Micron technology (NASDAQ:MU) shares have set the market on fire over the past five years, with impressive gains of 258% and faster than previous years. Technology sector Nasdaq-100 index return of 136% with a wide margin.

A fair share of the stock’s gains have come since early 2023, when the hype around artificial intelligence (AI) started to build. And now AI is more than just a hype for chipmakers like Micron, whose products are helping build the requisite infrastructure needed to spread this technology. The good part is that AI will likely remain one of the key growth drivers for Micron in the long term, driving robust top-line and bottom-line growth.

Let’s take a look at why that might be the case and try to find out whether Micron can continue to post big profits over the next five years.

Micron Technology will spend more money to meet the demand for AI chips

When Micron Technology reported its second-quarter fiscal 2024 results in March, the company posted a 58% year-over-year increase in revenue to $5.8 billion. However, it could have achieved even stronger growth if it had been able to meet the entire demand for memory chips, known as high-bandwidth memory (HBM), deployed in AI servers.

During its earnings conference call in March, Micron management noted that it is “on track to generate several hundred million dollars of revenue from HBM in fiscal 2024.” The company also said its entire 2024 HBM capacity has been sold out and an “overwhelming majority” of its 2025 supply has already been allocated.

So it wasn’t surprising that Micron management recently increased its 2024 capital budget to $8 billion, up from the previous estimate of $7.5 billion. The company will likely spend the increased budget on producing more HBM, especially given that it expects this type of memory chip to become a billion-dollar business in the next fiscal year, which starts in September.

Micron therefore expects a major acceleration in revenue from HBM chip sales from fiscal 2024 to fiscal 2025. More importantly, its HBM business appears built for healthy long-term growth. That’s because AI-oriented chips are expected to make up 61% of the total memory market by 2028, up from just 5% this year, according to Micron’s peer SK Hynix.

Market research firm Yole Group estimates that the HBM market could generate annual revenues of $14 billion by 2024. Even better, the company predicts that HBM shipments could increase at a compound annual growth rate (CAGR) of 45% through 2029. So, Micron is doing the right thing by increasing capital investments as this move should allow the country to take advantage of the lucrative HBM opportunities in the long run.

However, it’s worth noting that Micron will benefit from the spread of AI in more ways than one. While the possibilities for servers are vast, investors should not forget that AI-enabled smartphones and personal computers (PCs) will add to the chip maker’s addressable market.

According to Global Market Estimates, the market for generative AI-enabled smartphones and PCs is expected to register a CAGR of almost 35% through 2029. Moreover, it is expected that every AI-enabled smartphone and PC will contain more memory content. According to Micron, AI PCs reportedly have 40% to 80% more dynamic random access memory (DRAM) than traditional PCs. On the other hand, the company expects that “AI phones will contain 50% to 100% more DRAM content compared to today’s non-AI flagship phones.”

All this explains why the memory market is expected to generate annual revenues of $321 billion by 2030, up from $194 billion last year, according to Fairfield Market Research. It could pave the way for Micron to continue growing at a healthy pace over the next five years.

Stronger growth could lead to more upside in stock prices

We’ve already seen Micron deliver excellent revenue growth last quarter. The impressive sales growth is expected to translate into a significant increase in operating results.

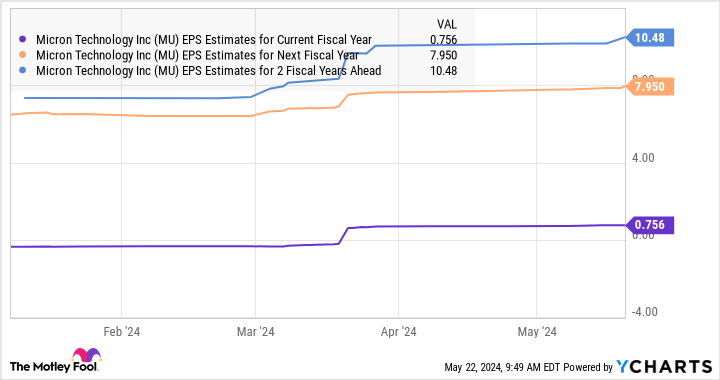

By comparison, Micron ended the previous fiscal year with a loss of $4.45 per share due to weakness in the memory market caused by weak sales of smartphones and PCs. Annual earnings growth over the past five years is just over 10%, but as the chart above indicates, net growth is likely to accelerate noticeably.

So there’s a good chance that Micron’s revenues will grow faster in the next five years than in the past five years. The market could reward this acceleration with more share price gains, so buying Micron right away would be a smart move as the company trades at an attractive 18x earnings.

Should You Invest $1,000 in Micron Technology Now?

Consider the following before purchasing shares in Micron Technology:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns May 13, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Where will Micron Technology stock be in five years? was originally published by The Motley Fool

Stock Surge and Is It Justified?")