stocks")

Over the past few years, the two hottest trends on Wall Street have been artificial intelligence (AI) and companies doing stock splits. In the days ahead, these two catalysts will collide for the hottest mega-cap stocks of them all. Nvidia (NASDAQ: NVDA).

A “stock split” is a purely cosmetic event that allows a publicly traded company to change its stock price and the number of shares outstanding by the same factor. It is cosmetic in the sense that it does not affect a company’s market capitalization or operating performance.

On May 22, Nvidia announced that its board had approved a 10-to-1 forward split. In other words, shareholders will own ten times as many shares, reducing the share price to 1/10 of what it is today. When the market opens on Monday, June 10, Nvidia will trade at its split-adjusted share price.

The reason investors have flocked to stock splits (and more specifically companies that implement forward splits, like Nvidia) is because they have a long track record of innovation and outpacing the competition.

Nvidia has consistently rejected Wall Street’s revenue and profit forecasts for more than a year, and there’s no doubt that artificial intelligence is the reason. The company’s H100 graphics processing units (GPUs) have become the default choice of companies looking to train large language models and run generative AI solutions. As demand swamps supply of these high-compute chips, Nvidia has enjoyed exceptional pricing power. As a result, gross margin in the last quarter (ending April 28) reached an astonishing 78.4%.

While stock split stocks are largely unstoppable, and AI is the hippest thing since sliced bread, I’m here to offer what I think is a necessary dose of reality. Namely, seven reasons to completely avoid Wall Street’s hottest AI stocks and the newest member of the stock split club, Nvidia.

1. The price power of AI GPU has probably reached its peak

Let’s start with the obvious: new competitors are entering the AI-GPU arena. Intel (NASDAQ: INTC) is scheduled to launch its Gaudi 3 AI accelerator chip in the third quarter Advanced micro devices (NASDAQ: AMD) has been steadily ramping up the rollout of its MI300X GPU, which is a direct competitor to Nvidia’s H100 GPU.

Here’s the catch: Even if Nvidia’s H100 and successor chips maintain a compute advantage over Intel, AMD and other future competitors in AI-accelerated data centers, the mere presence of these chips in the market will reduce the overwhelming supply crunch that caused Nvidia’s GPU prices to drop. primarily in the stratosphere.

Nvidia’s fiscal second-quarter forecast calls for a gross margin rebound of 235 to 335 basis points, which could be indicative of a spike in the pricing power of its AI infrastructure.

2. Internal competition is increasing

I’d say the biggest reason to avoid buying Nvidia stock, upcoming stock split or not, is the upside we’re witnessing internal competition.

While most people are focused on what Intel and AMD are doing to counter Nvidia’s dominance in high-compute data centers, they overlook the fact that Nvidia’s top customers are all developing their own AI GPUs. Microsoft, Metaplatforms, AmazonAnd Alphabet account for about 40% of Nvidia’s net revenue – and all plan to deploy internal Ai chips in their data centers.

Regardless, whether these internally developed chips should complement or ultimately replace Nvidia’s GPUs is irrelevant. The key point here is that we are likely to witness a spike in order activity among the most influential companies on Wall Street.

3. US regulators have tightened export restrictions to China

American regulators aren’t doing Nvidia any favors either. In 2022, regulators restricted Nvidia’s ability to export its powerful artificial intelligence chips to China, the world’s second-largest market by gross domestic product.

In response to these limitations, Nvidia developed the toned-down A800 and H800 GPUs specifically for China. Last year, US regulators also restricted the export of these chips to China.

Not being able to export to China potentially costs Nvidia billions of dollars in sales every quarter.

4. No insider purchases in more than three years

In December 2020, Nvidia Chief Financial Officer Colette Kress purchased 200 shares of her company. Since this open market purchase, no other insider has purchased a single share of Nvidia stock.

On the other hand, there have been dozens and dozens of insider stock sales over the past 3.5 years. While there are viable reasons to sell shares that are generally beneficial, such as for tax purposes, there is virtually only one reason to buy shares of a stock: the belief that it is undervalued. If no insider has chosen to buy Nvidia stock in the last 41 months, why would you?

5. History is undefeated

Past performance is no guarantee of future results. But when it comes to the next big trends and innovations, history is unbeaten for more than thirty years.

Every next-big-thing investment trend of the past thirty years has fought its way through a bubble-bursting event in the early stages of its adoption. Investors have consistently shown that they overestimate the adoption and utility of new trends and technologies, and it’s hard to believe that artificial intelligence won’t follow the same path.

No company has benefited more directly from the AI revolution than Nvidia. This means it will likely be hit hardest if the AI bubble bursts and investors’ high expectations are not met.

6. The signs of the recession and the stock market correction are worrying

A sixth reason to leave Nvidia stock on the shelf even as the long-awaited stock split takes place within days is because a combination of recession forecasting tools and stock market indicators are warning of potential future trouble.

For example, we have witnessed the first notable decline in the US M2 money supply since the Great Depression. The only four times since 1870 that the M2 fell by at least 2% annually were associated with periods of depression and high unemployment. Although a depression is highly unlikely today, a decline in available capital in circulation is a key ingredient for an economic downturn.

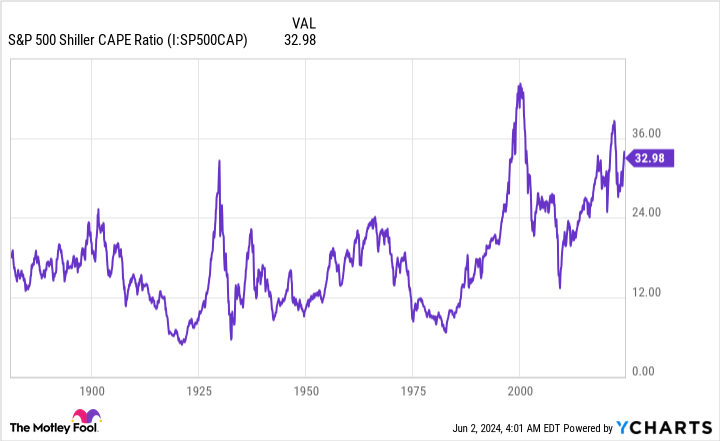

Meanwhile, the S&P500The Shiller price-to-earnings ratio (P/E) is at one of the highest values (34.54, as of the closing bell on May 31) in history when retested back to 1871. The Shiller P/E is based on the average inflation-adjusted income over the past ten years.

The five previous instances where the Shiller P/E exceeded 30 during a bull market run were ultimately followed by declines in the S&P 500 and/or Dow Jones Industrial Average of at least 20%. Companies trading at a premium, such as Nvidia, would be most likely to collapse during a correction.

7. A stock split won’t mask the valuation equations of the dot-com bubble

The seventh and final reason not to buy Nvidia stock is the company’s valuation.

On the surface, you could say that Nvidia is still fairly cheap. It trades for about 31 times Wall Street’s consensus earnings per share (EPS) in fiscal 2026 (Nvidia’s fiscal year ends in January), and Wall Street is expecting annualized earnings growth of about 46% over the next five years .

But on a twelve-month price-to-sales basis (TTM), Nvidia is harking back to the height of the dot-com bubble. Nvidia’s TTM sales figures are comparable to Amazon’s Cisco systems just months before the dotcom bubble burst.

Given that no next-big-thing innovation has been able to prevent an eventual bubble burst, this valuation premium is a concern that should not be swept under the rug.

Should You Invest $1,000 in Nvidia Now?

Before you buy shares in Nvidia, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $704,612!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns June 3, 2024

Suzanne Frey, a director at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, former director of market development and spokeswoman for Facebook and sister of Mark Zuckerberg, CEO of Meta Platforms, is a member of The Motley Fool’s board of directors. Sean Williams has positions in Alphabet, Amazon, Intel and Meta Platforms. The Motley Fool holds positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Cisco Systems, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls to Intel, long January 2026 $395 calls to Microsoft, short January 2026 $405 calls to Microsoft, and short May 2024 $47 calls to Intel. The Motley Fool has a disclosure policy.

Nvidia Makes a 10-for-1 Stock Split: 7 Reasons to Completely Avoid Wall Street’s Hottest Artificial Intelligence (AI) Stocks, originally published by The Motley Fool