Over the past five years, shares of Celsius companies (NASDAQ: CELH) have increased by 6,290%. That means every $1,000 someone invested in Celsius five years ago is worth more than $60,000 today. Not bad. The owner of the Celsius energy drinks brand has seen its sales grow like gangbusters as it gains market share in the highly profitable energy drinks sector and makes investors a fortune.

But what will the next five years look like? The company has some big plans in store and just reported another strong earnings report, pushing the stock close to an all-time high. Let’s see where this monster grower could end up in five years and whether the shares are a bargain at current prices.

Slowing revenue growth, growing margins

At first glance, sales growth in the first quarter of 2024 seemed somewhat weak. Revenue growth was just 37% year-over-year in the period, compared to 102% in the fourth quarter of 2023. Revenue was $355.7 million – a record – but investors should be right to be concerned about slowing revenue growth as this company matures is becoming.

However, it appears management had a good explanation for the massive slowdown: inventory build-up at retailers and distributors. In 2023, Celsius distributors built up inventories in anticipation of demand, leading to an acceleration in sales growth that exceeded 100%.

Now the opposite is happening, causing revenue growth to slow significantly. From a customer perspective, Celsius retail sales in the United States are estimated to have grown 72% in the first quarter, which is closer to the Celsius brand’s actual growth rate. It now has an 11.5% category share in its home market.

A maturing business means increasing profit margins. Celsius had a record operating margin of 23.4% in the first quarter, which is a great sign for shareholders. It comes closer to the competitor Monstrous drinkwhich had an operating margin of 28.5% in the same period.

Can the brand operate internationally?

There is still room for Celsius to grow in the United States. Given the rate at which it is gaining market share, I wouldn’t be surprised if the company doubled or tripled revenue through market share gains and price increases. This should help consolidated revenue grow in the coming years, although you shouldn’t expect 100% growth forever.

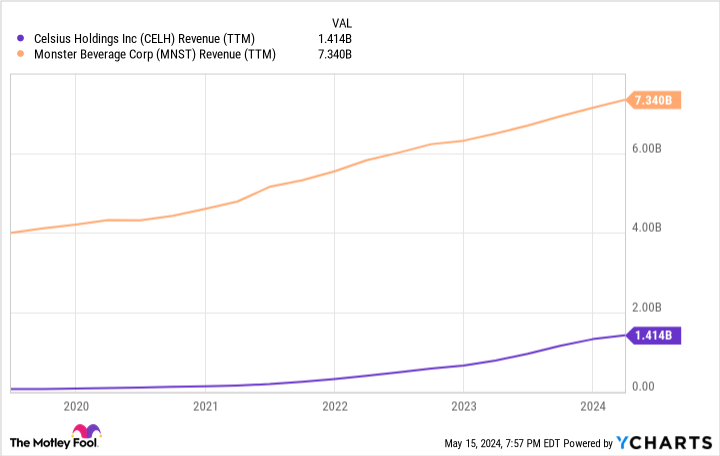

Ultimately, the company will need to expand internationally if it wants to continue growing sales and match the size of industry giant Monster Beverage. Monster generates annual revenue of about $7.3 billion, compared to Celsius’s $1.4 billion. The brand has announced expansions into France, Australia, the United Kingdom and New Zealand in recent months.

So far this has not been reflected in the income statement. International sales in the first quarter were only $16.2 million, or less than 5% of total sales. Investors can’t expect these markets to catch fire overnight, but there should be some concern that Celsius won’t be able to replicate the success it has had in the United States in other countries . International sales will be an important number to track in the coming years as it will be key to maintaining this high sales growth for the brand.

Where will Celsius stock be in 5 years?

Celsius is approaching $1.5 billion in annual sales. Let’s assume that the United States continues to grow market share, is able to raise prices to keep up with inflation, and eventually achieves some modest success in new countries over the next five years. If this happens, I think Celsius could triple its revenue to $4.5 billion in five years.

Let’s also assume that profit margins increase to 25% and apply that to a $4.5 billion revenue base. That’s $1.125 billion in annual revenue. Today, Celsius has a market cap of $22 billion, or a price-to-earnings (P/E) ratio of 20 based on this five-year earnings projection. Again, these are expected profits five years into the future, not current profits. This price-earnings ratio is barely lower than the average price-earnings ratio for the stock market Today.

What this tells me is that much of the strong revenue growth is already priced into Celsius stock, even if you expect revenue to triple over the next five years. For this reason, I wouldn’t be surprised if Celsius shares are at a similar level in five years, making the stock a risky bet for investors right now.

Celsius is a fast growing company. But that doesn’t automatically mean the stock is a buy.

Where you can invest $1,000 now

If our analyst team has a stock tip, it could be worth listening to. The newsletter they have been publishing for twenty years, Motley Fool stock advisorhas more than tripled the market.*

They just revealed what they believe to be the 10 best stocks for investors to buy now… and Celsius made the list — but there are nine other stocks you might be overlooking.

View the 10 stocks

*Stock Advisor returns May 13, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool holds positions in and recommends Celsius and Monster Beverage. The Motley Fool has a disclosure policy.

Where Will Monster Growth Stock Celsius Be in 5 Years? was originally published by The Motley Fool