While there has been no shortage of the next big investing trends over the past three decades, nothing has come close to the buzz created on Wall Street when the Internet transformed corporate America in the mid-1990s. That is, until now.

For more than a year, professional and private investors have been fascinated by the game-changing potential of artificial intelligence (AI). AI involves using software and systems instead of people, and allowing these systems to learn and evolve over time without human intervention. Ideally, AI can become more proficient at repetitive tasks and possibly even learn new skills over time, which would make the technology useful in virtually every sector and industry.

Predictably, estimates of what AI has to offer are all over the place. The eye-popping prediction comes from PwC analysts who believe AI could add $15.7 trillion to the global economy by the turn of the century.

While dozens of companies are benefiting from the artificial intelligence revolution, none have seen their stock price and business performance skyrocket as instantly as semiconductor titan. Nvidia (NASDAQ: NVDA).

Nvidia once again exceeded even the highest expectations

A week ago, Nvidia lifted the lid on its first-quarter operating results (Nvidia’s fiscal year ends at the end of January) and did what it has been doing consistently for more than a year: it exceeded all Wall Street expectations. institutions and analysts.

The company’s net revenue rose a cool 262% to $26 billion from the same period last year, with its data center business leading the way. Data center revenue rose 427% year over year to $22.6 billion, with the company’s A100 and H100 graphics processing units (GPUs) leading the way.

Nvidia’s H100 GPUs in particular are the undeniable top choice of the world’s leading companies for their AI-accelerated data centers. The H100 is used to train large language models (LLMs) and power generative AI solutions on cloud infrastructure service platforms. Nvidia controls a whopping 90% of the AI-accelerated GPU market.

With demand far exceeding supply, Nvidia enjoys exceptionally strong pricing power for its chips. While the company’s cost of sales (across all segments) increased 122% from the same period last year, net sales in the first fiscal quarter increased by more than twice this rate (the recorded 262%).

Nvidia’s top line will also benefit from the supply chain issues that are starting to resolve themselves. Taiwanese semiconductor manufacturing has significantly increased its chip-on-wafer-on-substrate capacity, which should allow Nvidia to meet more orders from its customers.

The icing on the cake is that the company also announced a 10-for-1 stock split and increased the token quarterly dividend by 150%.

In the 24 hours following Nvidia’s earnings release, more than a half-dozen investment sites and Wall Street organizations called the company’s results a “blowout” in headlines. But what seemingly every investor seems to have missed is the subtle warning Nvidia gave during its conference call with its second-quarter fiscal guidance.

Nvidia’s guidelines contain a red flag that should not be ignored

For the current quarter, Nvidia expects revenue of $28 billion, plus or minus 2%, easily past the analyst consensus of about $26.66 billion. Although demand exceeds supply, Nvidia also expects a gross margin of 75.5%, plus or minus 50 basis points.

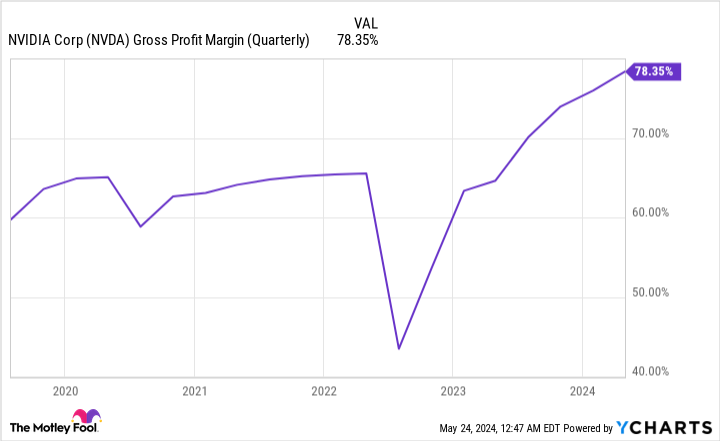

On the surface, this guidance looks great. After posting a gross margin of 64.6% in the first fiscal quarter of 2024, Nvidia’s forecast for a gross profit margin of 75.5% in the current quarter seems to show how quickly this nearly $2.6 trillion company has scaled. But there is a very casual warning here that optimists may blindly overlook.

In the quarter ended April 28, Nvidia’s gross margin was 78.35% ($20.406 billion in gross profit divided into $26.044 billion in revenue x 100). In the second quarter, the company’s gross margin is expected to decline by 235 to 335 basis points, based on Nvidia’s expectations. This may not sound like much, considering gross margin has grown roughly 13.8 percentage points in a year, but it most likely marks the arrival of two expected headwinds for the company.

First of all, Nvidia’s external competition is manifesting itself tangibly. After essentially having the high-compute GPU market to itself, Nvidia will have to contend with the launch of Intel‘S (NASDAQ: INTC) Gaudi3 AI accelerator during the third quarter, and the continued rollout of Advanced micro devices‘ (NASDAQ: AMD) MI300X GPU. Both companies have their sights squarely on competing with Nvidia’s H100 GPUs and winning over companies looking to train LLMs and exploit generative AI solutions.

Even if Nvidia’s AI GPUs remain superior in speed and computing power to AMD and Intel’s AI accelerator chips, the mere fact that this data center hardware comes to market will reduce the scarcity of AI GPU chips. This scarcity has been the fuel that has driven the price of Nvidia’s GPUs into the stratosphere. A sequential decline in gross margin of 235 to 335 basis points could signal weaker pricing power ahead.

The other problem for Nvidia that shouldn’t be ignored is that its top customers are all developing their own AI GPUs.

Microsoft, Metaplatforms, AmazonAnd Alphabet accounting for approximately 40% of Nvidia’s net sales. Meta Platforms has even increased its investment forecast for 2024, which will likely strengthen its investments in Nvidia’s AI GPUs. But now that all four are actively building and deploying internal AI accelerators for their data centers, their dependence on Nvidia’s hardware will almost certainly decrease in the coming quarters and years. This could be somewhat reflected in Nvidia’s forecasted sequential decline in gross margin.

I’d be remiss if I didn’t also note that every next-big-thing innovation or trend for three decades has endured a bubble-bursting event. Although Nvidia seems untouchable at the moment, history is unbeaten when it comes to the early phase of vibrant innovations and technologies.

Nvidia’s fiscal second quarter gross margin expectations may indicate that Nvidia stock has peaked.

Should You Invest $1,000 in Nvidia Now?

Before you buy shares in Nvidia, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns May 28, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, former director of market development and spokeswoman for Facebook and sister of Mark Zuckerberg, CEO of Meta Platforms, is a member of The Motley Fool’s board of directors. Suzanne Frey, a director at Alphabet, is a member of The Motley Fool’s board of directors. Sean Williams has positions in Alphabet, Amazon, Intel and Meta Platforms. The Motley Fool holds positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls to Intel, long January 2026 $395 calls to Microsoft, short January 2026 $405 calls to Microsoft, and short May 2024 $47 calls to Intel. The Motley Fool has a disclosure policy.

Nvidia’s “Blowout” Quarter Included a Subtle Warning Most Investors Probably Missed, originally published by The Motley Fool