Elf Beauty (NYSE:ELF) is a standout in an otherwise challenging cosmetics industry. Shares of the cosmetics maker have risen 382% over the past three years, while two peers — Ulta Beauty (NASDAQ: ULTA) And Estee Lauder (NYSE: EL) — have fallen during that period.

Warren Buffetts Berkshire Hathaway took a position in Ulta Beauty earlier this year, sparking a rally in the stock. But it has since sold after reporting disappointing earnings and guidance. Meanwhile, Estée Lauder shares have fallen so far that the stock is now yielding an impressive 2.9%.

Below are the key differences between the three beauty companies and why investors might want to consider Ulta and Estée Lauder over Eleven Beauty right now.

The growth game

Elf Beauty (which stands for eyes, lips, and face) started out offering $1 cosmetics online before gaining a foothold on Goal in 2005. Since then it has expanded its product line, improved quality, raised prices and expanded its network of national and international retailers, which now includes WalmartUlta and more. Over the past 20 years, elf Beauty has carved out an enviable position in the beauty industry’s value niche.

The stock is worth about 10 times its initial public offering price less than eight years ago. In that time, it has gone from a market cap of less than $1 billion to about half that of Ulta and a quarter that of Estée Lauder. Elf Beauty deserves a lot of credit for choosing a marketing strategy that fits its affordable product line. The company doesn’t focus on hair care or fragrances, but on skin care and makeup.

Sales have grown by over 300% over the past five years, and operating profit has grown more than fivefold. By comparison, Ulta has seen respectable growth, while Estee Launder has seen flat sales and a decline in operating profit. Eleven Beauty’s sales over the past 12 months are now over $1.13 billion, while its operating margin is 12.3%, demonstrating that the company can grow while maintaining profitability.

As stellar as elf Beauty’s results have been, there are concerns that growth is slowing, which could be why the stock has fallen 31% in the past six months. It’s a much bigger company today than it was even a few years ago, which means it can’t rely as heavily on familiarity and first-time buyers.

To justify the price increases, elf Beauty must prove that its products can compete with drugstore equivalents such as L’Oreal‘s Maybelline. That’s a different selling point than when elf Beauty relied solely on discounted cosmetics.

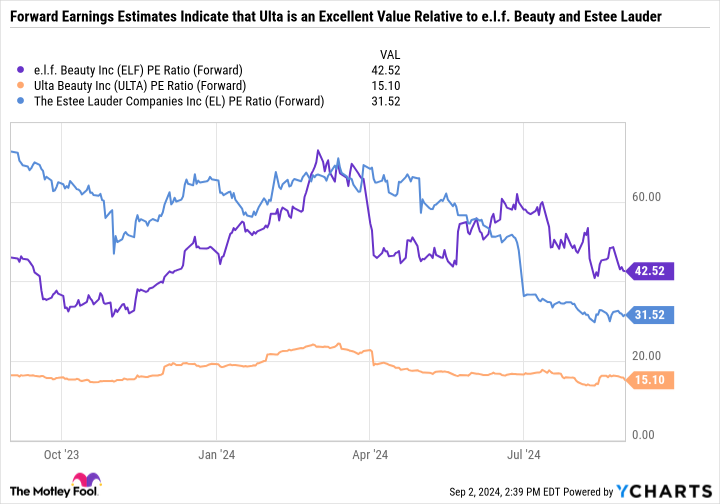

With a forward price-to-earnings (P/E) ratio of 42.5, elf Beauty is priced for perfection and will be under pressure to meet investors’ high expectations.

The Value Game

For comparison, Ulta Beauty stock is in the bargain bin with a forward P/E of just 15.1. What’s more, Ulta’s business model is very different from that of elf Beauty. The company operates brick-and-mortar stores and offers a variety of products, including its own-brand and private-label cosmetics, fragrances, hair care, bath and body products, and more.

The company also offers in-store services to give customers an additional reason to shop in person. Ulta appeals to a broad customer base by offering different product categories at different price points.

During the recent earnings call, management cited a number of challenges, including lower foot traffic, normalizing growth after years of gains, consumers switching to value, lower market share in prestige beauty and competition. CEO David Kimbell said during the second quarter earnings call:

What is unique about the current environment is the scale and pace of change. Over 80% of our stores have been impacted by one or more competitive openings in recent years, with over half impacted by multiple competitive openings. This significant portion of our store fleet is experiencing long-term impacts on sales.

Although growth is slowing, the company is still very profitable. Its proven business model and dirt-cheap valuation make it an all-encompassing way to capitalize on a boom in consumer spending and premium cosmetics.

The turnaround game

There’s no question that Estée Lauder stock has been a mess over the past few years. It rose 185% between 2019 and the end of 2021, but since then we’ve given up all those gains (and then some). This epic collapse has to do with the business model.

The company covers every category of the beauty industry, including skin care, makeup, fragrances, hair care, candles and soaps. It has a variety of established brands, including the flagship Estée Lauder, as well as Clinique, Origins, M A C, Bobbi Brown, La Mer, Aveda and more.

The company has expanded its e-commerce presence, but still relies heavily on luxury outlets, department stores, salons and spas, airports and duty-free locations. The product mix, combined with its distribution strategy and its heavy focus on China, has made Estée Lauder particularly vulnerable to a decline in consumer spending. And as Ulta said in its recent earnings call, we’re seeing a noticeable decline in demand for premium-priced products as consumers reduce discretionary spending.

When Estée Lauder is at its best, it is a high-margin cash cow that can fuel earnings and dividend growth. Lower interest rates and a rebound in discretionary spending could spark a significant turnaround in performance. But the company’s marketing strategy is in dire need of a facelift, so it will take much more than favorable economic data to return to growth.

If you buy stock now, you’re betting on what the company can do with its extremely valuable portfolio of brands, not on what it’s doing right now.

The good news is that it just needs to get back to pre-pandemic form (not even its peak performance during the pandemic). If that happens, the stock looks incredibly cheap. In the meantime, Estée Lauder’s 2.9% dividend yield provides an incentive to hold the stock during this volatile period.

Ulta and Estée Lauder are worth a closer look

Expectations and context are essential concepts in investing. Given its long-standing track record and expensive valuation, investors clearly have high expectations for elf Beauty. The company has undoubtedly benefited from consumer trends toward value products.

Similarly, Ulta Beauty and Estée Lauder are seeing slowing or even negative growth. Ulta has held up better due to its balanced product offering. Estée Lauder, on the other hand, is struggling due to a bloated business model that relies heavily on international travel and selling premium products in stores.

Now, Eleven Beauty must prove that it can succeed as a more established company at a slightly higher price. Ulta’s stock is probably the best buy right now because of its cheap valuation and balanced business model. However, investors should consider the company’s concerns about competition from other brick-and-mortar stores and the constant threat of Amazon.

Estée Lauder is a good choice for income-focused investors or those who believe it can revamp its marketing strategy and unlock margin expansion through online sales. If the company makes the necessary changes, it could be a compelling turnaround move. However, some investors may want to see concrete evidence that Estée Lauder is headed in the right direction before hitting the buy button.

Should You Invest $1,000 in Ulta Beauty Now?

Before you buy Ulta Beauty stock, here’s what to consider:

The Motley Fool Stock Advisor team of analysts has just identified what they think is the 10 best stocks for investors to buy now… and Ulta Beauty wasn’t one of them. The 10 stocks that made the cut could deliver monster returns in the years to come.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $630,099!*

Stock Advisor offers investors an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks each month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns as of September 3, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Daniel Foelber has positions in Estée Lauder Companies. The Motley Fool has positions in and recommends Amazon, Berkshire Hathaway, Target, Ulta Beauty, Walmart and elf Beauty. The Motley Fool has a disclosure policy.

Forget Eleven Beauty, This New Warren Buffett Stock And The Fallen Dividend Stocks Are Now Better Buys was originally published by The Motley Fool