As you approach your first year of retirement, it is important to evaluate whether the financial plan you have created to ensure your continued well-being is going as planned. An appropriate plan should include tax calculations to understand how much of your income you will actually have available for needs and wants.

Some people may think that because you pay Social Security benefits through payroll taxes your entire life, it is a tax-free benefit. However, this is often not the case. Both the amount of your Social Security benefits that are subject to taxes and the tax rate itself depend on a handful of factors that are personal to your situation.

To create your own retirement income plan and tax strategy, Talk to a fiduciary financial advisor today.

How Your Social Security Benefits Are Taxed

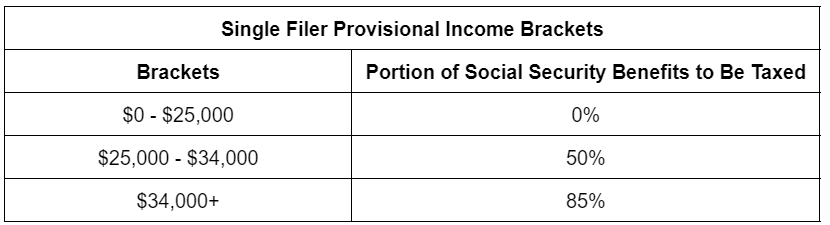

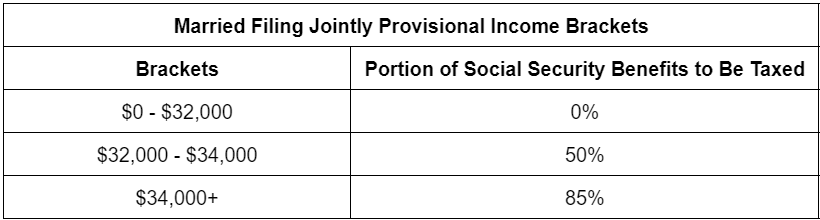

In short, you may pay taxes on 0%, 50%, or 85% of your Social Security retirement benefits. This depends on your provisional incomealthough:

Provisional income = Taxable income + Tax-free interest + ½ of the annual social security benefits

Next, you compare your preliminary income to that year’s income threshold to determine what portion of your Social Security benefits will be taxed. Your tax rate is your marginal rate. For a single person, the thresholds are as follows for the 2023 tax year:

SmartAsset and Yahoo Finance LLC may earn commission or revenue from the links in the content below.

For example, if you had $25,000 in withdrawals from your 401(k) retirement fund, $5,000 in tax-free bond interest, and $29,000 in annual Social Security benefits, your preliminary income would be as follows:

$25,000 + $5,000 + (½ x $29,000) = $44,500

Because this is above the $34,000 income limit, 85% of your Social Security income is taxed.

So, almost $25,000 of your Social Security benefits ($29,000 x .85 = $24,650) for the year would be taxable in this case. Again, that’s only the amount you pay taxes on — not what you actually pay in taxes. The remaining $4,000 or so would be tax-free.

Talk to a financial advisor about developing a strategy to minimize taxes during your retirement.

Deferring 401(k) and IRA Distributions

In some cases, it may make sense to reduce your other income streams to avoid additional taxes on your Social Security benefits. While some advisors may advise their clients to delay taking Social Security as long as possible in order to receive higher benefits, it may be beneficial to reduce the tax liability on Social Security income by delaying other income streams instead. For example, you could delay distributions from a 401(k) or traditional IRA.

This is because any 401(k) or IRA distributions you take in a year count toward your preliminary income, exposing you to the risk of higher taxes on your Social Security benefits. In some cases, however, this trade-off may be worth it, such as if you convert your 401(k) or IRA to a Roth IRA to save taxes in the future. A financial advisor can help you do the math to see which strategy might be more beneficial.

Handling and Managing Your RMDs

If you are in your 70s, you may already be taking or preparing required minimum distributions (RMDs) from your retirement accounts. RMDs will necessarily increase your interim income in many cases, but there may be ways to keep this income out of your interim income to keep your tax rate on your Social Security benefits low.

For example, you can get ahead of your taxes by converting your 401(k) or traditional IRA to a Roth IRA. While this will immediately create a taxable account, it could actually save you more in the long run than just your Social Security benefits, since Roth IRA distributions are tax-free. Keep in mind, however, that you often cannot take penalty-free withdrawals from a Roth IRA within five years of opening an account.

Another alternative is to take an RMD as a qualified charitable distribution, or QCD, if you don’t need the money. QCDs are excluded from your taxable income and wouldn’t push you into a higher qualifying income threshold.

To consider talk to a financial advisor about ways to integrate RMDs into your retirement income plan.

Conclusion

It is important to factor Social Security taxes into your overall retirement budget. Keep in mind that the portion of your benefits that are subject to taxes can change each year, depending on your other income streams. In turn, you will want to plan ahead for these considerations each year.

Tips for retirement planning

-

As you plan for your golden years, it’s important to accurately estimate how much money you’ll have saved by the time you retire. Fortunately, SmartAsset’s retirement calculator can help you predict how much money you’ll need to retire and whether you’re on track to reach that goal.

-

A financial advisor can help you navigate the sometimes complex world of retirement planning. Finding a financial advisor doesn’t have to be difficult. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can schedule a free introductory meeting with your advisors to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

-

Keep an emergency fund on hand in case you run into unexpected expenses. An emergency fund should be liquid—in an account that isn’t subject to big swings like the stock market. The tradeoff is that the value of liquid assets can be eroded by inflation. But a high-interest account allows you to earn compound interest. Compare savings accounts from these banks.

-

Are you a financial advisor looking to grow your business? SmartAsset AMP helps advisors connect with leads and provides marketing automation solutions so you can spend more time on conversions. Learn more about SmartAsset AMP.

Photo credit: ©iStock.com/FG Trade

The post This Is My First Year Taking Social Security. How Can I Lower My Taxes On It? appeared first on SmartReads by SmartAsset.