PepsiCo (NASDAQ: PEP) is best known for its soft drink products and snack options under the Frito-Lay brand. It is a powerful partner if retailers want to attract customers to their stores. And the company just got a little better after announcing plans to buy Siete Foods for $1.2 billion, even though Wall Street barely noticed the deal. This is why the acquisition is so important.

What does PepsiCo do?

PepsiCo’s name suggests that it is a beverage maker, and it is. But it’s so much more than that. It’s truly a food conglomerate, with brands ranging from drinks (Pepsi) to salty snacks (Frito-Lay) to packaged foods (Quaker Oats). And those are just some of the iconic brands; it also owns Gatorade, Doritos, Tostitos, Muscle Milk, Smartfood and Near East, among others. It is an essential partner for retailers and convenience stores around the world.

The size of the company is impressive, with a market capitalization of approximately $230 billion. Revenues in 2023 were approximately $91.5 billion. You can find the brands in more than 200 countries and territories around the world. Its distribution and marketing strength is exceptional and it is easily one of the largest and most powerful companies on Wall Street in the consumer goods sector.

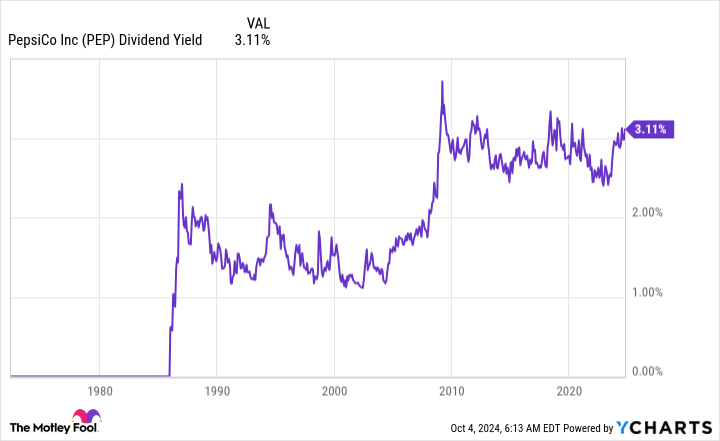

Investors should find the company very attractive overall. But right now it also looks quite attractive in terms of valuation. PepsiCo’s price-to-sales, price-to-earnings, price-to-book and price-to-cash flow ratios are all below their five-year averages. The stock’s 3.2% dividend yield is at the high end of its historical yield range. The return is also significantly higher than the 2.6% average return of the consumer staples sector Consumer Staples Select Sector SPDR ETF (NYSEMKT: XLP) as a sector proxy. Simply put, PepsiCo looks reasonably priced, if not a little cheap, right now.

From a basic level, dividend investors should probably look at PepsiCo, noting that it has increased its dividend annually for an impressive 52 consecutive years. That, for reference, makes it a Dividend King.

What about PepsiCo’s acquisition of Siete?

With PepsiCo’s many powerful brands and massive sales base, it’s understandable why Wall Street wasn’t excited about the $1.2 billion deal to acquire Siete Brands. The stock has essentially gone nowhere since the deal was announced. And to put a number on it, Siete is estimated to have sales of about $500 million, which is less than 1% of PepsiCo’s 2023 sales.

So this is a small transaction that won’t really help PepsiCo. But it seems attractively priced, about 2.4 times sales, so PepsiCo isn’t paying too much. And the financially strong company should have little trouble finding the money to pay Siete. So there is little concern that the deal will lead to any financial disruption at PepsiCo. In many ways it’s kind of a non-event.

But strategically it is crucial. If you look at the full list of brands that PepsiCo owns, including some of the largest and most important nameplates, they simply weren’t all created. It bought them. Gatorade is a great example of this, as the brand was the crown jewel of Quaker Oats when PepsiCo bought that company. It is one of the most dominant sports drink brands and has catapulted PepsiCo to the top of that product niche at a time when PepsiCo’s own offering was lacking there. This is not to say that the Siete is the next Gatorade. That’s not it. However, Gatorade’s approach is basically the same as Siete’s.

There is overlap between what Siete produces and what Pepsico produces, especially in the chip category. But Siete, a self-described Mexican-American food company, also has offerings on sauce, condiments, beans, tortillas, taco shells and sweets. It will help expand Pepsico’s reach in areas where it already competes, and perhaps even push the company further into the Spanish food category.

PepsiCo is buying a strong, emerging brand that it can use to grow its overall business. Simply connecting Siete to PepsiCo’s powerful marketing and distribution systems will likely increase sales. More importantly, it gives PepsiCo even more reach in the salty snack segment. While not a major problem in itself, this additional acquisition approach is how PepsiCo built its dominant position and how it maintains it over time.

Not a problem and yet a very big problem

PepsiCo’s acquisition of Siete isn’t likely to immediately change the course for the company, which is why investors haven’t paid much attention to it. But if you think about decades, not days, the deal represents the winning business approach that PepsiCo has taken for decades to expand its business — and, just as importantly, to reward dividend investors well along the way. If you’re a dividend investor, Siete is just one more reason to like PepsiCo while its stock appears to be on sale.

Don’t miss this second chance at a potentially lucrative opportunity

Have you ever felt like you missed the boat on buying the most successful stocks? Then you would like to hear this.

On rare occasions, our expert team of analysts provides a “Double Down” Stocks recommendation for companies they think are about to pop. If you’re worried that you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: If you had invested $1,000 when we doubled in 2010, then you have $20,855!*

-

Apple: If you had invested $1,000 when we doubled in 2008, you would have $43,423!*

-

Netflix: If you had invested $1,000 when we doubled in 2004, you would have $392,297!*

We’re currently issuing ‘Double Down’ warnings for three incredible companies, and another opportunity like this may not happen anytime soon.

See 3 “Double Down” Stocks »

*Stock Advisor returns October 7, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

PepsiCo’s $1.2 Billion Siete Purchase: The Underrated Move That Shapes Its Future was originally published by The Motley Fool