JD.com (JD), and China-based companies in general, used to be considered uninvestable by many. However, that sentiment is quickly changing after the Chinese central bank unleashed its monetary policy bazooka. I believe JD.com should benefit from this in the coming quarters. Overall, I’m bullish on JD stock because JD.com is an income grower and is fairly valued.

JD.com is an e-commerce company based in China. It’s not as big as Alibaba (BABA), but JD.com is still a big company with a market cap of about $62 billion.

Until recently, JD’s stock chart looked like a scary roller coaster over the past year. Still, shares are now on the rebound, and there is an apparent reason for that. All things considered, you might agree with my view that JD.com stock offers a good starting point for exposure to a potentially recovering Chinese economy.

Massive China stimulus and JD.com

China’s post-pandemic economic recovery has been uneven, and cyclical companies like Alibaba and JD.com have faced challenging conditions for several years. On the other hand, the Chinese government is now responding with a massive wave of monetary stimulus. This supports my bullish outlook, as a boost in Chinese business activity should generally provide tailwinds for JD.com’s top line and earnings numbers.

Last week was an eye-opener, as Chinese tech stocks had their best week since 2008. Before that, many global investors, according to DataTrek’s Nicholas Colas, considered Chinese stocks “almost uninvestable.” Now, however, the People’s Bank of China (PBOC) is unleashing a RMB800 billion ($114 billion) credit pool destined for China’s capital markets. This “surprise announcement of aggressive fiscal and monetary policy measures,” Colas notes, “stimulates a reappraisal” of the view that Chinese companies are uninvestable.

Billionaire David Tepper even went so far as to say that now is the time to buy “everything” in China. I’m being a bit pickier, but JD.com will undoubtedly benefit from what PBOC Governor Pan Gongsheng claims will be at least 800 billion yuan ($113 billion) in liquidity support from the Chinese government to the country’s companies. This financing could stimulate economic activity in general while facilitating share buybacks. Only time will tell how much of an impact all of this will have on JD.com specifically, but it’s easy to imagine a surge in e-commerce sales and revenue for this famous China-based company.

JD.com’s impressive income growth

Investors may wonder why JD stock is a standout opportunity among all the leading Chinese stocks. To start, I’d like to point out JD.com’s solid financial profile. The company has a respectable balance sheet with $28.8 billion in cash and minimal debt. This supports my JD bull thesis on JD stock, as I prefer investing in financially stable companies.

Another sign of financial stability is JD.com’s revenue growth. In the second quarter of 2024, JD.com grew its diluted net profit per American Depositary Share (ADS) by a whopping 97.3% year-on-year to RMB8.19 ($1.13). If you prefer adjusted (non-GAAP) measures, JD.com’s diluted net income per ADS rose 73.7% to RMB9.36 ($1.29), which is still quite impressive.

Additionally, despite recent challenging macroeconomic conditions in China, JD.com has exceeded earnings per share (EPS) expectations for more than fifteen consecutive quarters. Imagine how much better the company could do now that the Chinese government is providing major financial support to the country’s economy.

JD.com looks reasonably valued

JD shares rallied on Chinese stimulus news, but I believe there is more upside potential. The company’s price-to-earnings (P/E) ratio is very reasonable, and this is likely to appeal to many value-conscious investors looking to delve into US-listed Chinese stocks.

We can calculate JD.com’s twelve-month adjusted (non-GAAP) price-to-earnings ratio as $39.90 (the recent stock price) divided by ($0.95 + $0.75 + $0.81 + $1.33 ), or 10.39x. This compares favorably to the industry average price-to-earnings ratio of 15.28x, and to JD.com’s five-year average price-to-earnings ratio of 34.98x. That’s why I believe value seekers should definitely consider adding JD.com stock to their watchlists.

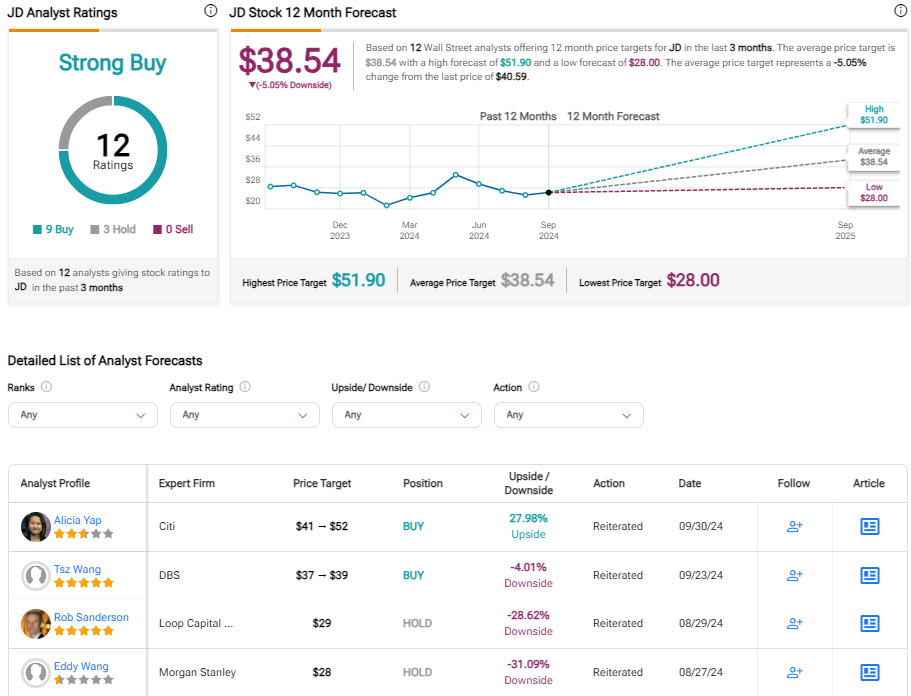

Is JD Stock a Buy According to Analysts?

On TipRanks, JD comes in as a Strong Buy, based on nine Buy and three Hold ratings assigned by Wall Street analysts over the past three months. There are currently no sales ratings. JD.com’s average price target is $38.54, not far from its last trading price.

Conclusion: Should Investors Consider JD Stock?

JD.com appears to be fairly valued despite the recent share price increase. It helps that the company’s profitability has increased. JD.com is also a cyclical e-commerce company that is poised to benefit from the Chinese government’s recently announced stimulus measures.

Analysts on average rate JD.com stock as a Strong Buy, which increases my confidence. While investing in JD stock is not without risks, I currently have a positive long-term view on JD.com.

Revelation

Disclaimer