The Federal Reserve’s long-term prospects are starting to improve. Interest rates will remain high for the time being, but the central bank is still signaling that it plans to cut spending. While GDP growth has slowed from post-pandemic highs, it has simply returned to historical norms. In short, after several years of economic headwinds, we could finally get out of the momentum.

Analyst Julian Emanuel looks at Evercore ISI’s situation and is willing to put some numbers on the positive sentiment: “The backdrop of slowing inflation, a Fed intention to cut rates and steady growth have supported Goldilocks. We are raising our price target for the S&P 500 by the end of 2024 from 4,750 to 6,000. 7,000 is possible by the end of 2025. High multiples are supported by companies’ proven track record of cost control and maintaining/growing margins.”

Emanuel’s target of 6,000 represents a year-end S&P 500 gain of ~9% from current levels. His colleagues among the Evercore stock analysts are taking that possibility into account and are choosing two stocks to capitalize on that rebound. Let’s take a closer look at them.

Ovintiv (OVV)

First on our list is an energy company, Ovintiv. The company is an exploration and production (E&P) company that takes a multi-basin approach and operates in multiple regions rather than focusing on just one region. The company’s asset portfolio includes valuable positions in several of North America’s high-value manufacturing areas. The company has interests in the Permian Basin of Texas, the Anadarko Basin of Oklahoma, the Uinta Basin of Utah and the Montney Formation that straddles the border between Alberta and British Columbia. Based on these assets, Ovintiv has worked to develop high returns through the extraction of hydrocarbon liquids, with the aim of generating free cash flows and returning money to shareholders.

As a company, Ovintiv was founded in 2020 through the restructuring of its Canadian predecessor Encana, but its roots in the energy industry go back more than a century.. Ovintiv is an innovator in horizontal drilling techniques and unconventional extraction, which has given it access to oil and gas reserves in difficult-to-reach sand and shale soils.

The company’s strategy delivered solid production numbers in the first quarter of this year, with totals at or above expectations at every product meeting. Ovintiv averaged total production volume of 547 Mboe/d in the quarter, a figure that included 211 MMbbls/d of oil and condensate, another 88 MMbbls/d of other natural gas liquids and 1,648 MMcf/d of natural gas.

That said, on the financial side, Ovintiv realized $2.35 billion on the top line, missing the forecast by $308 million. The company’s earnings, reported as earnings per share of $1.24 by GAAP measures, were 14 cents below forecast. The EPS figure was based on net income of $338 million. After capital expenditures, Ovintiv reported free cash flow of $444 million in the quarter.

For Evercore analyst Stephen Richardson, Ovintiv presents a buying proposition based on the company’s comparison to its peers and its strong production numbers. The analyst writes: “While the sector’s relative performance over the past six months tells the story, the stock remains well-positioned against SMID-cap peers in our view. After the 2023 Permian acquisitions, management achieved a process of asset integration and experienced a sharp decline curve. The initial wells drilled and completed by OVV have achieved outperformance (currently well understood by the market). In an increasingly smaller group of relevant names, looking for market opportunities to capture investor mindshare, we see that OVV continues to outperform its competitors.”

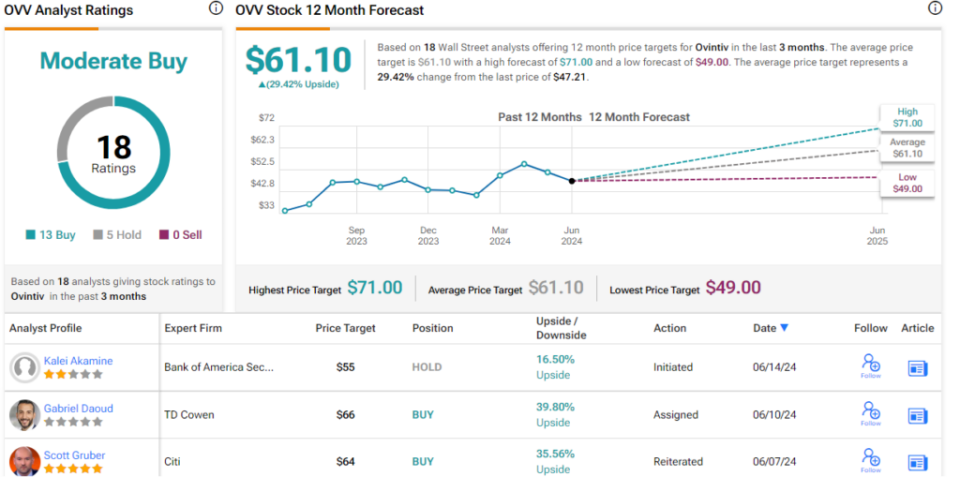

Richardson then rates these shares as Outperform (i.e. Buy) and sets a $60 price target to indicate a potential for 27% upside over the next twelve months. (To view Richardson’s track record, click here)

Overall, OVV stock gets a consensus rating of Moderate Buy, based on 18 recent reviews, including 13 Buys and 5 Holds. The stock is selling for $47.21 and the average price of $61.10 implies a one-year gain of 29.5%. (To see OVV stock forecast)

Confluent (CFLT)

The next stock we’ll look at is Confluent, a company dedicated to delivering ‘data in motion’, an essential tool for the digital business world. Confluent is a cloud-native company, built by the makers of Apache Kafka to work with that popular data processing platform. Confluent delivers a rich data experience, including extensive Kafka tutorials, and a fully managed data streaming service that is compatible with any cloud system, at any scale.

The Confluent Platform is available as a software download, enabling data storage, management and access, with continuous streaming. The tool is user-managed and integrates historical and current data streams into one centralized source.

Cloud computing has become nearly ubiquitous, and enterprise cloud users form a strong customer base, which Confluent has leveraged to achieve solid financial results. The company’s revenue has been on an upward trend for several years, and profits turned positive in the second half of 2023.

In its most recent quarter, 1Q24, Confluent generated total revenue of $217.2 million, representing a 24.6% year-over-year gain and beating forecasts by $5.36 million. Operating income, non-GAAP earnings per share, amounted to a nickel per share, 3 cents better than expected.

Several key metrics determined sales and profit figures. First quarter subscriptions rose 29% year over year to $207 million, and Confluent Cloud revenue of $107 million was up 45% year over year. And Confluent reported that it had 1,260 customers with at least $100,000 in annual recurring revenue – a total that was 17% higher than the same period last year, and that bodes well for the future.

All this caught the attention of Evercore analyst Chirag Ved, who says of Confluent: “We believe CFLT is the runaway market leader in the emerging $60 billion (and growing) data streaming market, and we are still in the early stages of companies using real-time data in their organizations as part of their data modernization and GenAI strategies. We believe the shift to Confluent Cloud and the number of underappreciated growth drivers (such as Flink and DSPs) will increase revenue to over 25% in FY25, alongside margin expansion, making CFLT a ‘Rule of 40+’ in FY26 company will become.”

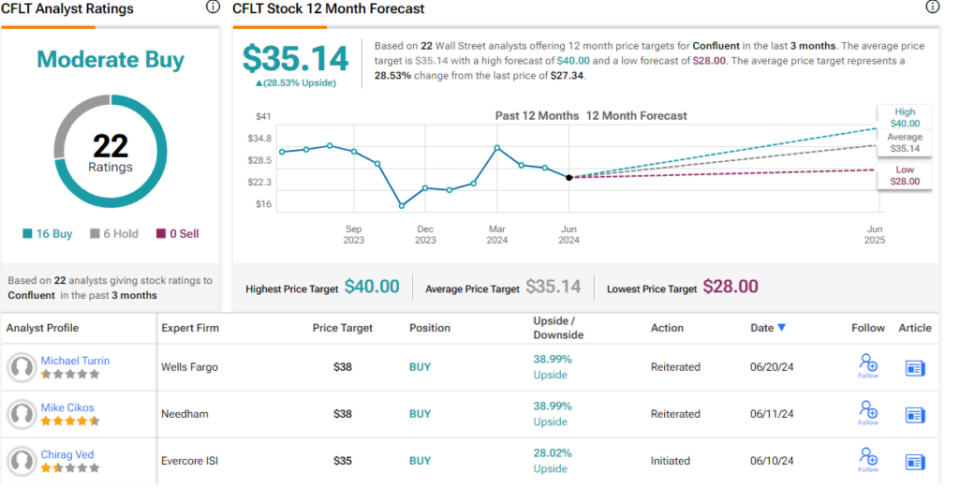

The analyst quantified his view with an Outperform (i.e. Buy) rating, and he set a $35 price target, suggesting the stock is poised for a 28% upside over a year. (To view Ved’s track record, click here)

Confluent has 22 recent analyst reviews on file, with a 16 to 6 split between Buy and Hold, giving it a consensus rating of Moderate Buy. The shares are trading for $27.34, and their average price target of $35.14 indicates that there is a 28.5% upside in store for the stock. (To see CFLT stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ stock insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is for informational purposes only. It is very important to do your own analysis before making an investment.