There is no way to control the dominance of Real estate income (NYSE: O) as a net lease real estate investment trust (REIT). It is about four times larger than its nearest rival, WP Carey (NYSE: WPC). The interplay between these two REITs is interesting, though. Right now, WP Carey is trying to be more like its larger competitor, but that wasn’t always the case.

What does Realty Income do?

Realty Income owns single-tenant properties where the occupants are responsible for most of the operating costs at the property level. This is known as a net lease.

While each individual property carries a high level of risk, given that there is only one tenant, the risk of this investment approach over a sufficiently large portfolio is quite low. Realty Income is the leading net lease REIT, with a market cap of approximately $54 billion and a portfolio of more than 15,400 properties.

There are many different types of properties that can use the net lease approach. Realty Income focuses primarily on retail assets, which make up approximately 73% of rent. The remainder is split between non-retail, which is largely industrial, at 17% of rent, and a significant “other” category, which makes up the remainder. In addition to this diversification within the portfolio, Realty Income also has properties in Europe, which make up 13.5% of rent (split across different property types).

Realty Income benefits from its scale as it offers investment-grade access to capital markets (on both the debt and equity sides). It also benefits from its diversification as it has multiple growth opportunities across both property types and geographies.

While being this big suggests that future growth will be slow and steady, that’s just fine with Realty Income. The REIT has increased its dividend annually for 29 years at a rate of about 4.3% per year. With a dividend yield of about 5% today, conservative income investors should probably find it fairly attractive.

What does WP Carey do?

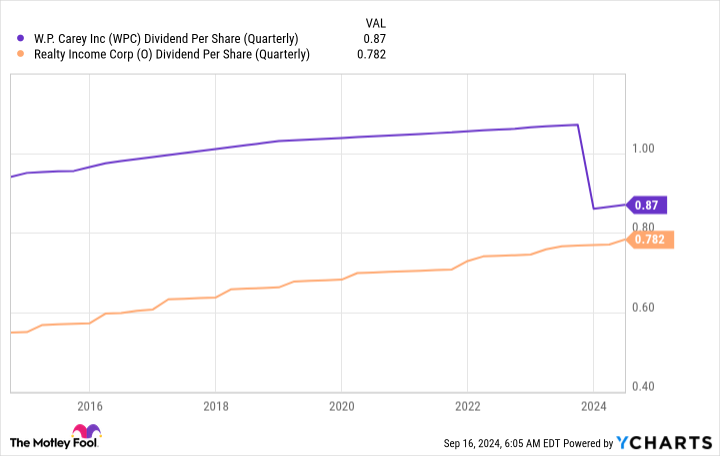

With a market cap of just under $14 billion and a portfolio of about 1,300 properties, WP Carey is the second-largest net lease REIT. It is about a quarter the size of Realty Income. The REIT’s dividend yield is 5.5%, which is a step above Realty Income and may be of interest to yield-focused investors.

Here’s the interesting thing: at one point, Realty Income tried to be like WP Carey. For over two decades, WP Carey has been investing in Europe, a region where the net lease model is still relatively new. It was only a few years ago that Realty Income expanded across the pond, trying to capitalize on a market that WP Carey had essentially helped develop.

At the time, Realty Income was imitating WP Carey, as the larger REIT looked for more ways to grow. But then Realty Income did something different: It spun off its office properties, allowing it to exit a sector that offered less potential. That’s exactly what WP Carey recently did.

But WP Carey hasn’t made the same move. Realty Income didn’t skip a beat on the dividend front, while WP Carey eventually cut its dividend after exiting the office sector. Investors were angry. Now, WP Carey’s portfolio is split 64% industrial, 21% retail and 15% “other.” Europe accounts for about 35% of rental income.

In some ways, the two portfolios are polar opposites in terms of retail versus industrial exposure, but WP Carey has been trying to grow retail lately. So after Realty Income tried to be like WP Carey by getting into Europe, it now looks like WP Carey is trying to be like Realty Income by expanding into retail.

Could WP Carey Become the Next Real Estate Income Generator?

For income investors looking at WP Carey’s higher yield, the question is whether it’s worth the risk after the dividend cut. That’s likely because the company started raising its dividend again the quarter after the cut, returning the dividend to its normal rhythm of quarterly increases. The dividend cut is probably better viewed as a dividend reset.

That said, WP Carey will likely always be heavily skewed toward the industrials sector and may never catch up to Realty Income in terms of size as the industrial giant continues to grow. But the path forward is clearly up, and thanks to the firm’s exit, WP Carey has record levels of liquidity that it plans to invest in new properties. And as long as the dividend continues to grow each year, WP Carey could be a great complement to Realty Income or, frankly, a solid standalone investment. Chasing an industrial giant, even if you don’t catch it, can lead to strong shareholder returns.

Should You Invest $1,000 in WP Carey Now?

Before you buy shares in WP Carey, you should consider the following:

The Motley Fool Stock Advisor team of analysts has just identified what they think is the 10 best stocks for investors to buy now… and WP Carey wasn’t one of them. The 10 stocks that made the cut could deliver monster returns in the years to come.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $710,860!*

Stock Advisor offers investors an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks each month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns as of September 16, 2024

Reuben Gregg Brewer has positions in Realty Income and WP Carey. The Motley Fool has positions in and recommends Realty Income. The Motley Fool has a disclosure policy.

Could WP Carey Become the Next Real Estate Income Generator? was originally published by The Motley Fool