The last three years have been terrible for C3.ai (NYSE: AI) investors as company shares lost almost half their value during this period. But the good news is that stocks are starting to show signs of life again.

A key reason why C3.ai stock was punished at that time is because of a business model transition that began in fiscal year 2023. As a provider of artificial intelligence (AI) software for enterprises, the company switched from a subscription-based based company. pricing model to a consumption-based pricing model in the first fiscal quarter (ending July 2022).

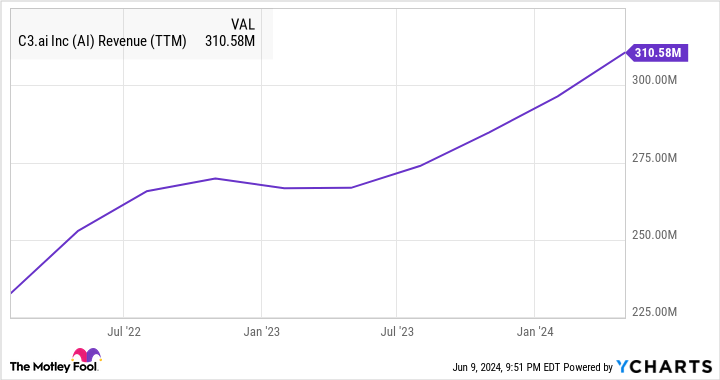

The move was intended to lower the barrier to entry for customers looking to deploy the company’s AI software solutions and help increase revenue. However, it negatively impacted revenue for several quarters as the consumption model prevented the company from receiving monthly subscriptions from customers and locking them into long-term contracts. This is evident from the graph below.

However, the above graph also shows that C3.ai has started growing again. But can the company maintain this momentum over the next three years and deliver solid profits for investors? Let’s find out.

C3.ai’s transition to a business model will accelerate its growth

When C3.ai transitioned to a consumption-based model a few years ago, management pointed out that it would take seven quarters for the transition to be completed. The company forecast that its customers would have switched to the consumption-based model by the eighth quarter, after which revenue growth should start to accelerate.

The good thing is that management’s prediction has indeed come true. Revenue in the fourth quarter of fiscal 2024 (the eighth quarter since the transition began) increased 20% year over year to $86.6 million. That was a significant jump from the flat sales growth the company reported in the same quarter a year ago.

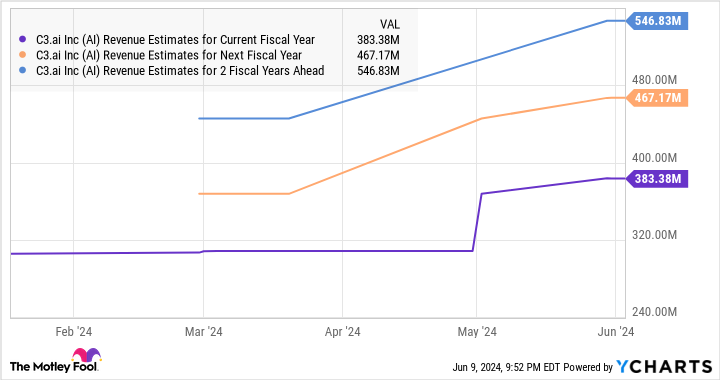

It’s also worth noting that C3.ai ended its latest fiscal year (ending April 30) with a 16% increase in revenue to $310.6 million. Again, that was a significant improvement over the 5% revenue growth it posted in fiscal 2023. As for fiscal 2025, C3.ai expects revenue to increase 23% to $382.5 million (at midpoint ), which further supports growth. the idea that his activities are on the rise.

CEO Tom Siebel’s comments on May’s earnings show that interest in C3.ai’s AI software solutions remains strong. The existing customers have increased the use of the offer, and the number of inquiries from new customers is also quite high. According to Siebel:

In the fourth quarter alone, we received almost 50,000 inquiries from 3,000 companies, each with a turnover of more than $500 million, all expressing interest in our generative AI application, 50,000 … 10,500 in February – in the 28 alone days of February. We currently expect this number to increase to 90,000 applications in the first quarter of ’25.

It’s worth noting that C3.ai closed 191 customer agreements last fiscal year, which was a 52% improvement over the previous year. Since the company is involved in 123 pilot projects, it is likely to win more contracts in the future and continue to build a solid revenue pipeline.

That explains why analysts predict stronger sales growth over the next three years.

This big improvement could see the stock soar over the next three years

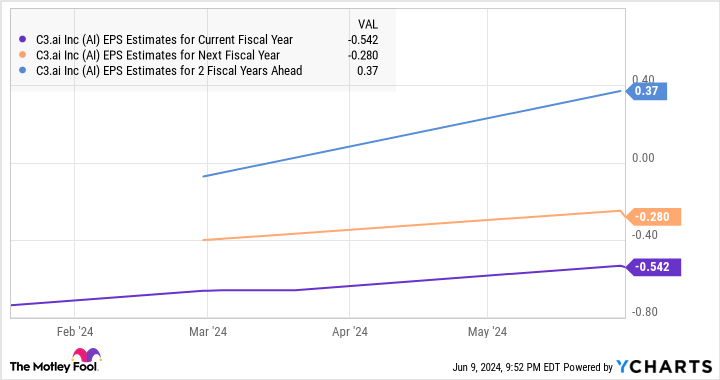

C3.ai ended fiscal 2024 with a non-GAAP net loss of $0.47 per share, which was higher than the $0.42 per share loss reported the year before. That loss should increase even further in the current financial year. However, as the following chart shows, analysts expect C3.ai’s losses to narrow in fiscal 2026, and the company could report non-GAAP profits the following year.

That won’t be surprising, as C3.ai management expects non-GAAP gross margin to remain at the high end of the 70% range now that the business model transition is complete. By comparison, C3.ai ended fiscal 2024 with a non-GAAP gross margin of 69%.

A combination of stronger revenue growth and an increase in the company’s margins will likely help C3.ai become profitable over the next three years. Furthermore, the enormous opportunity in the AI software market, which could be worth $52 billion by 2028, suggests that C3.ai could be at the beginning of a tremendous growth curve.

All of this suggests that C3.ai’s share price performance over the next three years could be much better than what it posted over the past three years. That’s why investors looking to add an AI stock to their portfolio should consider buying it as the latest earnings report appears to have sparked a bull run.

Should you invest $1,000 in C3.ai now?

Before purchasing shares in C3.ai, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and C3.ai wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $740,690!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns June 10, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool recommends C3.ai. The Motley Fool has a disclosure policy.

Where will C3.ai stock be in three years? was originally published by The Motley Fool