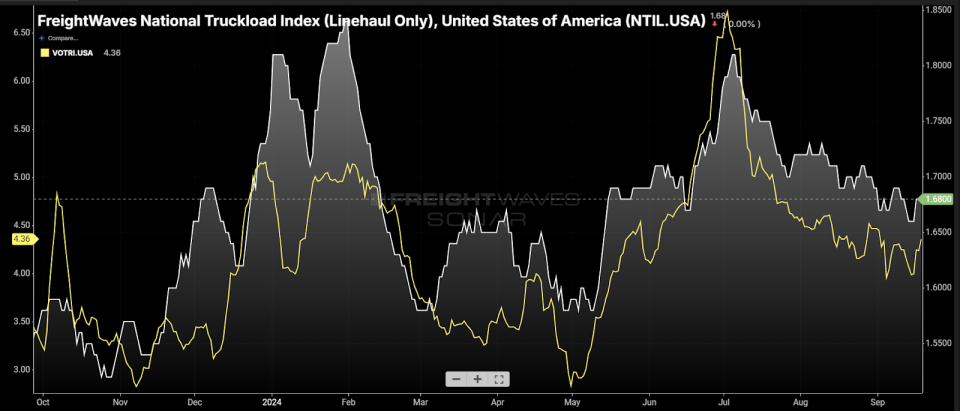

Chart of the week: National Truckload Index (scheduled transport only), Van Outbound Tender Rejection Index – USA SONAR: NTIL.USA, VOTRI.USA

Spot rates excluding total estimated fuel costs (NTIL) have fallen 3% since early August. Dry van rejection rates (VOTRI), which measure the percentage of loads that carriers cannot cover for their customers, average about 30 basis points lower. In other words, the market that appeared to be showing signs of tightening in the summer has changed course over the past quarter.

For those less familiar with the U.S. freight market, spot rates generally rise when it’s harder to find a truck that can haul the freight, and drop when it’s easier. The spot market is the Wild West of the truck market. It represents the most extreme levels of volatility and the polarized edges of the sector.

Spot rates are very useful when looking at short-term trends, but lose value when looking over multiple years due to inflation and compounding. Operating costs for carriers have increased by more than 30% over the past five years, creating invisible upward pressure on rates. Unfortunately for many airlines, they have been unable to pass on a large portion of these costs due to the extremely competitive environment. A flood of newcomers during the pandemic era is largely to blame.

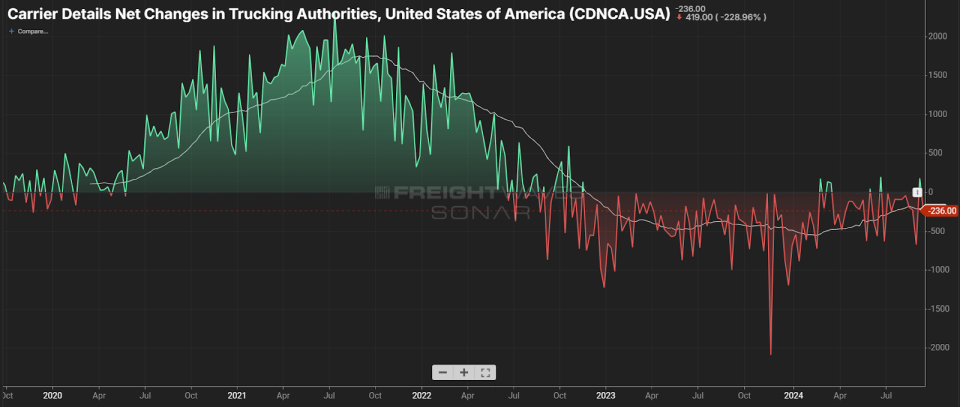

A carrier detail analysis of net changes in Federal Motor Carrier Safety Administration active operating authorities shows record 50% growth in newly registered real estate operating authority carriers from 2020 to mid-2022. This growth rate quadrupled the pace that occurred in the 2018-19 market. The result was also a strong long-term market decline, resulting in numerous airline exits.

The pandemic demand bubble for the domestic transportation market has been bursting for more than two and a half years. More than 200 carriers leave the space per week, excluding newcomers. The vast majority of these outflows are small fleets and owner-operators, consisting of fewer than five trucks and most with less than three years of experience.

So far, the deterioration in capacity has only led to some short-lived periods of mild market vulnerability.

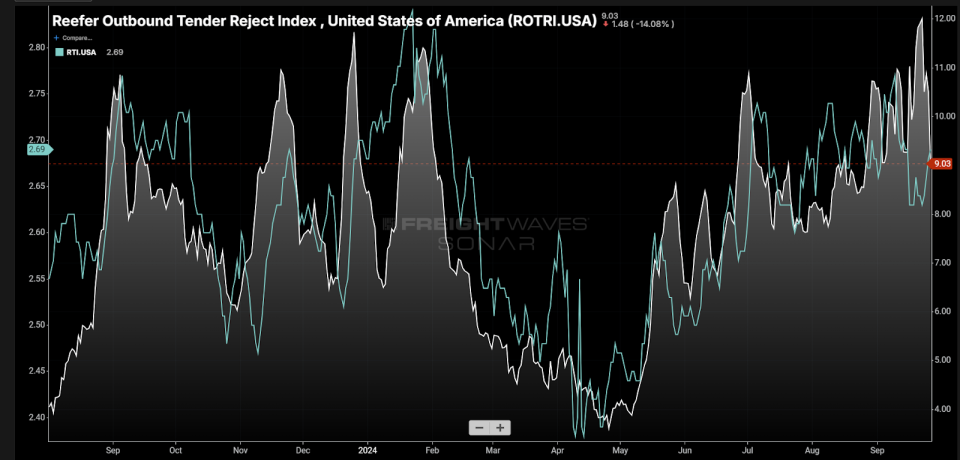

Last year’s reefer (refrigerated) truck market was the first to show signs of tightening. Spot (RTI) and rejection rates (ROTRI) rose leading up to Labor Day and rode a roller coaster into January before falling back to record lows. The reefer market has since recovered in a more sustainable manner, but has stumbled in the past week.

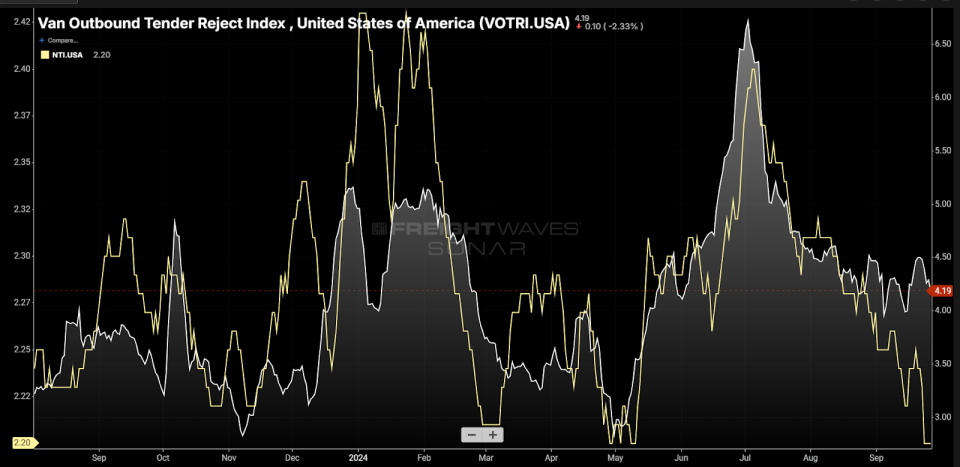

The dry van market, which represents the largest share of the truck rental market, is also having some moments. January’s Arctic air drop pushed spot and rejection rates back to Christmas levels as shippers were stuck for a few days.

Spot and rejection rates rose over the summer as an unexpected surge of imports hit the West Coast, putting pressure on carrier networks. However, there was enough capacity shortage to recover, and now the market is trending weaker after showing increasing signs of vulnerability.

Hurricanes and strikes

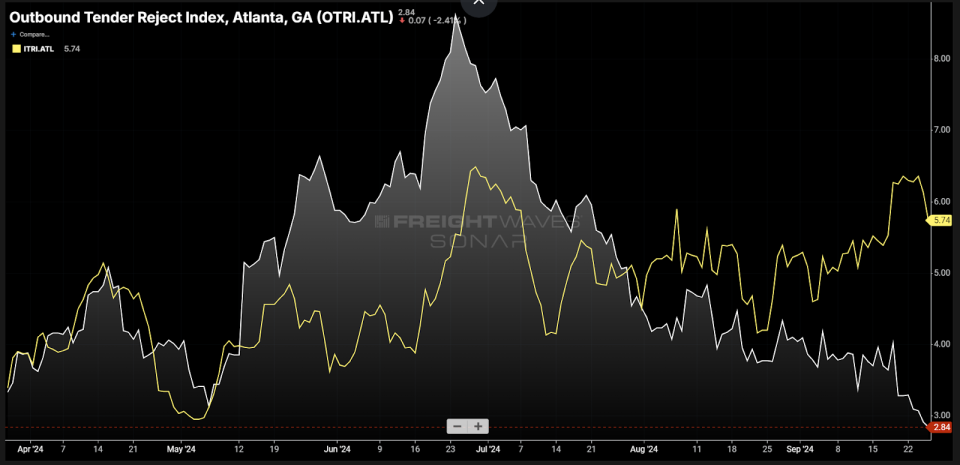

Hurricane Helene made landfall as a major Category 4 storm, with much of its infrastructure impact affecting domestic markets in the Southeast.

Outbound rejection rates in Atlanta dropped before the storm, while inbound rejection rates jumped. This could lead to some short-term disruption, but probably not a market breaker like Harvey was in 2017.

The International Longshoremen’s Association strike also has some potential depending on whether it happens and for how long, but many shippers have been preparing for this for several months.

Is this the new normal?

The possible good news for transportation service providers is that even though the spot market has collapsed and many of the short-term disruptive events have dissipated, rejection rates are still higher over the course of a year. The likelihood of a sustained market turnaround this fall has diminished, but that doesn’t eliminate the possibility of a strong shift in 2025.

Capacity decreases at the fastest rate during winter. If this trend continues and the market remains weak during the holiday season, the likelihood of a severe supply shock increases significantly.

This market is by definition not sustainable. It will shift. The fact that capacity continues to rise at record levels indicates that supply is trending toward demand on the curve. The timing is always the most challenging thing to predict and the shift will likely occur when many have let down their guard.

And who can blame them, because this has been the longest and most severe freight recession in modern times.

About the chart of the week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A map is chosen from thousands of potential maps on SONAR to help participants visualize the freight market in real time. Each week, a market expert will post a chart, along with commentary, live on the front page. The Chart of the Week will then be archived on FreightWaves.com for future reference.

SONAR collects data from hundreds of sources, presents the data in graphs and maps, and provides real-time commentary on what freight market experts want to know about the industry.

FreightWaves’ data science and product teams release new data sets every week and improve the customer experience.

Click here to request a SONAR demo.

The post The green shoots in the freight market are fading towards October appeared first on FreightWaves.