Nvidia (NASDAQ: NVDA) shares made headlines on Wednesday by becoming just the third U.S. publicly traded company to cross the $3 trillion market cap threshold. In January 2022, Apple was the first to achieve this remarkable feat, followed by Microsoft in January 2024. A growing chorus of investors believe that Nvidia will inevitably take Microsoft’s market cap crown at some point in the near future.

Let’s take a look at what has driven Nvidia stock to such dizzying heights and what investors can expect from the chipmaker in the future.

Chipmaker to the stars

Nvidia has been on fire in recent years as interest in artificial intelligence (AI) has spread like wildfire. Still, it’s important to look back, because it wasn’t that long ago that investor sentiment had turned decidedly against Nvidia. Think about this: Between November 2021 and October 2022, Nvidia shares fell more than 66% due to macroeconomic headwinds. Gamers had to make do with older graphics cards and companies were not interested in upgrading their data centers.

“This too shall pass,” goes the old saying. The arrival of generative AI in early 2023 caused a paradigm shift in technology, and investors quickly realized that Nvidia’s data center chips were at the heart of the AI revolution.

In short, generative AI is a new branch of AI that can create original content, and it is unlike anything before it. These AI models can write poems, create new songs and music, and even create digital paintings and other images. The new capabilities of these systems quickly caught the attention of technologists who realized that the same systems could be configured to compose emails, generate presentations, create charts and graphs, and even write and debug code. These skills could increase employee productivity, saving companies time and money – and the race was on.

The secret to Nvidia’s success is the parallel processing capabilities built into its graphics processing units (GPUs). In its simplest terms, parallel processing takes massive computational tasks and breaks them down into smaller, bite-sized chunks, making short work of otherwise taxing tasks. The company had already repurposed this technology to improve previous versions of AI, so Nvidia was ready when generative AI emerged.

However, these AI models, with trillions of variable bits of training data – called parameters – still require thousands of GPUs to complete the task. For example, training OpenAI’s GPT-4 required more than 25,000 of Nvidia’s top-end A100 AI processors to complete the task. Now consider that each of these A100 chips costs about $10,000, or roughly $250 million, to train just one AI model. Multiply that by all the cloud infrastructure providers, data centers and enterprise-level companies worldwide that want a piece of the AI action, and the size of the opportunity becomes clear.

An enduring track record of success

Nvidia wouldn’t be where it is today without the foresight of CEO Jensen Huang. AI is viral now, but that wasn’t the case in 2013 when the enigmatic CEO turned around Nvidia and bet the company’s future on embracing this still unproven technology.

Believing that AI was the future, Huang adapted and unleashed the parallel processing that originally produced lifelike visuals in video games to handle the rigors of AI. And the rest, as they say, is history.

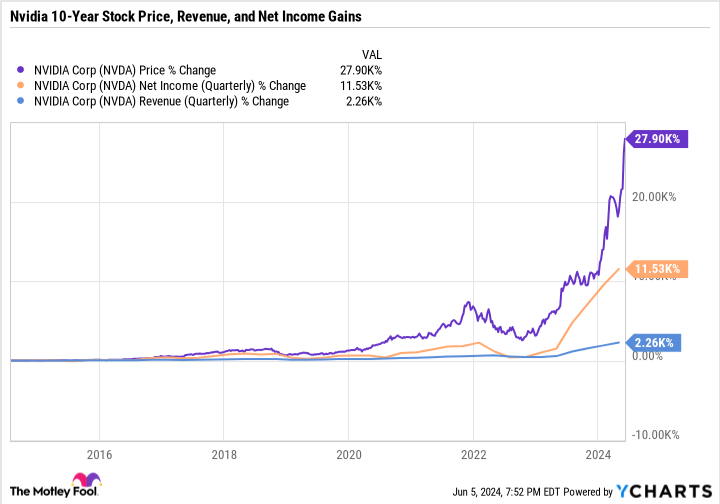

Nvidia already had a long history of success before generative AI became the sweet spot, but AI is now paying the bills. Over the past ten years, Nvidia’s revenue has increased by 2,260%, increasing its net profit by 11,530%. This has sent the stock price soaring 27,900%, and many believe the best is yet to come.

Nvidia’s meteoric rise is about to give way to a 10-for-1 stock split, which is expected to take place after the market closes on Friday. Research compiled by bank of America Analyst Jared Woodard suggests that companies that split their shares tend to gain an average of 25% in the year after the split, compared to a 12% gain for the S&P500. This is likely driven by the same operational and financial excellence that fueled the soaring stock price, resulting in a stock split.

A look at Nvidia’s most recent results paints a compelling picture. For the first quarter of 2025 (ending April 28), Nvidia’s revenue rose 262% year over year to a record $26 billion, while earnings per share shot up 629% to $5.98. Results were driven higher by the data center segment, which includes AI processors, as revenue rose 427% at $22.6 billion, fueled by rising demand for AI chips.

What this means for the future of Nvidia

In recent months, investors have begun to question the staying power of AI, with some taking a wait-and-see approach, but the resulting lesson could be costly. One of the more conservative estimates regarding the size of the generative AI market is $1.3 trillion by 2032, according to Bloomberg Intelligence. Cathie Wood, CEO of Ark Invest, is much more optimistic, suggesting a total addressable market of $13 trillion by 2030. The reality is probably somewhere in between, but the truth is that we simply don’t know how big the AI market will ultimately be.

What we do know is this. The deepest pockets of big tech are trying to develop a competitor to Nvidia’s gold standard GPU, which has had limited success so far. Additionally, Nvidia continues to invest heavily in research and development (R&D) to keep its AI processors at the cutting edge. Last year that amounted to almost $8.7 billion, or 14% of total turnover. With a lead of more than a decade and continued heavy spending on R&D, it will be difficult for its rivals to chip away at Nvidia’s leadership. That said, the competition is coming, but the size of the market suggests there could be more than one winner.

It’s also important to note that a $3 trillion market cap benchmark is completely arbitrary. Investors would be better off keeping an eye on Nvidia’s operating and financial results – which have been consistently excellent – to gain insight into the company’s continued prospects.

Finally, a comment about the rating. The rise in Nvidia’s stock price in recent years has pushed its valuation to levels that are uncomfortable for many investors. The stock is currently selling for 72 times earnings and 38 times sales, which many find egregious. However, this doesn’t take into account Nvidia’s triple-digit growth over the previous four quarters, a trajectory that is expected to continue in the current quarter. However, Nvidia’s price-to-earnings-growth ratio (PEG) – which takes that growth into account – is less than 1, the standard for a undervalued stock.

Bears will argue that the threat of competition is real, the stocks are expensive and the future of AI is unknown. That said, Nvidia is the surest way to claim the windfall that AI represents. I think this means Nvidia stock is a buy.

Should You Invest $1,000 in Nvidia Now?

Before you buy shares in Nvidia, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $713,416!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns June 3, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Danny Vena has positions at Apple, Microsoft and Nvidia. The Motley Fool holds positions in and recommends Apple, Bank of America, Microsoft and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls to Microsoft and short January 2026 $405 calls to Microsoft. The Motley Fool has a disclosure policy.

Nvidia reaches a market cap of $3 trillion ahead of its 10-for-1 stock split. This is what’s next for investors. was originally published by The Motley Fool