In the restaurant world, investors are constantly looking for what company could be next Chipotle Mexican Grill (NYSE: CMG). And for good reason: Chipotle’s stock is up more than 7,000% since its 2006 IPO.

The latest contender is Cava group (NYSE: CAVA), a Mediterranean fast-casual restaurant concept that has rapidly grown its restaurant base. The company reported strong sales growth in the first quarter.

Let’s take a closer look at Cava’s most recent earnings report and see if the stock makes sense for investors right now.

An increase in income

Cava saw revenue for its first fiscal quarter ending April 21 rise 30% to $256.3 million. Growth was aided by the company having 323 locations at the end of the period, up from 263 at the end of the first fiscal quarter a year ago. Same restaurant sales grew 2.3%, although the company said that when adjusted for holiday services, it would have seen growth of 4.3%. Cava benefited from menu price increases and mix by 3.5%, while guest traffic fell by -1.2%.

The company has faced particularly difficult comparisons as it saw same-store restaurant sales growth of 28.4% a year ago. Margins at restaurant level (RLM) decreased slightly from 25.4% to 25.2%. This metric helps measure the profitability of the restaurants, before operating expenses. Food costs as a percentage of sales fell, but labor costs rose.

The company turned to profit, with earnings per share of $0.12, compared to a loss of $1.30 a year earlier. Adjusted EBITDA, meanwhile, nearly doubled to $33.3 million. Cava also generated $38.4 million in operating cash flow in the quarter and free cash flow of $4.7 million. This is important because it shows that the company can self-fund its restaurant expansion plans, which is one of the key long-term share price drivers.

Reflecting the solid start to the year, Cava has also raised its expectations for the full year. It now expects same-store sales growth in restaurants to be between 4.5% and 6.5%, from a previous range of 3% to 5%, and for adjusted EBITDA of between $100 million and $105 million, up from compared to a previous expectation of $86 million to $92. million. Cava also increased expected restaurant openings for this fiscal year to between 50 and 54, up from a previous forecast of 48 to 52 new locations.

The company said it sees potential headwinds in traffic as the excitement surrounding last year’s initial public offering begins to fade. However, it expects to launch a new grilled steak offering to boost competition given the favorable reception the dish has had in its test markets in Boston and Dallas. Cava will also look to roll out a loyalty program by the end of the year, although its potential positive impact is not considered in current guidance. However, the rollout of steaks will be a slight headwind for restaurant-level margins.

Meanwhile, expansion plans remain on track, with locations now in 25 states and the District of Columbia. It said its recent entry into the Midwest with an opening in Chicago delivered strong results.

Time to buy the shares?

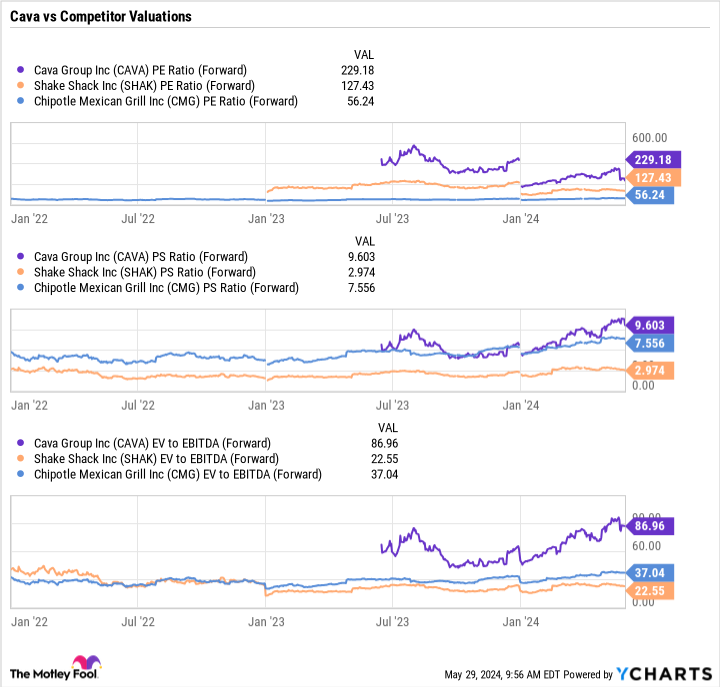

Despite a solid first quarter, Cava shares fell after the latest report. One reason could be the stock’s valuation, which, at a forward price-to-earnings (P/E) ratio of 230 times and a price-to-earnings ratio of 9.6 times, is not cheap. Even on an enterprise value to EBITDA basis, the stock trades at a hefty multiple of 87. Compared to other growing fast casual concepts like Chipotle and Shake Shackthe shares are expensive.

However, Cava has less than one-tenth the number of restaurants Chipotle currently has in the US. If the concept can remain popular and have the same appeal across the US, Cava could potentially grow to the size Chipotle has today (a market cap of almost $87 billion) in the next 15 to 20 years. Note that at the time of its IPO in 2006, Chipotle had fewer than 500 locations in 20 states.

That would mean a lot of upside potential for Cava stock, which currently has a market cap of about $9 billion. It’s not easy to project the success of a restaurant chain over the next twenty years because tastes evolve. But the ingredients are there for Cava to potentially be a big winner, despite the current expensive stock.

Should you invest $1,000 in Cava Group now?

Before buying shares in Cava Group, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Cava Group wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $671,728!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns May 28, 2024

Geoffrey Seiler holds positions in Shake Shack. The Motley Fool holds positions in and recommends Chipotle Mexican Grill. The Motley Fool recommends Cava Group. The Motley Fool has a disclosure policy.

Move on, Chipotle – Cava sees revenues rise. Time to buy the shares? was originally published by The Motley Fool