Stock Like There’s No Tomorrow")

Enterprise product partners (NYSE:EPD) is one of the largest midstream companies in North America, with an integrated system that transports natural gas, natural gas liquids (NGLs), crude oil and refined products. The stock has several characteristics that make it attractive.

Let’s take a look at three reasons why investors should consider delving into the pipeline giant.

1. A safe and growing distribution

With a yield of approximately 7%, Enterprise offers investors a very attractive income stream from its distribution payouts. In fact, the company has increased its distribution every year for the past 25 years. It has done this across different economic and energy price environments, demonstrating the consistency of its business model.

I consider Enterprise’s distribution to be extremely secure. The two biggest areas to look at when it comes to dividend safety are the distribution coverage ratio and the leverage ratio. The first measures how much cash in benefits the company pays out, compared to the distributable cash flow (operating cash flow minus maintenance investments) it generates. On that front, Enterprise had a robust coverage ratio of 1.7x for 2023, showing that distribution is well covered.

Meanwhile, the company ended last year with 3x leverage, which is near the bottom of companies in the midstream space. When companies’ leverage becomes too high, there is a risk that they will cut their dividend. This is not the case with Enterprise.

As such, the company has attractive and safe returns, and its distribution looks set to continue growing.

2. A stable and growing company

Enterprise has expanded its distribution over the past 25 years thanks to its stable, reliable business model. Despite being in the energy sector, the company has little direct exposure to commodity prices.

About 77% of 2023 gross operating profit came from fee-based activities, while 17% came from variances. The latter is where the company can take advantage of geographic arbitrage opportunities, but also by upgrading raw materials to higher value products.

Enterprise also has a solid backlog of growth opportunities, with $6.8 billion worth of projects currently under construction. The company currently plans to spend between $3.25 billion and $3.75 billion on capital expenditures (capex) this year, and another $3 billion by 2025. Over the past decade, it has averaged a return on invested capital (ROIC) of approximately 12%.

ROIC is the gross operating profit of a project dividend, calculated based on construction costs. If the company spends $3 billion to build a new project, it would earn $360 million per year in gross operating profit on that expenditure, which should also be comparable to the cash flow the asset generates.

Given the current backlog of projects and solid ROIC track record, Enterprise has a great runway to grow in the coming years.

3. An attractive valuation

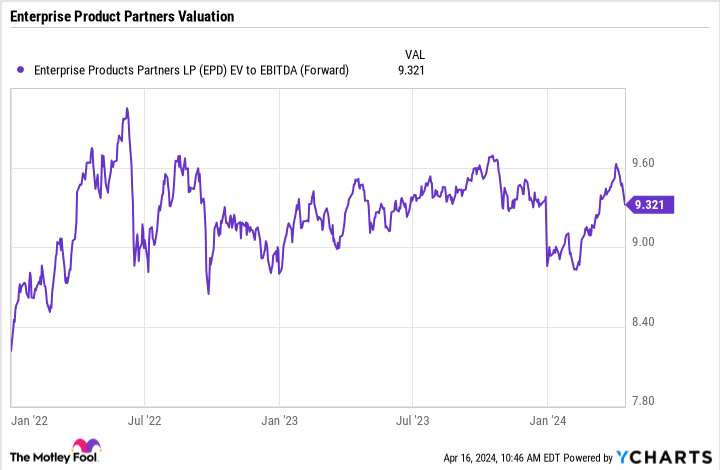

Given the non-cash depreciation costs associated with long-term assets such as pipelines and the debt companies carry, midstream companies are generally valued based on the ratio of enterprise value (EV) to earnings before interest, taxes, depreciation, and amortization (EBITDA). Enterprise value takes into account a stock’s net debt, while EBITDA takes out non-cash costs.

On that basis, Enterprise is trading at just over a 9x multiple.

This is similar to where the stock has traded since the end of the pandemic. Before the pandemic, however, Enterprise shares typically traded at an EV/EBITDA multiple above 11x, and sometimes higher than 15x.

At the same time, the company’s balance sheet has improved since the end of the pandemic, and started showing a much higher distribution coverage ratio from 2018 onwards.

A good time to buy

Given Enterprise’s stable, reliable business model, combined with attractive and growing distribution returns, now seems like a good time to pick up this stock, which is trading towards the lower end of its historical levels. Enterprise has one of the best track records of any midstream stock. With geopolitical tensions rising, it appears to be a company that has both the defensive and growth qualities that should help it perform well in the coming years.

Should you invest $1,000 in Enterprise Products Partners now?

Before purchasing shares in Enterprise Products Partners, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Enterprise Products Partners wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $514,887!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns April 15, 2024

Geoffrey Seiler holds positions at Enterprise Products Partners. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

3 Reasons to Buy Enterprise Product Parters (EPD) Stock Like There’s No Tomorrow was originally published by The Motley Fool