Stocks to Buy Instead")

The Nvidia (NASDAQ: NVDA) The juggernaut shows no signs of stopping, as the semiconductor giant posted another set of stunning results for the first quarter of fiscal 2025 (for the three months ending April 28) on May 22, easily crushing Wall Street expectations.

While Nvidia’s revenue rose a whopping 262% year over year to $26 billion, non-GAAP profits shot up 461% to $6.12 per share. Analysts would have settled for a profit of $5.60 per share on revenue of $24.6 billion. Additionally, Nvidia has forecast fiscal second quarter revenue of $28 billion, at the midpoint of expectations, which would be more than double the $13.5 billion it posted in the year-ago period and well above the consensus estimate of 26. 6 billion dollars.

There were even more goodies in store for Nvidia investors as the company increased its quarterly cash dividend by 150% and also indicated that it will begin shipping its next-generation Blackwell chips ahead of schedule. All of this suggests that Nvidia’s hot stock market rally won’t last much longer. The stock is already up 115% through 2024, and the latest results and guidance point to more gains.

But if you’re one of those investors who missed the Nvidia gravy train and are wary of buying the stock now because of its expensive valuation – even though it might justify it – it might be a good idea to consider taking a closer look Super microcomputer (NASDAQ: SMCI) And Snowflake (NYSE: SNOW). Let’s look at the reasons why.

1. Super microcomputer

Nvidia’s phenomenal results gave server manufacturer Super Micro Computer a nice boost. That wasn’t surprising, as robust demand for Nvidia’s artificial intelligence (AI)-focused chips bodes well for Super Micro, whose server solutions are used to mount those chips in data centers.

Nvidia CFO Colette Kress pointed out during the latest earnings conference call that demand for its current and next-generation chips could exceed supply by 2025. That’s good news for Super Micro, as it should continue to see healthy demand for its AI-optimized servers. and sustain the stellar growth it has shown in recent quarters.

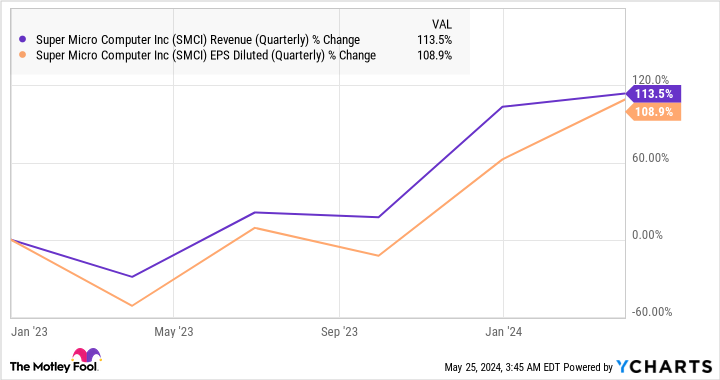

SMCI Earnings (Quarterly) Data per YCharts.

Super Micro’s revenue guidance of $14.9 billion for the current fiscal year would translate to a 110% increase from last year’s $7.1 billion. Likewise, its fiscal 2024 earnings forecast of $23.69 per share would be double last year’s level of $11.81 per share. However, it should come as no surprise that Super Micro is growing faster than currently forecast.

That’s because the company has already unveiled server solutions for Nvidia’s Blackwell chips, which will ship in the current quarter and expand as the year progresses. Reports indicate that Super Micro has already received huge orders for servers optimized to mount Blackwell processors, and is expected to meet a quarter of the demand for servers built with Nvidia’s next-gen chips.

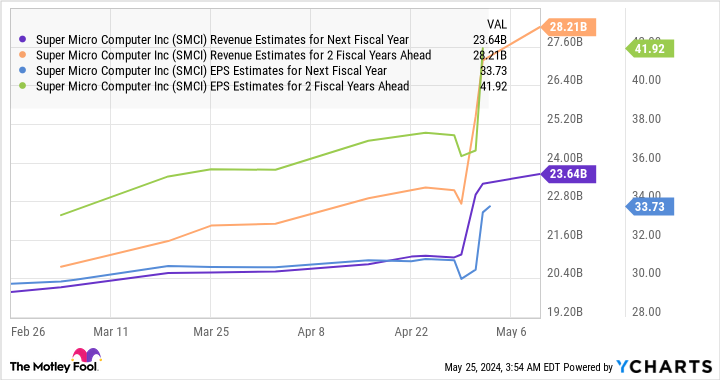

Not surprisingly, Super Micro’s revenue and revenue are expected to grow substantially in the coming financial years.

SMCI revenue estimates for next fiscal year data according to YCharts.

Super Micro’s revenue is expected to quadruple in just three years (considering it generated $7.1 billion in revenue in the previous fiscal year), while earnings could grow 3.5 times by fiscal year 2026 up from $11.81 per share in fiscal 2023. More importantly, it’s not too late for investors to buy this AI stock as it trades at an attractive 4.4x and 25x the expected profit.

Nvidia, on the other hand, has a revenue multiple of 33, along with a forward earnings multiple of 43. In fact, analysts expect Super Micro’s earnings to grow 62% annually over the next five years, giving investors yet another good reason to buy this stock to accumulate before it flies higher.

2. Snowflake

Snowflake may not be as popular an AI name as the other two companies discussed in this article. But the company, which offers a cloud-based platform that helps organizations store, organize, analyze and build applications using their proprietary data, believes AI could become the next big growth driver.

Snowflake shares have fallen by more than 21% in 2024 thanks to poor guidance and the management transition announced in February. However, the company’s first quarter fiscal 2025 results (for the three months ended April 30) suggest that AI could play an important role in driving future growth.

The company’s revenue rose 33% year over year to $829 million, easily exceeding the consensus estimate of $787 million. More importantly, the company’s second-quarter product revenue forecast of $805 million to $810 million topped the $793 million estimate and points to a year-over-year increase of 26.5% at the midpoint. The company also increased its full-year product revenue from $3.25 billion to $3.3 billion.

Snowflake’s remaining performance obligations, a measure that refers to the total value of a company’s contracts yet to be fulfilled, rose 46% year over year to $5 billion. That was faster than revenue growth, indicating the company is building a solid revenue pipeline for the future.

It appears that AI will play a central role in boosting Snowflake’s growth prospects. CEO Sridhar Ramaswamy noted in the company’s press release, “Our AI products, now widely available, are generating strong customer interest. They will help our customers deliver effective and efficient AI-powered experiences faster than ever.”

It’s worth noting that Snowflake has been aggressively investing in AI infrastructure and is looking to rapidly deploy AI-focused products to help its customers get the most out of their data. The company is also working with Nvidia to help its customers implement custom AI models for various tasks such as translation, summarization, sentiment analysis, extracting content from documents and creating generative AI-powered assistants.

In addition, Snowflake plans to strengthen its AI capabilities by acquiring TruEra, an observability platform that allows companies to monitor and evaluate the performance of large language models (LLMs) and machine learning models. Such steps should ensure that Snowflake can set itself up for stronger long-term growth, as high-quality data is important for developing robust, generative AI applications.

As such, it won’t be surprising to see Snowflake stock gaining momentum as its AI-focused moves start to pay off. The stock currently trades at 17 times sales. While that’s expensive, the sales multiple is lower than last year’s 24 and significantly cheaper than Nvidia. However, it may become more expensive in the future thanks to Snowflake’s growing AI chops, which is why it would be a good idea to buy it before it soars higher.

Should You Invest $1,000 in Super Micro Computer Now?

Before you buy shares in Super Micro Computer, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $703,539!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns May 28, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool holds and recommends positions in Nvidia and Snowflake. The Motley Fool has a disclosure policy.

Missed the Nvidia train? 2 Artificial Intelligence (AI) Stocks to Buy Instead was originally published by The Motley Fool