A good way to spot trends in the stock market is to look at which companies asset managers invest in. While there are many hedge funds out there, one of the more closely followed portfolios comes from Renaissance Technologies.

Renaissance is led by Jim Simons, who is actually a mathematician by profession. A look at the fund’s most recent filings shows one clear trend: Renaissance is currently investing heavily in the technology sector.

But as virtually every tech company imitates its artificial intelligence (AI) capabilities, it can become difficult to separate the winners from the wannabes. Let’s dive into Renaissance’s portfolio and assess Simons and his team’s most bullish opportunities.

1. Nvidia

Nvidia (NASDAQ: NVDA) is the third largest position in Renaissance’s portfolio and the largest of the “Magnificent Seven” positions.

What I find interesting about Nvidia’s prominence in the portfolio compared to other tech stocks is its relationship with Renaissance’s largest holding overall: Novo Nordisk. Although Renaissance trimmed its position in the Ozempic maker by 2.4 million shares last quarter, Novo Nordisk is still handily the top holding in Simons’ portfolio. Following a milestone year in 2023, Novo Nordisk recently teamed up with Nvidia to help accelerate AI in the healthcare world.

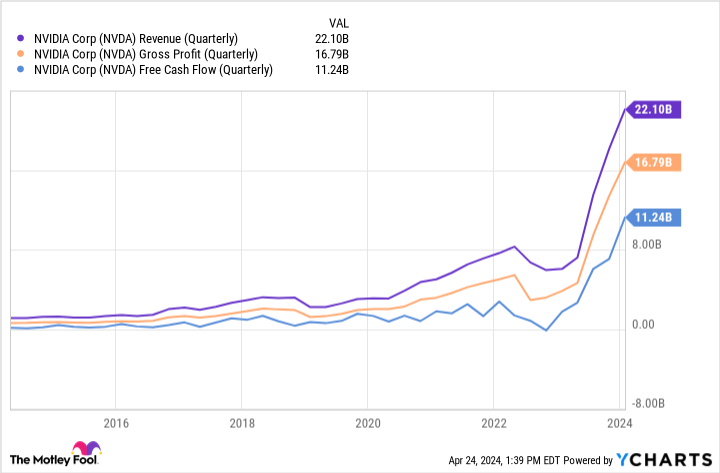

The chart above illustrates Nvidia’s revenue, gross profit, and free cash flow for each quarter of the last 10 years. The obvious conclusion is that the renewed demand driving AI services has ignited a new growth frontier for Nvidia.

However, there is more going on here. Nvidia plays a monumentally important role in the AI revolution. The company’s H100 and A100 graphics processing units (GPUs) are the core engine that powers numerous AI applications, including training generative AI models, improving accelerated computing, and more.

Nvidia’s GPUs are deployed in Tesla vehicles to assist with autonomous driving and are also utilized by Metaplatforms (NASDAQ: META) to hone its targeted advertising capabilities in an intensely busy social media landscape.

The superior pricing power that Nvidia has achieved over the competition has resulted in staggering earnings growth. As an investor, it’s encouraging to see Nvidia aggressively investing its profits into other high-growth opportunities.

For example, earlier this year Nvidia joined OpenAI, IntelAnd Microsoft in a $675 million funding round for a humanoid robotics startup called Figure AI.

I think this is an especially smart move, because Nvidia has a lucrative opportunity to help Figure AI’s development, both from a hardware and software perspective. In a way, owning Nvidia is akin to owning an index fund that focuses on different aspects of the AI domain.

Nvidia is active in semiconductor chips, robotics, enterprise software and data center services. The productive nature of its operations leads to a variety of AI-powered applications and paves the way for a robust long-term roadmap.

Given the tremendous opportunity Nvidia presents, it’s not surprising to see the company earn such a high ranking in a highly regarded portfolio like Renaissance.

2. Meta

Meta Platforms rounds out the top five positions in the Renaissance portfolio. For the quarter ending December 31, Renaissance purchased a whopping 2 million shares of Meta stock – an increase of more than 2,000% over its previous allocation.

2023 has been a year of transformation for Meta, and I’m not surprised to see smart money flowing into the stock.

Last year, Meta underwent several layoffs in an effort to lower its cost profile – which briefly inflated after some significant investments related to the 2022 Metaverse. Additionally, the company has doubled its core advertising business and proven it can handle the increasing to fend off competition, among other things Alphabet and TikTok.

The table below illustrates some key operational metrics for Meta:

|

Metric |

2022 |

2023 |

Change |

|---|---|---|---|

|

Gain |

$116.6 billion |

$134.9 billion |

16% |

|

Operating income |

$28.9 billion |

$46.7 billion |

62% |

|

Free cash flow |

$18.4 billion |

$43.0 billion |

134% |

Data source: Meta.

Meta’s return to respectable revenue growth, combined with disciplined cost control, ultimately led to rising profitability. The company showed a real sign of maturity by announcing that it will reinvest these profits in the form of a dividend and an expanded share buyback program.

Considering Meta’s forward price-to-earnings (P/E) ratio of 24.5 is currently the second lowest among the Magnificent Seven, I think the stock looks particularly attractive as sales and earnings appear to be back on track.

3. Amazon

The last company I’ll examine is Renaissance’s sixth-largest holding company, a specialist in e-commerce and cloud computing Amazon (NASDAQ: AMZN).

I see Amazon in a similar light to Nvidia. Although the company is largely known for its online store, Amazon is a much more prolific company. Thanks to Amazon Web Services (AWS), the company is a leader in the field of cloud computing and is also active in the world of streaming and advertising.

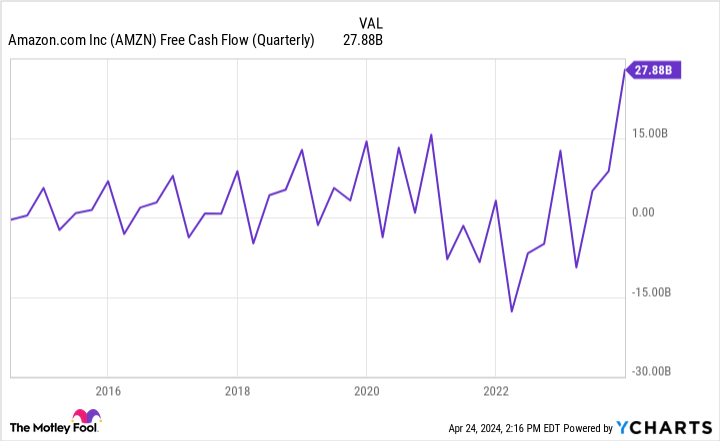

The trends below touch on an important theme for Amazon investors.

Persistent inflation and high borrowing costs have taken their toll on Amazon’s business in recent years. However, 2023 was somewhat of a recovery year, as Amazon sharply returned to being a consistently cash flow positive business. And like Nvidia, Amazon is using this money to stimulate new growth.

In September, Amazon pledged a $4 billion investment in AI startup Anthropic. The overarching tenet of the deal was to integrate Anthropic into AWS to help unlock new growth opportunities.

Furthermore, AI has the potential to span Amazon’s entire ecosystem. For example, the technology could help Amazon discover cost efficiencies it can integrate into warehouse and fulfillment centers, as well as new marketing tactics it can use for both its e-commerce and advertising segments.

Amazon’s price-to-sales ratio (P/S) of 3.2 is essentially identical to its 10-year average, making it an attractive buy for long-term investors.

I think Simons is on to something with his particular Magnificent Seven allocations, and I see each of the companies discussed above as solid opportunities for investors with a long-term horizon.

Should You Invest $1,000 in Amazon Now?

Before you buy stock in Amazon, consider this:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $537,557!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns April 22, 2024

Randi Zuckerberg, former director of market development and spokeswoman for Facebook and sister of Mark Zuckerberg, CEO of Meta Platforms, is a member of The Motley Fool’s board of directors. Suzanne Frey, a director at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, Novo Nordisk, Nvidia and Tesla. The Motley Fool holds positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends Intel and Novo Nordisk and recommends the following options: long January 2025 $45 calls to Intel, long January 2026 $395 calls to Microsoft, short January 2026 $405 calls to Microsoft, and short May 2024 $47 calls to Intel. The Motley Fool has a disclosure policy.

Billionaire Investor Jim Simons Just Bought These 3 “Magnificent Seven” Stocks Originally published by The Motley Fool