs in coming decades. Additionally, strategic stockpiling by the U.S. government and companies could act as a buffer against sudden supply chain disruptions.

“There are more opportunities to diversify suppliers of critical minerals than there are for oil, and countries expanding their mining and processing capabilities include allies such as Canada, Australia, the EU and Japan,” it added. them to it. “The US must remain optimistic.”

This story originally appeared on Fortune.com