United Parcel Service (NYSE:UPS) The stock rose by a whopping 83% between 2020 and the end of 2021 – thanks to a shift from services and in-store shopping to home delivery. But since the start of 2022, UPS is down more than 35%, compared to a 12% gain in the S&P500.

This is why the high-yield dividend stocks deserved to sell, but are now worth buying.

A big delay

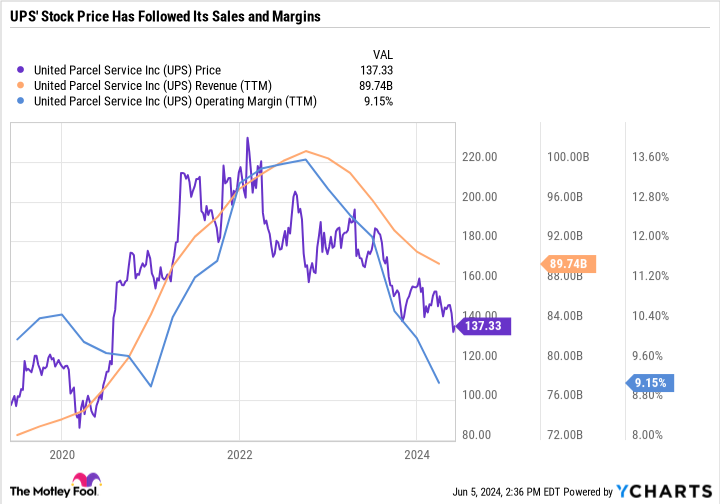

One look at a graph of UPS’s stock price, sales and operating margin, and it’s easy to see why the stock is hovering around a three-year low.

During the onset of the COVID-19 pandemic, UPS’s high-margin business-to-business volumes plummeted. However, demand for parcel delivery to private individuals increased dramatically, leading to rapidly rising revenues. As the business environment recovered, UPS entered a golden period of revenue growth And rising margins. The chart shows the share price peaking in early 2022, with revenue and operating margins peaking later that year.

The past two years have been very difficult for UPS, for reasons both within and beyond its control. The company’s most damaging decision was to over-expand its routes in anticipation of continued growth in the U.S. small package market. Unfortunately, UPS’s prediction seriously missed reality, as the pandemic-induced surge in package deliveries proved short-lived.

UPS has revised its forecast and expects a compound annual growth rate of 5.5% in average daily volume from 2023 to 2026. Based on that growth rate, the company expects to grow revenue to a range of $108 billion to $114 billion and reach an adjusted operating level by 2026. margin of at least 13%. In other words, it expects an adjusted operating margin similar to the peak of late 2021 and 2022, combined with higher revenues.

A key part of UPS’s growth plan is healthcare. UPS expects healthcare revenue to double by 2026, driven by organic growth and acquisitions. UPS is betting big on this segment and it’s important to understand that its medium-term goals largely depend on the success of the healthcare industry. Monitoring the segment’s performance in UPS’s quarterly financials, as well as management’s commentary on healthcare during the earnings calls, can help you determine whether the bet is paying off or not going as planned.

Get paid to wait

UPS has set clear medium-term goals and expectations for investors, which is a useful benchmark on which to judge the company. However, until UPS makes progress toward these goals, the stock will likely remain in prove-it mode. The story has changed dramatically, as UPS went from a company that consistently blew expectations to one that was not well informed about the guidelines. UPS is running out of slack, and rightly so.

In times like these, it can be helpful to zoom out and understand what’s driving negative investor sentiment, and assess that sentiment in the context of the long-term investment thesis. UPS is benefiting from a growing economy, both domestically and by design. The move into healthcare, which is both time and temperature sensitive, makes a lot of sense and is a great way to give UPS a competitive edge.

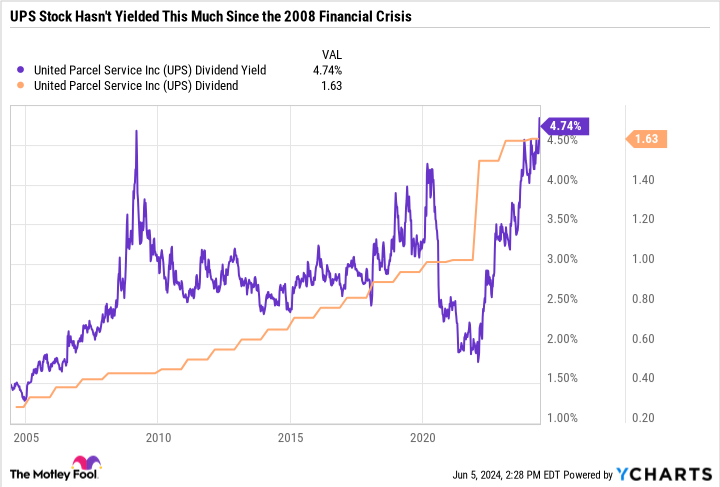

UPS has achieved a valuation and dividend yield that are too generous to pass up.

The dividend yield is 4.7%, the highest in more than fifteen years. UPS has also increased its dividend every year for the past 15 years, including a monstrous 49% increase in early 2022.

In the short term, UPS doesn’t have the earnings growth to justify a growing dividend. However, management’s commentary on the Q1 2024 earnings call indicated that UPS would try to hold the dividend steady or increase it slightly and bring the payout ratio down with earnings growth, rather than cutting the dividend.

UPS has an adjusted payout ratio of 50%, meaning it plans to return half of its adjusted earnings to shareholders through its dividend. UPS recognizes that it must improve its profitability to deliver significant dividend increases again. But in the meantime, the dividend is already quite attractive – especially considering the S&P 500 yields just 1.3%.

UPS’s price-to-earnings (P/E) ratio of 19.9 is close to the 10-year average of 20.6. However, UPS’s forward price-to-earnings ratio is 16.8, indicating that analysts expect earnings to improve in the coming year.

Consensus analysts estimate earnings per share (EPS) to reach $8.23 in 2024 and as much as $9.82 per share in 2025. These are only projections, so they should be approached with caution. However, with a price per share of around $137.50, UPS looks very cheap if earnings improve even closer to the forecast pace.

Don’t pass up this passive income opportunity

In today’s expensive market, it can be difficult to find juicy opportunities. But UPS is one of them.

UPS’s cheap valuation and high dividend yield provide valuable incentives to hold the stock during these challenging times. However, if UPS continues to disappoint and deviate from its medium-term targets, analysts will likely revise their forecasts, and the stock won’t look like such a bargain.

UPS is a good example of a stock that has fallen out of favor. It’s easy to highlight the company’s recent flaws and blunders, but it’s also a big mistake to discount UPS’s impressive market position and career in healthcare.

The passive income opportunities and potential for a turnaround outweigh the downsides, making UPS a valuable high-yield dividend stock to buy if you’re willing to ride out the volatility.

Should you invest €1,000 in United Parcel Service now?

Before purchasing shares in United Parcel Service, please consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and United Parcel Service wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $740,688!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns June 3, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool recommends United Parcel Service. The Motley Fool has a disclosure policy.

This dividend stock hasn’t returned this much in over 15 years. Here’s Why It’s a Buy Near a 52-Week Low Originally published by The Motley Fool