Hubspot (NYSE: HUBS) Shares are below $500 after falling from their 2024 high of $682, set in April. The stock is down 16% year-to-date and 30% from its 2024 high.

Major changes in valuation can be important signals for investors to take action. Either the stock is available at a new discount price, or there is a fundamental problem that is likely to cause more problems.

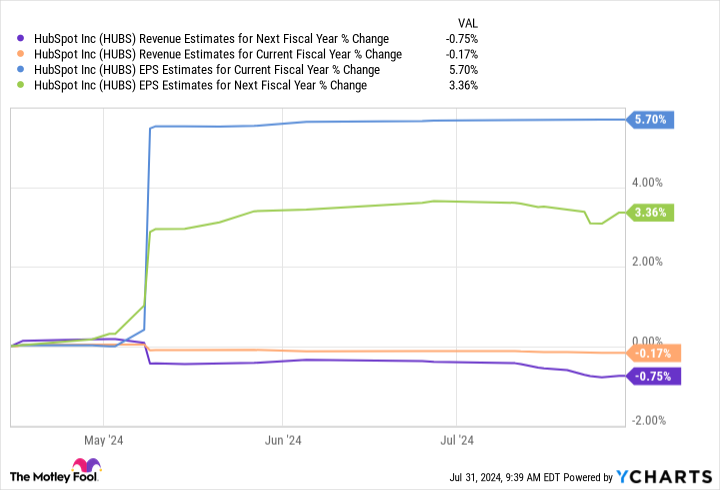

The latest financial results were generally positive

Hubspot’s most recent quarterly results were impressive. The company posted 23% revenue growth and 40% adjusted earnings growth. It produced about $100 million in free cash flow in the first quarter of 2024, up from $60 million in the first quarter of 2023. These numbers all beat analyst expectations.

Hubspot maintained its full-year revenue forecast and raised its profit guidance by 4%. After analysts digested the quarterly results and updated outlook, they kept their revenue forecasts largely unchanged while slightly raising their profit expectations.

From a fundamental perspective, the latest financial results showed little change. Hubspot delivered strong financial results that were closely in line with expectations.

Headlines sent Hubspot’s stock price plummeting in July

For months rumors circulated that Alphabet was exploring a possible acquisition of Hubspot. Early discussions were reportedly progressing, indicating genuine interest from both parties. The news was announced in the first week of April, sending the stock higher. Acquirers typically pay a premium to market valuations, so acquisition rumors tend to have a positive effect.

Unfortunately, the reverse is also true. A stock can plummet if a potential acquisition is called off. That’s exactly what happened to Hubspot on July 10, when reports surfaced that Alphabet and Hubspot were abandoning their efforts. Talks broke off before the companies even reached the due diligence stage, suggesting they were still relatively far from a deal.

The selloff was significant. Hubspot shares fell nearly 20% in the days following the news, leaving the company’s valuation well below its pre-takeover rumor levels in April.

Has the market overreacted?

Hubspot’s July collapse illustrates the volatility that comes with growth stocks with expensive valuations. Acquisition rumors came and went, but the company’s financial outlook has changed little. May’s quarterly results were generally positive and slightly better than expected. Analyst estimates for revenue and earnings over the next two years have barely changed since March. The only difference is that Alphabet won’t be acquiring Hubspot anytime soon.

Despite repeating their predictions, several research analysts substantially lowered their price targets immediately following the news that the acquisition had fallen through. The price target cut was not accompanied by a shift in analyst recommendations. This was purely a recognition of demand trends in capital markets.

From a fundamental perspective, there is no reason for investors to like Hubspot any less. From a valuation perspective, the stock has become more attractive. The risk-reward balance has shifted favorably for potential buyers. Long-term investors now have the opportunity to “buy low.”

Unfortunately, Hubspot is still exposed to much of the same volatility risk. The stock’s forward price-to-earnings (P/E) ratio is nearly 70, even after a decline. It’s also expensive relative to revenue and free cash flow, and its valuation assumes continued rapid growth. In other words, substantial success is already being assumed in the price, even after the July sell-off.

Hubspot dominates the sales and marketing software industry for small and medium-sized business customers. It has a highly rated product suite and high switching costs. This results in high revenue retention and an economic moat.

These provide a solid foundation for continued growth and cash flow generation. That makes it an attractive target for growth investors, but it should only be a priority for long-term investors with a high tolerance for volatility. The stock’s valuation could lead to significant short-term drawdowns, as was evident in July.

Should You Invest $1,000 in HubSpot Now?

Before you buy shares in HubSpot, there are a few things to consider:

The Motley Fool Stock Advisor team of analysts has just identified what they think is the 10 best stocks for investors to buy now… and HubSpot wasn’t one of them. The 10 stocks that made the cut could deliver monster returns in the years to come.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $657,306!*

Stock Advisor offers investors an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks each month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns as of July 29, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Ryan Downie holds positions at Alphabet. The Motley Fool holds positions at and recommends Alphabet and HubSpot. The Motley Fool has a disclosure policy.

With Shares Down Nearly 30%, Is Now the Time to Buy This Tech Software Stock? was originally published by The Motley Fool

")