Shares of Nvidia (NASDAQ: NVDA) were sold off after the company’s recent earnings report and are now down about 11% from their all-time high.

Nvidia continues to post excellent growth, with revenue up 122% in the quarter, beating analysts’ expectations. But with the stock now trading at over $3 trillion in market cap and expectations skyrocketing, Nvidia still sold off after the launch.

One reason could be concerns about the company’s gross margin. Here’s what happened to this all-important metric last quarter, and whether investors should be concerned.

Why Gross Margin Matters for Nvidia and AI Stocks

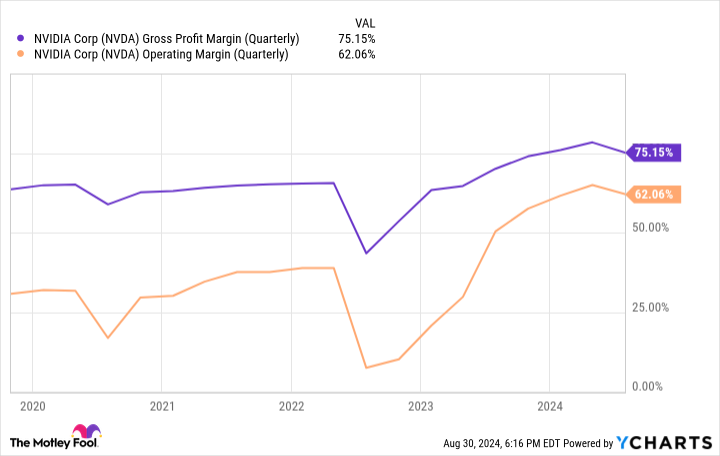

As the AI revolution took hold, cloud computing companies and large enterprises clamored for as many Nvidia data center GPUs as they could get. The mismatch between supply and demand allowed Nvidia to charge a premium for its chips even as volumes grew. As a result, gross margin grew from a range of 55% to 65% “pre-AI” to a whopping 78.4% in the company’s first quarter ended April, while operating margin grew from a range of 20% to 40% to 64.9% in the first quarter.

But as you can also see, gross and operating margins declined in the recently reported second quarter compared to Q1. Gross margin declined to 75.1%, a decline of 3.3 percentage points, and operating margin declined to 62.1%. Meanwhile, CFO Colette Kress predicted gross margin of just 74.4% in the current quarter during the conference call with analysts.

That could signal a cooling in demand or a price backlash from big customers who may be tired of paying through the nose for Nvidia chips. After all, investor concerns about cloud customers’ returns on all their AI spending led to tech stocks’ summer slump.

But Nvidia gave several reasons for the decline

Nvidia said in the press release that the gross margin decline was due to “a greater mix of new products within Data Center and inventory provisions for low-yield Blackwell materials.”

That explanation should make Nvidia shareholders feel a little better, at least for now. Nvidia’s upcoming Blackwell chip was known to be delayed slightly, due to a manufacturing error discovered late in the production and sampling process.

During the call, Nvidia noted that it has made a change to the GPU mask in its foundry, Taiwanese semiconductor production (NYSE:TSM)to improve production yields. Notably, this appears to be a minor adjustment, as CEO Jensen Huang noted that no functional changes were required to the chip. Still, there appear to be enough defects in Blackwell’s initial sampling that Nvidia had to scrap a significant amount of chips from early production at TSMC.

It’s not clear how much of the decline in gross margin was due to inventory write-downs. But the remaining margin decline was attributed to a “mix shift to new products.” This is where things get murky.

Can new products deliver the same margin?

In chip manufacturing, newer products often take time to ramp up their yields as the manufacturing process is perfected over time. But is Nvidia’s gross margin decline due to lower initial yields in manufacturing, or is Nvidia increasingly constrained in the premium it can charge for new products?

Make no mistake: the current workhorse, the H200, is undoubtedly more expensive than the H100. However, newer products are also more complicated, and therefore more expensive, for TSMC to produce.

So it’s unclear whether the remaining decline in gross margin is due to lower initial revenues (which eventually turn out higher as production ramps up) or whether Nvidia, despite charging more money for new products, can’t maintain the same margin as the selling price of newer chips gets higher and higher.

Nvidia noted that 45% of its revenue comes from cloud service providers, all of which are now pursuing their own in-house designed AI accelerators to reduce costs. Additionally, Meta platforms (NASDAQ: META)which is not a cloud service provider but likely also accounts for a large portion of Nvidia’s revenues beyond that 45%, has also started designing its own accelerators. And rival Advanced micro devices (NASDAQ: AMD) predicts revenue of more than $4.5 billion for its MI300 line of AI GPUs, which were just released this year and should keep Nvidia on its toes.

All of these companies should continue to buy Nvidia chips, though. Nvidia still makes the most advanced neutral third-party GPU chip, and since developers are already very familiar with its CUDA software, Nvidia should continue to see strong sales in the coming years.

But with its big customers pursuing their own cheaper, homegrown alternatives and more competition on the way, Nvidia will have to compete even harder. It can do that by staying ahead on the hardware front, or by lowering prices — or both.

Therefore, Nvidia investors should keep an eye on gross margin, or perhaps build in some degree of margin sacrifice in the coming years even as revenue grows.

Should You Invest $1,000 in Nvidia Now?

Before you buy Nvidia stock, here are some things to consider:

The Motley Fool Stock Advisor team of analysts has just identified what they think is the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could deliver monster returns in the years to come.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $731,449!*

Stock Advisor offers investors an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks each month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns as of August 26, 2024

Randi Zuckerberg, former chief market development officer and spokeswoman for Facebook and sister of Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Billy Duberstein and/or his clients have positions in Meta Platforms and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Advanced Micro Devices, Meta Platforms, Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Should Nvidia Investors Worry About Declining Gross Margin? was originally published by The Motley Fool